A Strong March Leads to a Surge in Chinese GDP in Q1 2023

Economic news and commentary with April 18, 2023

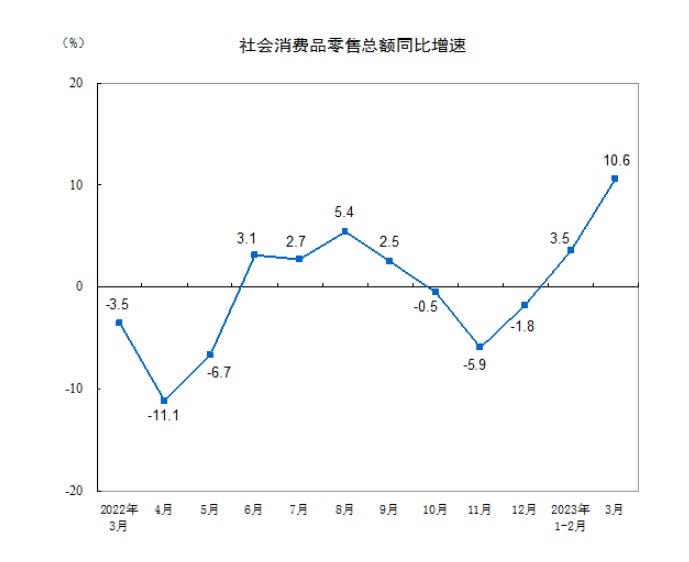

China GDP, Retail Sales, Industrial Production & Fixed Asset Investment

After a disappointing start to the first quarter, it appears that a strong March in China helped the economy bounce back strongly from a weak 2022. GDP grew 2.2% QoQ and 4.5% YoY in Q1 2023, beating consensus expectations that were heavily influenced by the frailty of the January/February numbers. In particular, China saw its industry grow 3.0% YoY, up slightly from 2.7% YoY in Q4 2022. This includes manufacturing growth of 2.9% YoY and mining growth of 3.2% YoY. The GDP beat was not a result of better factory activity. Instead, China’s services sector finally experienced its resurgence from the harsh restrictions of the last two years. Services grew a robust 5.4% YoY, up significantly from 2.3% YoY in Q4. The annual improvement in the service industry production index in March was a sharp 9.2% YoY. It appears that Chinese consumers got up and out into services businesses as spending there finally increased as it was expected to for some time. Tourism has especially been a boon for growth as domestic and international travel has recovered in Q1. One key area to note is real estate. The struggling sector has suffered from weak financial conditions and thus weak investment. It appears that the trend will continue in 2023. Real estate activity was down -5.8% YoY.

GDP received a huge boost from consumer spending in Q1 which was bolstered by surge in retail sales in March. Sales jumped 10.6% YoY which is a sharp acceleration from February's growth of 3.5% YoY. There was growth in almost every segment of sales, but non-durable goods categories saw the largest expansion. Food sales surged 26.3% YoY on the month alongside other non-durable goods markups including clothing (17.7% YoY) and entertainment goods (15.8% YoY). Durable goods categories, especially related to real estate, were the weakest. Building materials sales were down -4.7% YoY, and household appliance sales fell -1.4% YoY. These trends confirm that there are two major factors impacting the Chinese economy’s path. The first is a strong reopening catalyst that is sparking positive consumption developments, something that was largely expected by analysts when putting together growth estimates. The second is shaky credit conditions that are restricting both businesses’ and individuals’ abilities to make big purchases. Fixed asset investment grew 5.1% YoY in March which was a -0.4 ppt decline from February growth. Private investment was up only 0.6% YoY. Fiscal and monetary policy actions to address credit concerns are increasingly being considered in 2023.

Finally, we have a vigorous improvement in Chinese industrial production in March, up 9.3% MoM and 3.9% YoY in March (production grew 2.4% YoY in February). Manufacturing production was up 4.2% YoY, and as discussed before, was up 2.9% YoY in the first quarter. The two big areas of growth were in the auto manufacturing industry, up 13.5% YoY, and the electrical machinery manufacturing industry, up 16.9% YoY. Both are seeing booms from Chinese investment in green energy industries which has been a new goal of the Xi administration’s plan to dominate the space as it escalates competition with the US and Europe. New energy vehicle production surged 33.3% YoY, and solar cell production jumped even more, up 69.7% YoY. This will continue to be a trend driving growth in China for years to come.

China’s economy looks to be back. The Asian giant’s resurgence from COVID is being fueled by its citizens finally going out and spending again, sparking a much-needed boom in the services sector. Businesses are starting to feel that they have room to stretch their legs and expand again, especially in industries that are favored by Xi’s focus on high-tech manufacturing and green energy which aligns with China’s geopolitical struggle with the US and Europe. For now, though, weakness in those two regions is keeping Chinese export growth limited as they maintain the status of primary trading partners. Additionally, fragile financial conditions keep a solid ceiling on Chinese growth as debt concerns first sparked by the real estate sector persist. As reopening effects fade and the boom in consumption stabilizes, it seems that the economy will have to be driven by stimulating monetary and fiscal policies to sustain the strong performance that we have seen in Q1 2023. Nevertheless, for now it seems like the world’s Asian giant is back.

Canada CPI

The March CPI report for Canada provides support for the Bank of Canada’s decision to pause rate hikes in its last meeting. Canada's CPI grew 0.5% MoM and 4.3% YoY in March, a significant downgrade from 5.2% YoY in February. As a result of the steep monthly increase in prices in March 2022 (+1.4%), base-year effects, notably gasoline prices, continued to have a strong downward impact on consumer inflation, contributing to the year-over-year deceleration in March 2023. Energy prices did increase on the month (up 0.7% MoM) but are down sharply over the year at -6.9% YoY. Food prices remain sticky, up 0.2% MoM and 8.9% YoY. Excluding food and energy, prices were up 4.5% year over year in March, following a 4.8% gain in February. Remove the elevated mortgage interest cost index which has inflated thanks to Bank of Canada rate hikes and prices were up just 3.6% YoY. In general, goods and services prices saw moderate increases of 0.6% MoM and 0.5% MoM respectively with services inflation now at 5.1% YoY. Because of that last stat, the Bank of Canada will remain focused on wage growth since it is a driver of elevated services inflation and will become a major factor in whether the BoC decides to raise rates again. Based on the current trend, it looks like that will not need to happen again.

Still to come…

N/A

Morning Reading List

Other Data Releases Today

In the Reserve Bank of Australia's April minutes, members wanted to make it clear that the pause in rate hikes was not a result of any weakness in the financial sector and only so that the RBA could gather more data.

The UK added 31k jobs in March, and the unemployment rate in the quarter to February edged up 0.1 ppts to 3.8%. Job vacancies fell -47k to 1.1 million indicating some loosening in the labor market, while nominal earnings were up 5.9% YoY.

The Italian trade balance improved to €2.9 bil as exports increased 0.4% MoM and imports fell -1.4% MoM in February. Total imports are down -6.5% YoY including a decline of -15.5% YoY for non-EU imports as the economy slows.

The ZEW Indicator of Economic Sentiment for Germany fell -8.9 pts to 4.1 in April. The Economic Situation Germany index (tracking current conditions) improved 14.0 pts to -32.5. Sentiment has likely declined on new financial stability concerns.

In Germany, the number of building permits for dwellings was down -23.4% YoY in January and February compared with the same period a year earlier. The number of building permits has decreased each month since May 2022. Since October 2022, the decline has amounted to more than 10% each month.

US housing starts edged down -0.8% MoM and -17.2% YoY in March. Single-family starts up 2.7% MoM, and multi-family starts down -6.7% MoM. Permits issued down -8.8% MoM and -24.8% YoY.

China GDP

China’s GDP for 1Q23 is better than expected (ING) - 1Q23 GDP grew 4.5%YoY, much faster than the 2.9%YoY recorded for 4Q22. This is a better-than-expected data report. We expect that the government will hold back extra stimulus plans and the yuan should strengthen.

China - Q1 GDP data even stronger than expected (ABN AMRO) - In line with consensus expectations including ours, China’s real GDP growth accelerated sharply in Q1-23. This reflects the country’s rapid reopening rebound, led by services/consumption. The GDP data for Q1 came in even stronger than expected. Quarterly growth accelerated to 2.2% qoq, while annual growth rose to 4.5% yoy.

China | Chinese economy has rebounded with deflationary caution in the post-Covid era (BBVA) - The Chinese economy rebounded significantly in Q1 with 4.5% higher-than-expected growth. However, we need to pay attention to the recent deflationary pressure amid economic recovery.

China’s Economy at a Glance – April 2023 (NAB) - According to China’s national accounts data, its economy grew by 4.5% yoy in Q1. This was stronger than market expectations (at around 4.0%), reflecting the faster-than-anticipated transition period following the end of zero-COVID policies, as well as support from base effects (with the end of Q1 2022 marking the start of the COVID-19 wave that would heavily impact the following quarter). We have revised our forecast for China’s growth in 2023 to 5.6% (5.4% previously), although the property sector and foreign trade could be headwinds. The outlook for 2024 and 2025 is unchanged.

UK Employment

Faster UK wage growth unwelcome news for the Bank of England (ING) - The surprise pick-up in UK wage growth casts doubt over recent indications that pay pressures have started to ease. We should caution that one month doesn't make a trend, though a similar surprise blowout in services inflation due on Wednesday would inevitably move the dial in favour of a 25bp rate hike from the Bank of England next month.

US

January Surge Kept Q1 Positive (First Trust Portfolios) - The US economy is being tugged in two different directions right now. On the positive side we have the

lingering effects of the massive stimulus of 2020-21, the renormalization of the service sector after COVID Lockdowns, and, as always, the entrepreneurial and

innovative spirit of the American people. On the downside we have the early stages of a drop in the money supply that started last year and too much government spending.

Calibrating Policy in an Uncertain Time (Mary Daly, San Francisco Fed) - President Daily speaks at the Salt Lake Chamber in Salt Lake City, UT on uncertainty in monetary policy.

Europe

European Transformation – finally, Europe gets a makeover (DWS Group) - Europe is embracing digitalization and renewable energy – This will require substantial investments.

European high yield – enough meat on the bones (DWS Group) - Emerged as relative winners in the fixed-income segment – and we believe they can still deliver

Japan

Aging societies – the end of “Japanification” (DWS Group) - “Japanification” = shorthand for countries with persisting low inflation and yields, but the comparisons fall short

Australia

The Forward View – Australia: April 2023 (NAB) - The economy continues to evolve in line with our near-term forecasts, with signs that consumption is plateauing ahead of a likely slowdown later in the year. We continue to see well below trend GDP growth of around 0.7% y/y over 2023 as higher rates increasingly weigh on household budgets.

NAB Consumer Sentiment Survey Q1 2023 (NAB) - Consumer stress rises again as cost of living concerns increase to their highest level since late-2018. But Australians remain upbeat about their job prospects, although spending may be slowing now. Household budgets are rebalancing and priorities shifting as consumers are mindful where they spend, switch to less expensive products, and research more.

Canada

Getting a bigger slice of the trade pie (CIBC) - If you want more dessert, you can either buy a bigger pie or carve yourself a bigger slice. It’s much the same for exports: you can either keep the same share of a growing global trade pie or

try to carve out a larger slice.

Inflation

Inflation Monitor for April 17 (BMO) - Although most inflation measures are trending in the right direction, one survey showed short-term consumer inflation expectations jumped by the most since 2021.

Trend Inflation and Implications for the Phillips Curve (Cleveland Fed) - This Economic Commentary estimates trend PCE inflation and a Phillips curve with time-varying parameters while allowing for trend inflation to affect the frequency at which firms change prices. Since the beginning of 2021, trend PCE inflation has risen well above the FOMC’s 2 percent long-term inflation target, and the most recent estimate of trend inflation in 2022:Q4 is 3.4 percent. With the increase in trend inflation, the Phillips curve slope has risen above its pre pandemic level. At the same time, the relationship between current inflation and inflation expectations has strengthened.

Real Estate

Lack of Existing Inventory Continues to Support Builder Sentiment (NAHB) - Builders remained cautiously optimistic in April as limited resale inventory helped to increase demand in the new home market even as the industry continues to grapple with building material issues.

Trade

Deglobalization – rather diversified globalization (DWS Group) - Brexit, Trump, Covid-19 and Putin’s war on Ukraine came as shocks. The end of globalization? Probably not.

How U.S. Import Shipping Costs Vary across Countries and Industries (St Louis Fed) - The higher demand for tradable goods observed across countries in the aftermath of COVID-19 increased international shipping costs to unprecedented levels, leading to nontrivial effects on the level of international trade and economic activity.1 In this blog post, we study the extent to which shipping costs act as barriers to U.S. imports across countries and industries during normal times.

Banking

Financial Fragility without Banks (Liberty Street Economics, NY Fed) - Proponents of narrow banking have argued that lender of last resort policies by central banks, along with deposit insurance and other government interventions in the money markets, are the primary causes of financial instability. However, as we show in this post, non-bank financial institutions (NBFIs) triggered a financial crisis in 1772 even though the financial system at that time had few banks and deposits were not insured. NBFIs profited from funding risky, longer-dated assets using cheap short-term wholesale funding and, when they eventually failed, authorities felt compelled to rescue the financial system.

Commodities

Commodities Tripped Up by Bank Turmoil (BMO) - Although last month's banking stress has moved to the rearview mirror, commodity markets remain concerned about the economic outlook. This helps explain why precious metals prices have soared, with gold recently topping the $2,000 mark and silver gaining nearly 30% since SVB’s collapse.

FX

U.S. Dollar's Reserve Currency Status Still Secure (Wells Fargo) - Over the last few weeks, headlines around the U.S. dollar losing its global reserve currency status have become widespread and captured attention. In our view, the U.S. dollar is not on the brink of losing global reserve currency status at any point in the foreseeable future.

Subscribe to receive Econ Mornings every weekday at 9 am. More economic and finance content on Twitter, Reddit, and my website.