August NFIB Survey Showed a Tough Environment for Small Businesses

Economic news and commentary for September 12, 2023

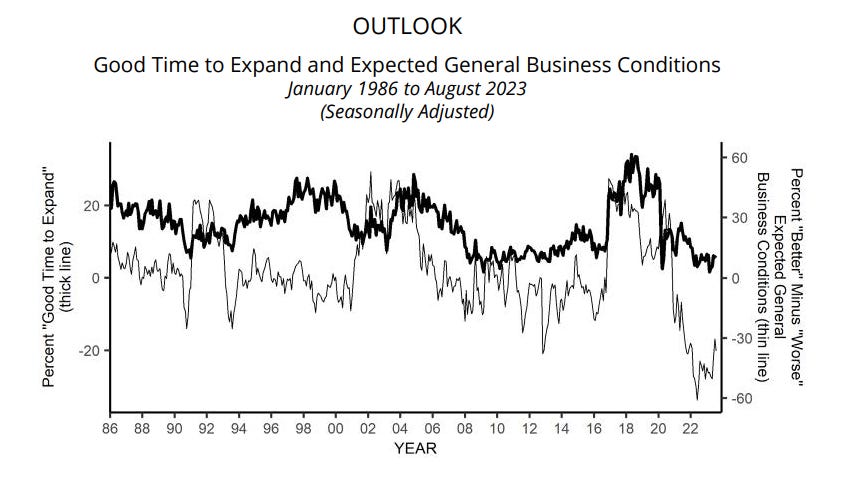

US NFIB Small Business Optimism

The NFIB Small Business Optimism Survey for August emphasized the mixed momentum of the recovery in business sentiment as inflationary pressures ease and interest rates rise. The headline Optimism Index fell -0.6 pts to 91.3 which reversed most of the 0.9 pt increase in July. Regardless, it is still the second highest reading of the year which shows that the general upward trend in sentiment from the lows of late 2022 and early 2023 is intact. A similar trigger could be seen in the biggest moving subindex, the General Business Conditions index, which fell -7 pts to -37 in August, offsetting the improvement in July. This reading is still one of the highest in the last two years. The second largest mover was the index tracking small business earnings. It improved 5 pts from a 2023 low to -25. The volatility in these readings suggests that the inflation situation remains largely questionable for many small businesses. In fact, there was a slight uptick in the percentage of survey respondents who saw inflation as their single most important problem.

The slight rise in inflation concerns is consistent with marginal positive movement in the indexes tracking small business pricing. The Actual Price Changes index which looks at price changes over the last three months ticked up 2 pts to 27 after falling near a three-year low in July. The Price Plans index, tracking the expectations of price changes in the next three months, increased 3 pts to 30. This is the second highest in 2023 though not by a substantial amount. The movements in these price indexes suggest that there is some resistance to the disinflationary path which could be revealed in this week’s CPI release. The rise in energy prices has already reversed the course for headline inflation, and the deceleration in core inflation has already more or less stopped. The lingering concern of elevated inflation continues to threaten to increase small business owners’ inflation expectations which would be damaging to the Fed’s ability to maintain price stability.

The subindexes tracking labor force dynamics for small businesses show that there are some signs of easing in the demand for workers. Most noticeably, the current employment index fell back to the lowest value of 2023 at -4, a -2 pt decline, and the job openings index also fell -2 pts to 40, the lowest since February 2021. Both reflect trends in earlier BLS reports on the labor market like the JOLTS report which showed that the official number of job openings has fallen significantly from its all-time high of over 11 million and the employment situation which showed a notable tick up in unemployment to 3.8%. Despite some strength falling out of demand. there is still a sense that labor shortages are still an impact as the labor supply situation still hasn’t fully returned to where it was before the pandemic. A net 54% of respondents are still seeing few or no qualified applicants and, as a result, the compensation plans index ticked up 5 pts to 26, the highest so far in 2023. Overall, it seems that some of the post-COVID excess hiring demand has started to fall away, but the lack of skilled workers is creating a shortage of skills that small businesses are increasingly having to pay more money to get. This will provide some resistance against easing wage growth.

The NFIB surveys are important because they provide an in-depth look into many aspects of small businesses as they navigate the new high interest rate environment. Small businesses reported an average interest rate of 9.0% on short-term loans in August, this is sharply higher than 6.2% a year ago and 4.6% two years ago. The higher cost of borrowing does appear to be having effects on inflation and hiring as we have seen in the trends of the subindexes tracking these dynamics, but in recent months, the trends have started to move sideways. The Fed meets later this month to decide if it will hike interest rates one more time, and it has a lot of evidence to consider in its deliberations. The stagnation in NFIB Small Business Survey in August will likely be a part of the argument for one additional rate hike to tie up loose ends.

Still to come…

7:50 pm - Japan PPI

Morning Reading List

Other Data Releases Today

The NAB Business Survey Business Conditions index edged up 2 pts to 13 in August. The Business Confidence index also increased marginally by 1 pt to 2. Labor cost growth fell to 3.2% QoQ, partially reversing the 3.7% QoQ increase in July.

The Westpac Index of Consumer Sentiment fell -1.5% MoM to 79.7 in September. The index tracking household finances dropped -4.4 pts to the lowest point in the current cycle despite easing fears that the RBA will raise rates further.

The ZEW Indicator of Economic Sentiment for Germany edged up 0.9 pts to -11.4 in September. The Economic Situation Germany fell -8.1 pts to -79.4, the lowest value in the last three years.

India's CPI edged down -0.1% MoM but was up 6.8% YoY in August, down from 7.4% YoY in July.

Food: 9.2% YoY (-0.5% MoM)

Fuel & Light: 4.3% YoY (0.2% MoM)

Household Goods & Services: 4.8% YoY (0.2% MoM)

Recreation: 3.6% YoY (0.2% MoM)

India's industrial production fell -1.0% MoM but was up 5.7% YoY in July. On a YTD basis, general production was up 4.8% in 2023 over 2022. Manufacturing production was up 4.8% as well despite no change on the month.

UK Employment

The UK jobs report is more dovish than it looks (ING) - Private-sector wage growth in the UK barely increased in level terms between June and July, and alternative data from payrolls showed a second consecutive fall in median pay. We still expect a rate hike next week but with unemployment rising too, this latest data doesn't scream a need to lift rates much further.

US

Macro/FX Watch: US CPI may not be a game-changer for September Fed meeting (Saxo Bank) - The US dollar started the week on the backfoot as intervention threats from Chinese and Japanese officials ramped up. However, fundamentals need to support intervention efforts to bring a more noteworthy recovery in yen or yuan. US CPI on the radar for Wednesday and even a beat on core may not be able to change the pause expectations for September, but could still bring upside in USD if higher-for-longer prevails. UK jobs data, meanwhile, starts to be mixed and may open the door for dovish BOE repricing.

September Flashlight for the FOMC Blackout Period: Our Expectations Ahead of the September 20 FOMC Meeting (Wells Fargo) - We look for the FOMC to keep its target range for the federal funds rate unchanged at 5.25-5.50% at its meeting on September 20. Most market participants expect rates to remain on hold as well.

US Weekly Economic Commentary: Higher for longer… growth and rates (S&P Global) - The US economy is growing significantly above its sustainable trend of roughly 1¾% to 2%, showing striking resilience in the growth of spending amid financial conditions that have tightened measurably over the past year or so.

Failure of Silicon Valley Bank Reduced Local Consumer Spending but Had Limited Effect on Aggregate Spending (Kansas City Fed) - The failure of Silicon Valley Bank (SVB) on March 10, 2023, raised concerns that deteriorating financial

market conditions would reduce consumer spending. We use high-frequency data from California to examine whether the March banking stress influenced trends in consumer spending in counties more affected or less affected by the failure of SVB. We find that while spending declined in some counties heavily exposed to the SVB failure, aggregate consumer spending was not significantly affected.

Our Stagflationary Future (First Trust Portfolios) - We are not back to the 1970s yet, but there are some similarities. Great Society spending pushed government spending on a steep upward trajectory in the 1970s, in spite of the eventual wind-down of the Vietnam War. In turn, policymakers monetized much of this extra spending. The result: a wet blanket of big government which slowed growth, but a boost to inflation from easy money. Reagan and Volcker reversed these two policies and growth accelerated, while inflation fell, after going through a severe recession early in the 1980s.

More Women Working in Construction in 2022 (NAHB) - The number of women employed in the construction industry increased to over 1.28 million in 2022, as the construction industry recovered all jobs lost during the pandemic. Currently, women make up 10.9% of the construction workforce, up from 9.3% in 2002. As the construction skilled labor shortage remains a key challenge for housing, adding new workers is an important goal of the industry. Bringing additional women into the construction labor force represents a potential opportunity for the future.

Europe

ECB preview: a hawkish pause will satisfy hawks and doves (Saxo Bank) - At this week's ECB rate decision, policymakers will likely opt for a pause. Despite the hawks arguing that another hike is warranted, a recession is underway in their own countries. The doves will maintain that we are finally seeing rate hikes feeding through the economy and that overtightening risk is rising. Yet, for the ECB to keep its hawkish bias, policymakers might need to turn to the Pandemic Emergency Purchase Program (PEPP) and stop reinvestments. The PEPP program is half the size of the APP, and redemptions currently account for only 0.02% of its total holdings. Stopping reinvestments under the PEPP program will send a hawkish message without moving the needle much.

ECB cheat sheet: Is a hike hawkish enough? (ING) - Markets are torn. Will the ECB hike this week or not? We think it will, but we look at how different scenarios can impact rates and FX. Even in our base case, we suspect that convincing markets that this is not the peak will be very hard, and dovish dissenters may get in the way. The upside for EUR rates and the euro may not be that big and above all, quite short-lived.

Danish inflation moves lower again (Nordea) - In August, annual Danish inflation fell to 2.4%, the lowest level in the past two years. Also core inflation fell back and stood at 4.2%. This is markedly lower compared to the Euro area.

Swedish August inflation preview: Below 5% (Nordea) - The year-on-year figure for CPIF stood at 4.9% in August according to our call, down 1.5% points from July. The main reason for the drop is so called base effects as prices surged in August last year. Inflation will fall further before year-end.

China

China | Structural change of the trade: forced imports substitution industrialization (BBVA) - China's exports and imports are experiencing some structural change. The forced Chinese version of imports substitution industrialization indicates value chain upgrading and technology self-sufficiency.

FX

FX Talking September: Strong dollar overstays its welcome (ING) - The dollar has enjoyed a strong summer on the back of surprisingly strong US activity data. But this dollar strength is now causing problems in Asia, and local policymakers are fighting back. Expect further containment measures from Chinese and Japanese authorities before the broad dollar trend turns lower – something we expect to see later this year.

Research

Profit Shifting in the 21st Century: Multinationals’ Use of Intrafirm Patent Transfers (St Louis Fed) - In the modern globalized economy, multinational companies (MNCs) can conduct business in markets across the world quickly and efficiently. However, one byproduct of a globalized economy is that multinationals are often able to shift their profits to subsidiaries across jurisdictions in order to minimize their overall tax burden. A common mechanism for profit shifting, and the focus of this blog post, is transferring the ownership of intellectual property (IP). Transferring patents, trademarks and copyrights across a corporate ownership tree allows MNCs to book profits in the jurisdictions with the lowest applicable taxes.

Looking for a way to take advantage of higher interest rates? I recommend SoFi’s high-yield savings account which has a yield of 4.5% (subject to change) and includes FDIC deposit insurance for both its checking and savings accounts just like a traditional bank. Use my referral link to get a sign-up bonus and start earning that rate today. (This is also a great way to support me since I get a bonus too!)

Subscribe to receive Econ Mornings every weekday at 9 am. More economic and finance content on Twitter, Reddit, and my website. You can also see my feed on the PiQSuite platform as a partnered feed.