Australian GDP Growth Slows in Q1 2023, Reflecting Inflationary Pressures and Mixed Component Performance

Economic news and commentary for June 7, 2023

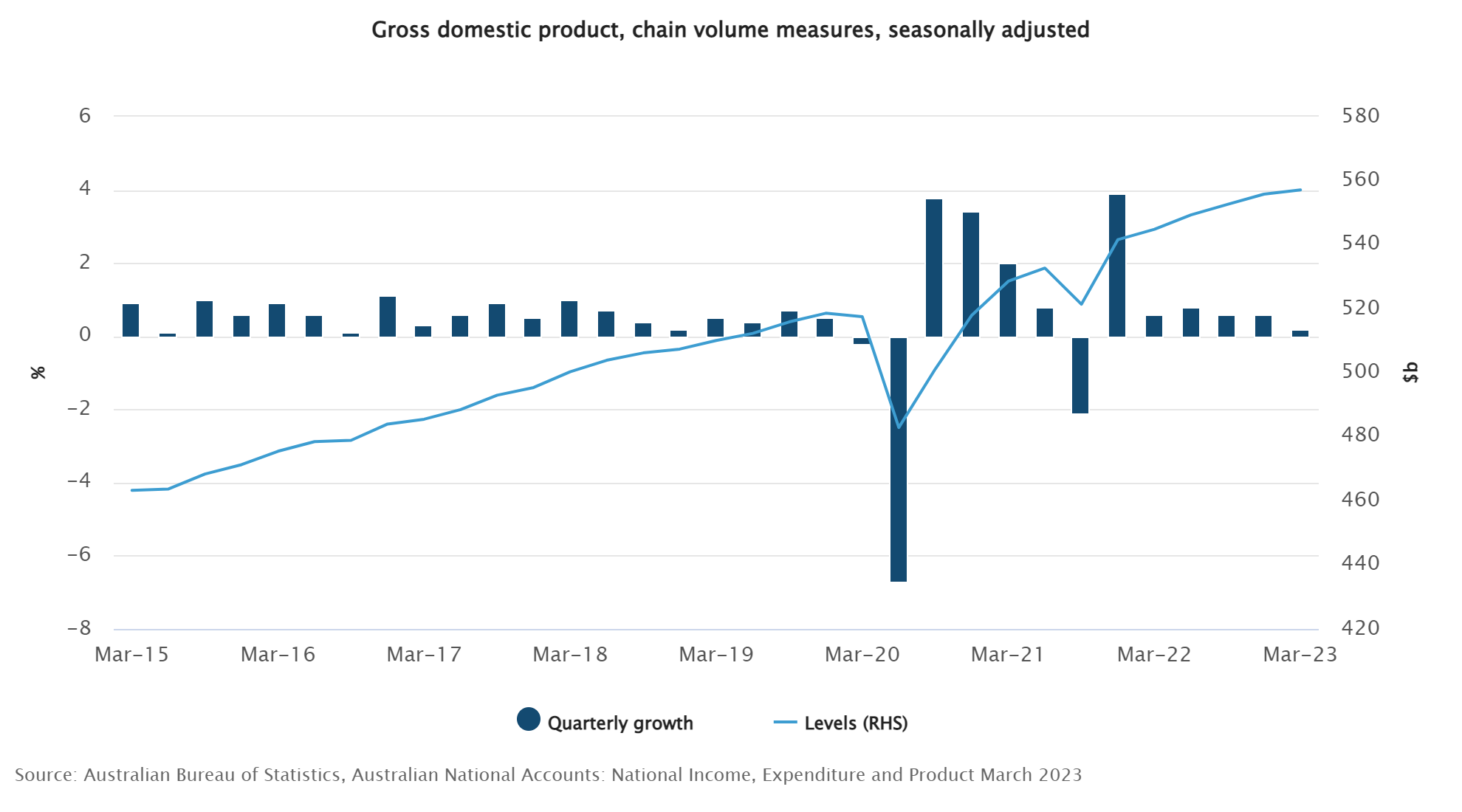

Australia GDP

Australian GDP expanded by 0.2% QoQ in Q1 2023, a decrease from the 0.6% QoQ growth observed in Q4 2022. However, nominal GDP increased by 2.1% QoQ, highlighting the influence of high inflation on overall economic performance. Productivity continued its decline, contracting by -0.3% QoQ in Q1, following a -1.4% QoQ decline at the end of 2022.

Household consumption registered a modest growth of 0.2% QoQ, driven by another quarter of strong income growth. Real disposable income increased by 0.9% QoQ, building on the solid 1.5% QoQ growth witnessed in Q4 2022. Gross fixed capital formation expanded by 1.8% QoQ, bolstered by a 3.0% QoQ surge in public investment. On the private side, the machinery and equipment sector experienced significant growth of 6.0% QoQ, compensating for weakness in residential investment, which declined by -1.2% QoQ. Net exports made a slight negative contribution as the growth in imports, up 3.2% QoQ, outpaced the growth in exports, up 1.8% QoQ.

The GDP deflator, reflecting the overall level of inflation in the economy, rose by 1.9% QoQ in Q1 2023. This increase surpassed the growth of the GDP deflator observed in both Q3 and Q4 2022, at 0.3% QoQ and 0.6% QoQ respectively. Inflationary pressures persisted, particularly in the services sector, due to skilled labor shortages and a tight labor market, which exerted upward pressure on labor costs. Conversely, goods inflation moderated as prices for capital goods adjusted in line with import prices for materials. Consumption goods experienced a decline in prices, reflecting subdued demand for discretionary goods amidst the prevailing high inflationary environment.

Growth in Australia is clearly slowing down. The increase in Q1 was slower than any of the growth seen in the 2022 quarters. Household consumption has clearly become constrained as a result of the financial tightening from rate hikes over the past year, and if it were not for public investment, fixed capital formation would have likely been negative. The outlook for the rest of the year is dim. This report confirms NAB’s weak growth outlook for the full year of 2023 at 0.7%. It also presents a real problem for the Reserve Bank of Australia which must deal with persisting price pressures at the same time as sluggish growth.

Still to come…

10:00 am (EST) - Bank of Canada Announcement

10:30 am - EIA Petroleum Status Report

3:00 pm - US Consumer Credit

7:50 pm - Japan GDP

9:30 pm - Australia Trade

Morning Reading List

Other Data Releases Today

German industrial production grew 0.3% MoM and 1.6% YoY in April. Production in the 3 month period to April was 1.6% higher than the previous 3 months. Energy-intensive production is still falling, down -1.1% MoM.

Italy's retail sales (volume) fell -0.2% MoM and -4.8% YoY in April. In value terms, sales increased 0.2% MoM and 3.2% YoY. Food sales grew 0.6% MoM while non-food sales fell -0.7% MoM. Both are down on an annual basis.

The UK Halifax House Price Index was flat MoM in May and down -1.0% YoY.

This is the first time since 2012 that prices have fallen on an annual basis.

The US trade deficit increased 23.0% MoM to $74.6 bil as exports fell -3.6% MoM and imports increased 1.5% MoM. The decline in exports was a result of a large decrease in energy exports, crude oil exports down -$2.1 bil and fuel oil exports down -$1.3 bil.

Canada's trade balance increased to a surplus of $1.9 bil in Apr with exports up 2.5% MoM and imports down -0.2% MoM. Exports of metal and non-metallic mineral products (+13.6%) contributed the most while imports of energy products (-12.8%) contributed the most to the decrease.

German Industrial Production

German industrial production remains weak in April (ING) - With another rebound that was too weak to bring any substantial relief, industrial production increased by a meagre 0.3% month-on-month in April. Without any significant pick up in activity, the German economy's recession could continue in the second quarter.

Australia GDP

Australian Economic Update: Q1 GDP 2023 (NAB) - GDP rose by 0.2% q/q (2.3% y/y) – in line with our expectations and a touch softer than market and RBA forecasts (consensus 0.3%). The expenditure side was in line with partials and continues to paint a picture of soft consumption growth and weakening housing construction, with increasing evidence that higher rates and inflation are weighing on spending.

RBA Announcement

FX Update: RBA surprises hawkish again, extending AUD gains (Saxo Bank) - The Australian dollar jumped overnight on Australia’s RBA surprising for the second time in a row with a 25-basis point rate hike and guiding for more possible hikes at coming meetings. This has taken AUDUSD to pivotal levels while the US dollar remains firm elsewhere, particularly against the European majors.

Europe

ECB Preview: Don’t look back in anger (ING) - A 25bp rate hike looks like a done deal for next week’s European Central Bank meeting. However, with growth disappointing, the economic outlook getting gloomier and inflation dropping, arguments for several more rate hikes are becoming weaker. That said, the ECB is likely to ignore this.

The right to work versus the right to retire (Allianz) - Ageism is still pushing older workers out of the labor market: In the EU only 51% of the population aged between 60 to 64 is still active on the labor market. The main causes are difficulties to find an adequate job and long-term unemployment in higher ages since negative stereotypes about older workers persist.

Industrial producer prices down by 2.9% in April 2023 (Eurostat) - In April 2023, industrial producer prices in the EU domestic market fell by 2.9% compared with March 2023. The decrease followed a series of producer price reductions that started in the autumn of 2022. Total prices have fallen by 9.4% since September 2022. These price decreases only partly compensated for the massive increases that had taken place between early 2021 and September 2022.

Wage pressures keep global inflation elevated, most notably in the UK, but goods prices fall (S&P Global) - Inflationary pressures eased globally in May, according to the latest PMI survey data, though remained elevated thanks principally to wage pressures. Price rises were hence more widely seen in the labour-intensive services economy, but selling prices fell in manufacturing for the first time in three years. Especially stubborn selling price pressures were seen in the UK, while - at the other end of the scale -prices fell in mainland China.

National Bank of Poland leaves rates unchanged, focus on tomorrow’s press conference (ING) - The National Bank of Poland rates and statement after the June Monetary Policy Council meeting were unchanged. More information should come from tomorrow's conference by the central bank president. We expect a slightly more dovish stance.

The Dutch Economy Chart Book: Large revision, but same view (ING) - Our Dutch Economy Chart Book provides an overview of the many important business cycle developments of the Dutch economy in more than forty visuals. Download this new edition below.

Australia

Why rents are going up and when they will stop (NAB) - Advertised rents have been rising rapidly since late 2020 and currently show few signs of slowing. Rents in the CPI, which reflect average rents paid by all renters, not just the cost of new rental agreements, have now also accelerated. As higher new rents continue to be reflected in the stock of outstanding rents, CPI rents look set to accelerate to around 10% y/y and supporting overall inflation prints well into 2024.

Energy

Crude oil sees quick reversal of Saudi-cut pump (Saxo Bank) - Crude oil trades softer despite Sunday's OPEC+ meeting where Saudi Arabia announced they would make a unilateral cut of one million barrels per day, so far only in July. A decision that on paper should be mildly positive but the subsequent price action highlights the current focus on demand worries, and while the cut may support a floor under the market, the upside potential remains limited.

Banking

Macro and business risks from a credit crunch (EY Parthenon) - In the wake of recent banking sector stress, elevated bank funding costs and deposits volatility are likely to keep pressure on small and mid-sized banking institutions, leading to tighter credit conditions. This, in turn, will constrain consumer spending and weigh on business investment decisions. We estimate that the cumulative tightening in credit conditions will represent a drag on the US economy worth around 0.4% of GDP over the next year.

Banking risk monthly outlook: June 2023 (S&P Global) - The loan to deposit ratio (LDR) in mainland China increased to 83% when last reported in 2022. The rise in the LDR from 80% (2019) before the pandemic was due to the loan prime rate (LPR) cut and the cut back from cautionary savings as the economy reopened.

Real Estate

Single-Family Construction Slowdown Less Pronounced in Lower Density Markets (NAHB) - While single-family home building has slowed significantly from pandemic-fueled highs because of higher interest rates and construction costs, the slowdown is less pronounced in lower density markets. On the other hand, multifamily market growth remained strong throughout much of the nation, according to the latest findings from the National Association of Home Builders (NAHB) Home Building Geography Index (HBGI) for the first quarter of 2023.

Markets

Fixed Income Is Now a Buyer’s Market (Guggenheim) - The tightening cycle has brought about a regime shift that we believe is likely to continue to benefit fixed-income investors for the foreseeable future. The era of low levels of interest rates and borrowing terms favoring shareholders over lenders seems behind us. The subsequent recapturing of economics and negotiating leverage by creditors is just beginning. The shift in this dynamic, combined with wide spreads and higher yields, has dramatically improved the value proposition of credit investments.

Little growth, much uncertainty, decent returns (DWS Group) - Over a twelve-month horizon, we expect decent overall returns across many asset classes despite lackluster economic growth and sticky inflation.

Outlook

Our forecasts: Still waiting for the recession (DWS Group) - DWS Group Q2 2023 updated forecasts.

What Goes Up Must Come Down (Northern Trust) - Senior Economist Ryan Boyle anticipates when central banks will see fit to cut interest rates.

Subscribe to receive Econ Mornings every weekday at 9 am. More economic and finance content on Twitter, Reddit, and my website.