CFNAI Stabilizes at Slight Contraction in March Which Shouldn't Derail Strong Q1 GDP

Economic news and commentary with April 24, 2023

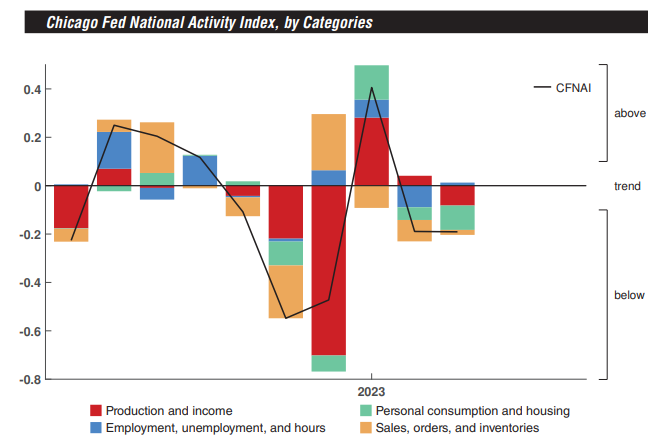

US Chicago Fed National Activity Index

After a strong January, economic indicators pointed to a cooling of the economy in February and March. The Chicago Fed National Activity Index was -0.19 in March which was unchanged from February. Once again, the sub-indexes painted a mixed picture of business activity that was more-or-less slightly below trend in March. The strongest group of indicators, and the only positive, was employment at 0.01 which increased from -0.09 after the strong March jobs report which saw the unemployment rate fall further. Sitting at 3.5% now, the jobless rate indicates that the labor market remains tight, but there are other leading signals that suggest Q2 will see some of that tightness unwound. The sales, orders & inventories category also saw improvement but remained slightly negative at -0.02.

The two categories that declined in March were production, down -0.12 pts to -0.08, and consumption, down -0.05 pts to -0.10. The major indicators dragging down these two subindexes include manufacturing production which fell -0.5% MoM after an 0.4% MoM increase in February, and new and existing home sales which continued to reflect the frailty in real estate. The consumption subindex would probably be higher if it weren’t for the weakness in the housing sector which has notably diverged from other areas of the economy. In particular, we see that retail sales and personal consumption data have proven to be resilient despite the rise in interest rates. This is especially the case in January data. Backward-looking indicators have led to a sharp upward revision in the 1st month’s CFNAI reading, from 0.23 initially estimated to 0.41 in the March release. This suggests Q1 GDP growth could surprise to the upside in this week’s release.

Still to come…

10:30 am (EST) - US Dallas Fed Manufacturing Survey

Morning Reading List

Other Data Releases Today

The Ifo Business Climate Germany grew to 93.6 in April, up from 93.2 in March. The Situation index edged down -0.4 pts to 95.0, and the Expectations index increased 1.2 pts to 92.2. The service sector index fell -2.0 pts to 6.8.

German Ifo

German Ifo improves marginally in April (ING) - An improving Ifo index is always good news. However, a weaker current assessment component and below-average expectations do little to take away the stagnation risk for this year.

Flash PMIs

PMIs continue to show a two-speed economy (Danske Bank) - April Flash PMIs continued to show a picture of a two-speed economy, with euro area manufacturing index remaining on contractionary territory, but with services sector driving the composite index to a 11-month high (54.4). We think the ECB is more concerned about the latter due to the close link to wage dynamics, and continue to look for a 50bp hike in the May meeting.

Eurozone flash PMI signals strong start to second quarter thanks to resurgent service sector (S&P Global) - Eurozone business activity growth accelerated to an 11-month high in April according to the latest flash PMI survey data, indicating that the economy has gained further growth momentum at the start of the second quarter.

US flash PMI signals further acceleration of economic growth in April, but resurgent demand also brings higher price pressures (S&P Global) - The latest PMI survey data from S&P Global adds to signs that business activity has regained growth momentum after contracting over the seven months to January.

Eurozone PMIs give mixed signal but not inconsistent with cooling economy (ABN AMRO) - The flash estimates of the eurozone PMIs for April show a mixed picture. Whereas the manufacturing PMI dropped sharply lower and moved further into contraction territory, the services PMI increased and jumped further into expansion territory. The services PMI has never been this far above the manufacturing PMI since the start of the series in 1998. We think that the normal cyclical drivers will soon start to have a downward impact on activity in the services sector and we still expect GDP to contract modestly during most quarters this year.

US

A Downturn Is Still in the Cards (Wells Fargo) - Data released this week support our expectations for a recession in the second half of the year. The LEI continued to flash contraction as early signs of labor market weakening are starting to emerge. Meanwhile, a batch of housing data confirmed that a full-fledged housing market recovery is still far off.

Strike One! (BMO) - Just two weeks ago, we intoned that cracks were forming in the foundation of the global expansion. Well, those cracks are still mostly of the hairline variety. True, there are increasing indications that the U.S. economy is losing momentum, but next week’s GDP report is likely to reveal a respectable 2% pace for Q1 growth.

The other government shutdown (CIBC) - The government shutdown we should be fretting over is the potential one in Washington, should Congress and the White House fail to reach a deal over raising the debt ceiling. Not only would it impact a much larger share of the civil service, it would also raise fears of an outright default, bringing a period of volatility in global debt markets.

Out of Office (Northern Trust) - A reckoning has been a long time coming. Even before the pandemic, office real estate had slack capacity in many cities. During the 2020 crisis, I started tracking monthly reports from commercial real estate (CRE) data aggregators, watching for evidence of falling rents or higher office vacancies.

Employment Situation in March: State-Level Analysis (NAHB) - Nonfarm payroll employment increased in 36 states and the District of Columbia in March compared to the previous month, while 14 states lost jobs. According to the Bureau of Labor Statistics, nationwide total nonfarm payroll employment increased by 236,000 in March, following a gain of 326,000 jobs in February.

Understanding Monetary Policy Through the Housing Channel (Patrick Harker, Philadelphia Fed) - The Chicago Fed President discusses the impact of monetary policy on the housing sector of the economy.

Welcoming remarks at Fed Listens: Transitioning to the postpandemic economy in the Permian Basin (Dallas Fed) - Dallas Fed President Lorie Logan delivered these remarks April 20, 2023, at the Fed Listens event at Odessa College in Odessa, Texas.

Tracking the Fallout from Bank Stress (BMO) - With the risks of imminent bank failures fading, markets have settled down, but that doesn’t mean the economy is off scot-free. Here’s what to look for to track the situation and its impact on the U.S. economy.

Bank Stress and Lending Standards (Northern Trust) - The banking problems that dominated the news last month have largely faded into the background. Analysts are watching first-quarter earnings reports from the industry, looking for further signs of weakness, but the risk to the financial system seems to have eased.

Texas’ cheap housing edge slipping away as resilient demand outpaces supply (Dallas Fed) - Texas home prices have headed steadily higher, a byproduct of rising housing demand and pandemic-related supply shortages. More recently, tightening monetary policy has led to surging mortgage rates and added to homebuyer costs in the state and across the country.

Canada

Canada's Slowly Approaching Economic Slowdown (Wells Fargo) - Canada's economy has made a solid start to 2023, with sturdy employment gains over the last six months and monthly GDP figures pointing to respectable growth in the first quarter. However, the cumulative effects of past monetary tightening and lower energy prices should, together, weigh on consumer and business activity going forward. We forecast 1.0% GDP growth in 2023, down from 3.4% in 2022.

Japan

Bank of Japan Preview: Risk of tightening too soon still dominates (Danske Bank) - We do not expect any changes to monetary policy on the new Governor Ueda’s

first monetary policy meeting on 28 April. Inflationary pressures seem persistent, especially fuelled by stronger-than-expected wage growth, which could pave the way for the BoJ to at least tweak the Yield Curve Control (YCC) on either the June or the July meeting.

Emerging Markets

Emerging Market Vulnerabilities (Northern Trust) - The combination of rising debt servicing costs, low reserves and softer growth could lead to a systemic debt crisis in the developing world. Several developing economies are facing sovereign credit spreads above 1,000 basis points, a sign of distress. According to the IMF, 17% of low-income economies are already in debt distress and 39% are estimated to be at high risk.

Inflation

The Inflation Battle Continues (BMO) - Nearly two months have gone by since SVB collapsed and CS folded into the arms of its big competitor. Markets have calmed significantly and monetary policymakers have turned their full attention back to more mundane matters, such as inflation.

Outlook

US and eurozone GDP to help guide recession risks (S&P Global) - Insights into economic growth in the first quarter will be the highlights of the coming week, as both the US and eurozone publish advance GDP estimates. The US economy is expected to have slowed slightly from the 2.6% annual rate of increase seen in the fourth quarter, with the consensus at 2.0% and our tracker at 1.9%.

Central banks: Our latest calls ahead of a dramatic month (ING) - The most aggressive central bank tightening cycle for decades is reaching its finale. This is our definitive guide to global central banks as we enter another round of crucial meetings over the next few weeks.

Research

International Diversification, Reallocation, and the Labor Share (Chicago Federal Reserve) - How does growing international financial diversification affect firm-level and aggregate labor shares? We study this question using a novel framework of firm labor choice in the face of aggregate risk. The theory implies a cross-section of labor risk premia and labor shares that appear as markups in firm-level data.

Jointly Estimating Macroeconomic News and Surprise Shocks (Dallas Fed) - This paper clarifies the conditions under which the state-of-the-art approach to identifying TFP news shocks in Kurmann and Sims (2021, KS) identifies not only news shocks but also surprise shocks. We examine the ability of the KS procedure to recover responses to these shocks from data generated by a conventional New Keynesian DSGE model. Our analysis shows that the KS response estimator tends to be strongly biased even in the absence of measurement error.

Debt Maturity and Commitment on Firm Policies (Dallas Fed) - If firms can issue debt only at discrete dates, debt maturity is an effective device against the commitment problem on debt and investment policies. With shorter maturities, debt dynamics are less persistent and more valuable because upward leverage adjustments are faster and long-run leverage lower.

State-Dependent Local Projections (Dallas Fed) - Do state-dependent local projections asymptotically recover the population responses of macroeconomic aggregates to structural shocks? The answer to this question depends on how the state of the economy is determined and on the magnitude of the shocks. When the state is exogenous, the local projection estimator recovers the population response

regardless of the shock size.

Markets

Earnings Season Brings Mixed Winds (BMO) - Equity markets were mixed this week, and all eyes are on the Q1 earnings season with notable hits (big banks) and misses (Tesla) already on the books. Based on the latest tally from Refinitiv, S&P 500 earnings are expected to fall 5% y/y in the quarter, marking a second consecutive quarter below year-ago levels.

Green

US electric vehicle market set for sustained growth despite stricter subsidy rules (ING) - Despite tougher rules for tax credits, US electric vehicle sales (including plug-in hybrids) are expected to grow to 1.4mn in 2023, accounting for 10% of total light-duty vehicle sales. This puts the US EV market in a better position to achieve the 2030 ‘step-up scenario’ we’ve outlined, but it will take time to form a mature domestic EV value chain.

Subscribe to receive Econ Mornings every weekday at 9 am. More economic and finance content on Twitter, Reddit, and my website.