China's Weak Start to Q3 Means More PBoC Easing

Economic news and commentary for August 15, 2023

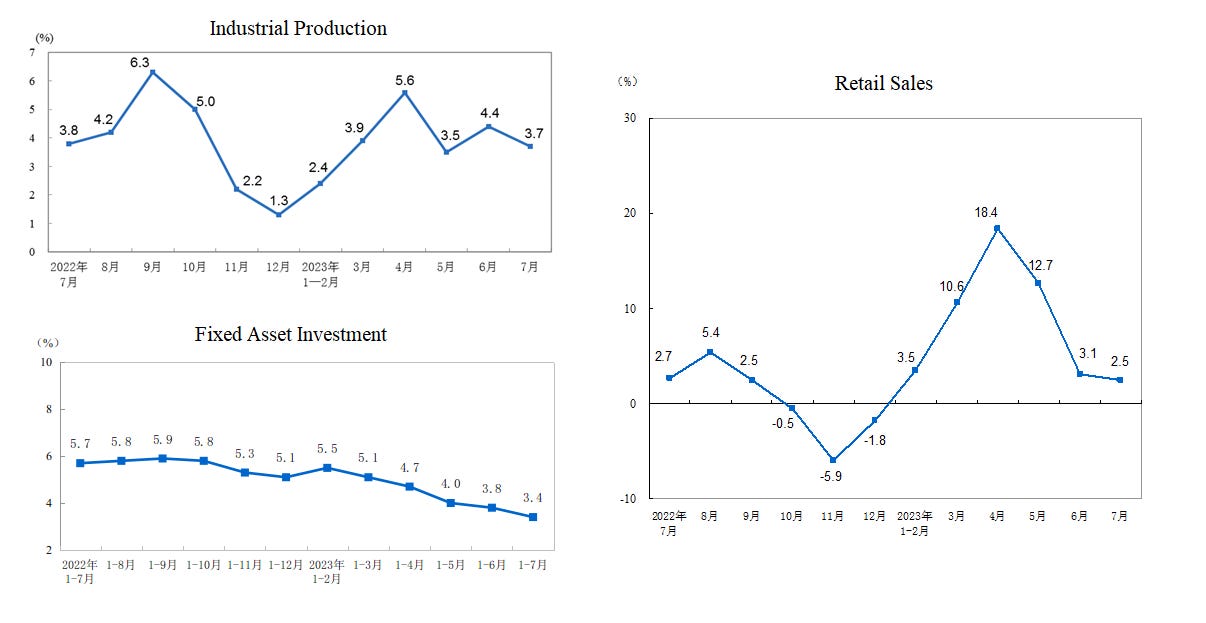

China Economic Data

The month of July saw China's industrial production remaining relatively stagnant, with a marginal 0.01% MoM growth and a YoY increase of 3.7%. This figure represented a slight dip from the 4.4% YoY growth observed in the preceding month of June. While manufacturing production maintained a moderate upward trajectory, registering a 3.9% YoY growth, the high-tech manufacturing segment showed a relatively modest growth rate of only 0.7% YoY. A major downtrend in the semiconductor and computer industries continues to impact the latter segment of production.

In the metals industry, China displayed signs of rebound, with ferrous metal smelting and non-ferrous smelting witnessing robust YoY growth rates of 15.6% and 8.9% respectively. These encouraging figures suggest pockets of resilience within the metals sector, even as the broader global economy slows. However, these areas of production are coming off of low bases which could be inflating the numbers a bit. The electrical machinery manufacturing sector remained strong, with a substantial YoY growth of 10.6%; however, the electronics equipment manufacturing segment, including semiconductor production, struggled, with a meager 0.7% YoY growth. Again, the latter low rate of growth is being impacted by weak semiconductor demand. The strength in metals production was also evident in the output of crude steel and steel. Both recorded YoY growth rates exceeding 10%.

Once again, we also see China’s investment in renewable manufacturing emerging as a noteworthy source of growth within the industrial landscape. "New energy vehicles" output surged by an impressive 24.9% YoY, while solar cells output and power generation equipment also recorded remarkable YoY growth rates of 65.1% and 15.7% respectively. However, the semiconductor sector faced significant headwinds, with semiconductor output witnessing a staggering -22.3% YoY decline.

Amidst mixed production data, China's national fixed asset investment demonstrated only a modest YoY growth of 3.4% in the year-to-date period through July. This figure represents a decrease from the 3.8% YoY growth observed in June. Of note is the negative YoY growth of -0.5% in private investment, reflective of liquidity challenges within China's financial system. Contrasting with this private sector trend, state-owned businesses maintained robust investment growth at 7.6% YoY. This growth can be attributed to the Chinese government's continued support for the economy through fiscal and monetary measures. The real estate sector's struggle was evident in its investment figures, with a significant YoY decline of -8.5% in the year-to-date period through July. This decline marked the weakest performance since September of the previous year, highlighting the continued challenges faced by the real estate market. In response to these challenging investment trends, the People's Bank of China (PBoC) took an unexpected step to ease the situation, cutting its medium-term lending facility rate by 15 basis points to 2.50%.

Finally, we turn to an update on the Chinese consumer. Retail sales growth experienced a minor setback in July. MoM growth dropped to -0.06%, and YoY growth dipped from 3.1% to 2.5% compared to June. The 2.5% YoY growth disappointed the consensus forecast of 4.4% YoY by a large margin. While food and beverage revenue continued to exhibit strength, growing at an impressive 15.8% YoY, certain sectors faced significant challenges. Jewelry sales plummeted by -10.0% YoY, office supplies witnessed a decline of -13.1% YoY, and building materials sales contracted by -11.2% YoY. Even sales in daily necessities experienced a decrease of 1.0% YoY. Weakness in these areas suggests that the post-pandemic-fueled rebound is basically over, and Chinese households are returning to more normal patterns of spending.

In general, the Chinese economy entered Q3 2023 with little hope that the underwhelming first half of the year can be reversed. While certain areas of manufacturing show some resilience, most grapple with economic headwinds that have been blown by the central banks abroad. The Chinese government's support measures and adaptive policies will play a pivotal role in trying to flip the current trends, but so far, its efforts have been futile.

Still to come…

10:00 am (EST) - US Business Inventories

10:00 am - US Housing Market Index

Morning Reading List

Other Data Releases Today

Japan’s GDP grew 1.5% QoQ in Q2 2023 after a solid 0.9% QoQ increase in Q1 2023. However, domestic demand fell -0.3% QoQ with a -0.5% QoQ drop in consumption and a 0.3% QoQ increase in public demand. The strong growth was spurred on by exports jumping 3.2% QoQ and imports falling -4.3% QoQ.

Australia’s Wage Price Index grew 0.8% QoQ and 3.6% YoY in Q2 2023, down from 3.7% YoY in Q1 2023. Private sector wages saw the strongest growth of 0.8% QoQ and 3.8% YoY. The share of jobs receiving wage rises of between 4 to 6% (3.3%), continued to grow and is now at the highest level since 2009.

The UK unemployment rate increased 0.3 ppts to 4.2% in Q2 2023 and is now up 0.2 ppts from the pre-pandemic period. The employment rate edged down slightly while the inactivity rate also fell, down -0.1 ppts to 20.9%. Job vacancies continued the long descent to a more normal level, down -66,000 to 1.02 million. Despite the easing in employment trends, the annual growth in regular pay (ex-bonuses) was 7.8% YoY, the highest wage growth since 2001.

The ZEW Indicator of Economic Sentiment for Germany improved to -12.3 in August, an increase of 2.4 pts. Meanwhile, the Economic Situation Germany index crashed -11.8 pts to 71.3 which is the weakest since October 2022.

Retail sales grew 0.7% MoM and 3.2% YoY in July, up from 2.3% YoY in June.

Nonstore: 1.9% MoM

Sporting Goods: 1.5% MoM

Food Services: 1.4% MoM

Clothing: 1.0% MoM

Furniture: -1.8% MoM

Electronics: -1.3% MoM

Canada's CPI grew 0.6% MoM and 3.3% YoY in Jul, up from 2.8% YoY in Jun.

Core CPI: 3.4% YoY (0.5% MoM)

Food: 7.8% YoY (0.4% MoM)

Energy: -8.2% YoY (1.7% MoM)

Goods: 2.3% YoY (0.2% MoM)

Services: 4.3% YoY (1.0% MoM)

US import prices grew 0.4% MoM but were down -4.4% YoY in July, export prices grew 0.7% MoM but were down -7.9% YoY. Fuel import prices posted the second strong gain in a row, up 1.9% MoM in June and 3.6% MoM in July.

The Empire State Manufacturing Survey Business Conditions index fell -20 pts to -19.0 in August. New orders and shipments both saw drops that were worse than -20 pts to -23.2 and -25.7. Prices received jumped 8.7 pts to 12.6.

China Economic Data

China’s Economy at a Glance – August 2023 (NAB) - Weakness in China’s economy that was evident in Q2 has continued into July, with indicators of domestic demand subdued, the real estate sector remaining a headwind and demand for China’s goods in export markets continuing to soften. The highly likely modest cut to the PBoC’s policy rate later this month (having cut its MTF rate in mid-August) is unlikely to provide much of a boost, given already lacklustre loan demand. While our forecasts for China’s growth are unchanged this month – 5.2% for 2023, 4.5% for 2024 and 4.8% for 2025 – risk in the near-term is becoming increasingly weighted to the downside, with a growing chance of China missing its 5% target this year.

China: PBoC cuts rates amidst data weakness (ING) - The market was expecting the PBoC to wait until September before easing again, and today's cuts suggest that the authorities' concern about the state of the macroeconomy is mounting. But that doesn't mean that they are about to undertake unorthodox policy measures.

UK Employment

Surprise UK wage growth pick-up helps cement September hike (ING) - There are growing signs that the UK jobs market is softening, but for now the Bank of England will remain focused on stubbornly high wage growth. A September hike is highly likely, but November is more of a question mark.

US

Panic or Panacea?: The Economic Impact of Artificial Intelligence, Part III: The Labor Market and Income (Wells Fargo) - Past technological breakthroughs have brought with them concerns about new technology's impact on the labor market. Artificial intelligence has sparked another such wave of anxiety today, as large language models (LLMs) such as ChatGPT have led to new fears about the future of employment in a world of widely adopted generative AI. Will generative AI displace large numbers of workers, and what will happen to living standards for the average American worker?

The Federal Reserve’s Two Key Rates: Similar but Not the Same? (Liberty Street Economics, NY Fed) - Since the global financial crisis, the Federal Reserve has relied on two main rates to implement monetary policy—the rate paid on reserve balances (IORB rate) and the rate offered at the overnight reverse repo facility (ON RRP rate). In this post, we explore how these tools steer the federal funds rate within the Federal Reserve’s target range and how effective they have been at supporting rate control.

Gauging the Fed’s Current Tightening Actions: A Historical Perspective (St Louis Fed) - At the conclusion of their July 26, 2023, meeting, the Federal Open Market Committee (FOMC) voted to raise the target range of the federal funds rate by 25 basis points to 5.25% to 5.50%. This blog post will examine the magnitude of the FOMC’s current actions relative to those since 1983 and, importantly, whether monetary policy has moved into restrictive territory.

How Far Is Labor Force Participation from Its Trend? (San Francisco Fed) - Labor force participation in the United States has dropped a percentage point since the pandemic began. Analyzing how participation has evolved for various groups of the population suggests that more than two-thirds of this decline has been due to persistent “trend” factors. The remainder is due to temporary economic conditions, or “cyclical” factors. Estimates project that trend factors—driven largely by population aging—could push labor participation down an additional percentage point over the next decade.

An Age of Fiscal Limits (First Trust Portfolios) - The US is on the cusp of some very big budget challenges. If policymakers don’t address entitlement spending, expect worse budget news in the years ahead. Whether voters actually hold politicians’ feet to the fire will determine whether the US becomes another Argentina, or France, or finds its way back to the fiscal sanity as it has in the past.

Europe

Polish CPI inflation falls; a rate cut is surely coming (ING) - The decline in Polish CPI inflation is set to continue, supported by a rapid unwinding of external supply shocks. And that should allow the central bank to cut rates by 50-75bp in 2023. However, the slow decline in core inflation compared with the rest of the region suggests that the second stage of disinflation will be difficult.

China

China holiday wrap-up - part 3 - Risks of a financial crisis resurface (Danske Bank) - The past weeks saw another turn in sentiment on China as property stress resurfaced, signs of shadow banking problems appeared and economic data disappointed. The new financial challenges is a blow to China's efforts to restore confidence and lift private demand and it highligts downside risks to growth in coming quarters.

Canada

An Easier Quarter for Lending Conditions (BMO) - Lending conditions eased in Q2 as the Bank of Canada paused its rate hike campaign until the end of the quarter. A lack of meaningful tightening suggests that any spillover effect from the early-year U.S. banking sector stress was muted, at least initially. Still, we expect credit conditions to tighten again in the third quarter, reflecting the Bank’s two latest rate hikes.

Australia

The Forward View – Australia: August 2023 (NAB) - With inflation moderating more than expected in Q2 and further evidence of activity slowing, we now see only one more rise in the cash rate, taking the peak to 4.35% – most likely in November. Our forecasts for GDP growth have strengthened marginally, reflecting stronger Q2 exports, but we nonetheless continue to expect growth to be well below trend at 0.7% y/y in 2023 and 0.9% y/y in 2024.

Mexico

Mexico as a supply chain reshoring leader (S&P Global) - Mexico has been a leader in reshoring of manufacturing both out of the US and away from mainland China. There's plenty of evidence of reshoring over the past five years, but success in the future is by no means guaranteed given stiff competition from other countries including Vietnam.

Inflation

Inflation Monitor for August 14 (BMO) - U.S. consumer prices rose modestly in July, increasing the probability that the Fed can restore price stability without sparking a recession.

FX

FX Talking August: The dollar’s still got the groove (ING) - High US rates, a surprisingly strong US domestic economy, and a soft overseas investment environment have all combined to keep the dollar strong this summer. It is hard to see this changing much over the coming months, but by the fourth quarter, we think there will be enough evidence of a US slowdown for the dollar to be embarking on a bearish trend.

Markets

Is the Inverted Yield Curve a Broken Signal or Is a Recession Still Coming? (First Trust Portfolios) - The ROI podcast discusses some of the most important questions facing investment professionals today.

Research

Postpandemic Nominal Wage Growth: Inflation Pass-Through or Labor Market Imbalance? (Clevaland Fed) - Measures of wage growth have increased substantially during and after the pandemic compared to their average levels in the decade before. Does higher wage growth reflect compensation for a higher cost of living, brought about by an increase in inflation in the past two years? Or has an imbalance between strong labor demand and restrained labor supply lifted wage growth? Using a new empirical wage Phillips curve model, we find that the increase in wage growth largely reflects the pass-through of higher inflation and does not reflect labor market imbalances. The model forecasts a decline in wage growth to about 3 percent annually by 2025.

Looking for a way to take advantage of higher interest rates? I recommend SoFi’s high-yield savings account which has a yield of 4.5% (subject to change) and includes FDIC deposit insurance for both its checking and savings accounts just like a traditional bank. Use my referral link to get a sign-up bonus and start earning that rate today. (This is also a great way to support me since I get a bonus too!)

Subscribe to receive Econ Mornings every weekday at 9 am. More economic and finance content on Twitter, Reddit, and my website. You can also see my feed on the PiQSuite platform as a partnered feed.