Deflation in China Points to Struggling Economic Recovery

Economic news and commentary for May 11, 2023

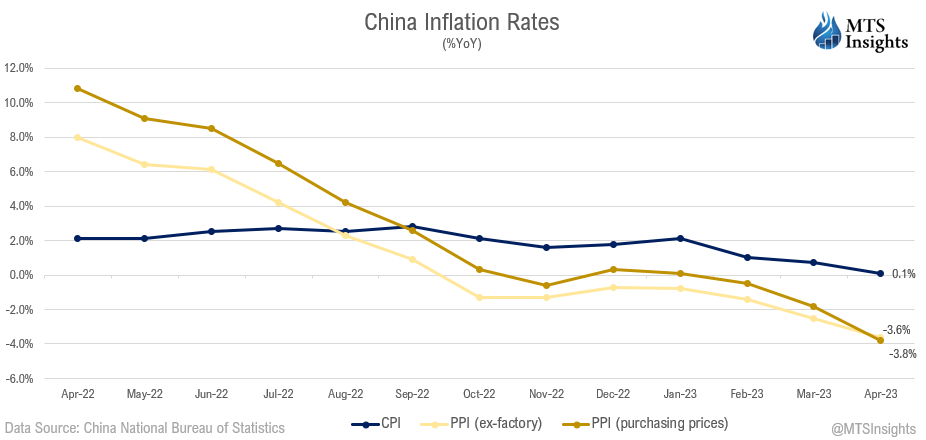

China CPI & PPI

China's inflation figures for April were released today, and the data came in worse than expected. The country's CPI edged down by -0.1% MoM and increased by just 0.1% YoY. This is a notable decline from the previous month, where CPI had risen by 0.7% YoY. When looking at core CPI, which does not factor in energy deflation, the figures were slightly higher, showing a YoY increase of 0.7%. Despite this, the decline in energy prices was evident across several categories. Gas prices fell by -1.6% on a monthly basis and a staggering -10.4% YoY. These prices indicate the sharp decline in energy prices and the effects it has on inflation. The decline in energy prices is also evident in the PPI for oil and gas extraction, which fell by -16.3% YoY, and fuel and power purchasing prices, which were down by -5.3% YoY. In general, mining and raw material producer prices were weak for producers, with coal prices down by -9.3% YoY, and ferrous metal prices down by -10.8% YoY.

Turning to other categories, food prices edged down by -0.2% MoM, but it was still one of the strongest categories, increasing by 1.1% YoY. Consumer goods prices (which do include some of the weak energy indexes) were even weaker, with a YoY decline of -0.4%. The PPI for daily necessities and consumer durables were both pretty inconsequential on the month. The former saw no growth and was only up 0.4% MoM while the latter fell -0.3% MoM and -0.6% YoY. Services prices have maintained some inflation, up by 0.3% MoM and 1.0% YoY. Travel played a big part in the rise in services prices, up by 4.6% MoM and 9.1% YoY.

The two reports suggest that a global slowdown is having a significant impact on how Chinese firms price their goods. The sluggishness of exports also provides evidence of this. The recent downside surprise in imports hints that domestic demand for goods is not that great either. The main thing driving the economy and thus prices is the reopening effects that are still having a major impact after restrictions were lifted at the end of last year. At this point, it seems that half of the Chinese economy is working against it. Industrial and manufacturing weakness is clashing with the expansion of services that were closed during the pandemic. In this dynamic, the momentum needed to stage a strong economic rebound in 2023 is unlikely to develop, and Q2 2023 GDP growth is probably going to be disappointing.

Still to come…

10:30 am (EST) - EIA Natural Gas Report

4:30 pm - US Fed Balance Sheet

Morning Reading List

Other Data Releases Today

The Bank of England increased its Bank Rate by 25 bps to 4.5% by a vote of 7-2 with two members opting to pause. The Bank indicates that its projections are based on a Bank Rate that "peaks at around 4.75% in 2023 Q4 and ends the forecast period at just over 3.5%."

US PPI grew 0.2% MoM and 2.3% YoY in April, down from 2.7% YoY in March. Core PPI was up at a stronger 3.4% YoY but, on the month, saw an identical increase of 0.2% MoM. Processed and unprocessed goods prices were both still declining, -3.2% YoY and -19.2% YoY. Services prices increased faster than the headline pace, up 0.7% MoM, but the annual pace fell -0.2 ppts to 4.5% YoY.

Jobless claims grew 22,000 to 264,000 last week. The insured unemployment rate was unchanged at 1.2%. Continued claims grew 12,000 to 1.81 million.

Bank of England Announcement

Bank of England: First to hike, last to pause and pivot (Allianz) - As expected, the Bank of England increased interest rates by +25bps today, but it will have to contend with stickier-than-expected inflation ahead. In March, inflation hit 10.1% in the UK, higher than in all other Western European countries, as well as the US. Easing food prices and normalizing supply chains, as well as negative base effects from energy prices, will bring inflation down to 4% by Q4 2023. By end-2024, we expect inflation at 2.5% y/y but this will still be 0.5% higher than the level in the US.

Bank of England hikes rates and keeps options open for further increases (ING) - The BoE has hiked rates by another 25 basis points and kept the door open to more if inflation data come in higher than expected between now and the next meeting in June. Another hike is possible, but with inflation forecasted to be well below target in a couple of years' time, we think this tightening cycle is reaching its limit.

US CPI

April CPI: No Major Surprises (Wells Fargo) - The April CPI report was largely in line with forecasters' expectations. The 0.4% increase in both the headline and core CPI pointed to an inflation backdrop that is improving incrementally rather than rapidly. Falling prices at the grocery store and for energy services helped to offset an increase in gasoline prices in April, while an outsized jump in used auto prices was similarly tempered by declines in prices for travel-related services such as airfares and lodging away from home.

US inflation continues to run too hot, but there are glimmers of hope (ING) - Another 0.4% MoM print for core CPI means that inflation is still running far too hot for the Federal Reserve to relax. Nonetheless, there are some signs that service sector price pressures are moderating so a June Fed pause look likely. With corporate pricing power flagging and shelter costs topping out, we could see core CPI in the 2-3% range by year-end.

U.S. CPI: Supercore Cools Off (BMO) - There's a little something in the CPI report for both FOMC hawks and doves. The still meaty core price increase (with its 5.1% annualized 3-month rate) will dissuade any thoughts of near-term rate cuts. However, signs of cooler services inflation should support a rate pause in June, and, we suspect, the remainder of the year.

It’s sticky and bumpy, but make no mistake, inflation is cooling (EY Parthenon) - Headline Consumer Price Index (CPI) rose 0.4% month over month (m/m) in April, in line with expectations, following an energy constrained 0.1% gain in March. Energy prices rebounded 0.6% on higher gasoline prices as electricity and utility gas prices fell, while food prices were unchanged for the second consecutive month — the softest back-to-back readings since mid-2019.

Inflation remains stubbornly elevated, but April data shows encouraging signs (TD Bank) - There were definitely some encouraging signs in this morning's CPI numbers. The continued deceleration in shelter costs suggests that we are starting to see some passthrough from last year's pullback in rental rates, which should continue for the next several months. Meanwhile, price growth across non-housing services decelerated to its slowest month-on-month pace of growth in nearly two years.

US CPI (Apr): markets find reason to cheer, but a long road ahead (CIBC) - Investors dug into the US inflation data and found reason to cheer, but taken as a whole, the latest figures still showed a long road to get to where the Fed wants to be. The headlines were hardly rosy. Higher prices at the pump meant that overall price pressures picked up momentum once again, despite a second consecutive month of flat food prices.

US inflation stays firm, even as recessionary forces build (ABN AMRO) - Inflation remained elevated in April, even as weakening credit conditions point to a looming recession.

Inflation Falls Below 5% For First Time in Two Years (NAHB) - Consumer prices in April saw the smallest year-over-year gain since April 2021. This marked the tenth consecutive month of deceleration and the first time the rate has fallen below 5% in two years. While the shelter index (housing inflation) experienced its smallest monthly gain since January 2022, it continued to be the largest contributor to the total increase, accounting for over 60% of the increase in all items less food and energy.

The Consumer Price Index (CPI) Rose 0.4% in April (First Trust Portfolios) - Headline inflation re-accelerated in April after a lull in March, and readings remain well above the Fed’s 2% inflation target. For the most volatile categories, energy prices rose 0.6% in April while food prices remained unchanged for a second month in a row. Stripping out these components shows “core” prices rose 0.4% in April, matching consensus expectations. Core prices have risen 5.5% in the past year and have not budged lower on a year-ago basis since the start of 2023.

Europe

Euro Area Macro Monitor - Core inflation easing yet service price pressure still persists (Danske Bank) - Preliminary seasonally adjusted GDP data revealed that economic growth in the euro area continued to pick up with GDP increasing by 0.1% q/q. However, we still await the final GDP prints as the preliminary flash is slightly distorted by volatile Irish GDP numbers. The upward trend is further confirmed by April PMIs with overall business activity growth at an 11-month high.

Europe, And the World, Should Use Green Subsidies Cooperatively (IMF) - Governments across the world are using subsidies to support the green transition. Green subsidies can be helpful where there are market failures. When carbon emissions are underpriced in relation to their true cost to society or preferable policy solutions (such as carbon pricing) are not in place, subsidies can steer businesses and consumers towards clean technologies that are less polluting while also lowering the costs of those technologies.

Turkey’s annual current account deficit dropped in March (ING) - With a better-than-expected monthly reading, Turkey's current account deficit narrowed for the first time in March, on an annual basis, since early 2022.

Spain | Analysis of national tourist flows in real time between January and April of 2023 (BBVA) - During the first four months of the year, total tourist spending (domestic and foreign) was 39pp above that observed during the same period of 2019 (5pp more than in the previous four-month period), according to spending data with BBVA credit card.

Australia

Australian housing market update: May 2023 (NAB) - It’s looking increasingly likely that Australian housing values have bottomed out, with CoreLogic’s national Home Value Index having posted a second consecutive monthly rise. April’s half a percent increase, follows a 0.6% lift in March, leaving the Home Value Index 1.0% higher over the past three months.

Taiwan

Taiwan economy slumps into recession (S&P Global) - Taiwan's export-driven economy has been hit by slumping exports, resulting in GDP contracting by 3.0% year-on-year (y/y) in the first quarter of 2023, following negative growth in the fourth quarter of 2022. With two consecutive quarters of negative growth recorded, Taiwan's economy has entered a technical recession.

Inflation

US CPI Primer: Understanding inflation and its impact on portfolios (Saxo Bank) - Inflation is a key metric watched by traders and investors for its impact on portfolios. The impact can be direct with high inflation eating up investment returns, or indirect as the resulting change in central bank policies creates varied impacts across asset classes. We dig deeper on the different measures of inflation, key metrics to watch, and how to trade the release.

The Impacts of Supply Chain Disruptions on Inflation (Cleveland Fed) - Since early 2021, inflation has consistently exceeded the Federal Reserve’s target of 2 percent. Using a combination of data, economic theory, and narrative information around historical events, we empirically assess what has caused persistently elevated inflation. Our estimates suggest that both aggregate demand and supply factors, including supply chain disruptions, have contributed significantly to high inflation.

Industrial imports prices on downward trend (Eurostat) - After a dramatic increase in industrial import prices starting in the second half of 2020 and peaking in the Summer of 2022, import prices have been on a steep downward trend for the last seven months. Still, they are much higher than in previous years, remaining at the highest levels ever recorded.

Markets

Hedge Funds: Improved Prospects in the Post-Modern Cycle? (Goldman Sachs) - We suspect we have now entered a ‘Post-Modern Cycle’ shaped by increased geopolitical risk, a partial pullback from globalization, and higher energy and labor costs. This environment has the potential to result in stickier inflation, a higher-for-longer rate environment, and elevated volatility for risk assets overall. This different set of macro conditions and priorities may imply different opportunities and risks for investors to consider, and the above-average equity and bond returns they have become accustomed to may potentially be challenged.

Commodities Caught in Fog of Uncertainty (BMO) - Commodity markets remain focused on the risk of a major U.S.-led downturn developing via a further escalation of bank stress or the (remote, but rising) possibility of a U.S. debt default. Even signs that China’s economy is recovering, albeit somewhat unevenly, are being ignored.

Investment Traffic Lights (May 2022): Our monthly market analysis and positioning (DWS Group) - After a turbulent March, April offered some time to digest what had happened. Investors used the time to rebuild some confidence but, at the beginning of May, their nervousness returned. Inflation, recession and the banking system are the three big worries, and not only for central bankers. “Muddling through” remains our base case.

Real Estate

Mortgage Activity Increases Despite Affordability Issues (NAHB) - Per the Mortgage Bankers Association’s (MBA) survey through the week ending May 5th, total mortgage activity increased 6.3% from the previous week and the average 30-year fixed-rate mortgage (FRM) rate fell two basis points to 6.48%. The FRM rate has risen 18 basis points over the past month.

Outlook

Navigating geopolitical headwinds (S&P Global) - Geopolitics is no longer reserved for dinner-party conversation. We find ourselves simultaneously in a pandemic recovery, an ongoing conflict in Ukraine, and a reorientation of global partnerships amidst strategic competition. A period out of equilibrium as the world rebalances. The contours of global risk today and in the years ahead are unlikely to be narrowly delineated by an arms race, space race or nuclear threat forcing countries to choose sides, as countries are instead pursuing pragmatism: collaborating across spheres of mutual interest while simultaneously competing elsewhere across spheres of national interest.

Eurozone, Japan inflation and US, China data in focus (S&P Global) - The week ahead sees a packed economic calendar with key releases due from the US to mainland China, notably for both including industrial production and retail sales figures. The eurozone also updates Q1 GDP alongside inflation and industrial production figures, while the labour market report is out from the UK. Central bankers in both the US and Europe will be watched for comments particularly with regards to the economic and monetary policy outlook.

Asia week ahead: Policy meetings in China and the Philippines (ING) - Next week’s data calendar features policy meetings from the People's Bank of China (PBoC) and Banko Sentral ng Pilipinas (BSP), wage and job data from Australia, plus growth and price data from Japan.

Green

Stronger supply of sustainable aviation fuels crucial to securing uptake (ING) - Blending sustainable aviation fuels (SAFs) needs to grow massively to meet ambitions for 2030 and beyond. Demand is there, but supply is limiting uptake. Ramping up capacity investments is critical to meet the aspired goals. Airlines (purchase grants) and suppliers (production, delivery) have a joint role here, but more policy support will help.

Climate targets expedite the take-off of sustainable aviation fuels (ING) - It’s a pivotal time for sustainable aviation fuels (SAFs). Demand depends heavily on regulation and airline commitments, and blending is just starting off. But on the back of progressive target-setting for 2030, demand is about to accelerate. And this is necessary to curb and reduce net emissions, with airline traffic rebounding post-Covid.

Time is running out for bank climate-related risks disclosures (ABN AMRO) - The ECB has released its third review on banks’ climate-related and environmental (C&E) risk disclosures practices and trends. Supervisors recognise developments and improvements, but confirm that financial institutions are still lagging behind their expectations . The report also revealed that most banks are not yet prepared to comply with EBA ITS Pillar 3 reporting guidelines. Banks need to further substantiate their disclosures and reports and start providing less generic information.

Subscribe to receive Econ Mornings every weekday at 9 am. More economic and finance content on Twitter, Reddit, and my website.