Deflation is Now a Concern for China While Inflation Remains a Concern for US Small Business

Economic news and commentary for April 11, 2023

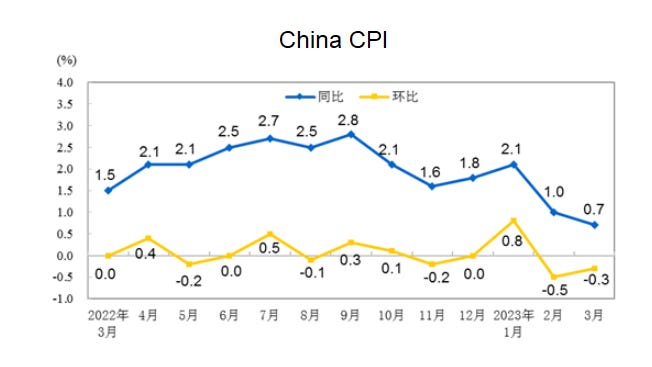

China CPI & PPI

Though China’s reopening may be improving economic activity, that improvement is not being reflected in price developments. In March, China's CPI fell -0.3% MoM but was still up 0.7% YoY. This annual pace is a slight deceleration from the 1.0% YoY in February and the second consecutive deceleration from a near-term peak of 2.1% YoY set in January when there was hope that the lifting of restrictions would breathe some life into businesses and their pricing power. At the moment, that doesn’t seem to have happened. Food prices were one of the main sources of inflation at the start of the year, growing as much as 4% YoY at some point, but in March they fell a sharp -1.4% MoM to drop the annual inflation rate to 2.4% YoY. Gas prices which were also a source of inflation but back further in 2022 are now down -6.4% YoY after another dismal month. Core CPI measuring the core segments was flat on the month and only up 0.7% YoY as goods prices tumbled -0.5% MoM only to be offset by a 0.1% MoM increase in services.

March’s inflation trends are interesting since there has been an improvement in retail sales to start 2023 which had been an encouraging sign that Chinese growth could get back on track. However, this seems to be more of a limping back to normalcy than a surge past the pre-pandemic levels of economic activity for consumers. This has all occurred despite an enthusiastic Two Sessions conference and the backing of easy monetary policy. Before condemning the Chinese economy again, it is worth noting that a large part of the disappointment in today’s report can be traced back to the sharp drop in food prices, and there were some signs of life in categories like clothing (0.5% MoM), household appliances (0.4% MoM), and other supplies/services (0.8% MoM), but these categories were basically the only ones keeping core inflation from falling on the month. One possible explanation is that poor growth in Japan, Europe, and, to a lesser extent, the US is causing firms who typically enjoy growth from strong exports to see less demand for the supply that they ramped up in the post-restriction period. If that is the case, domestic retail sales would stay more stable while industrial production falls to adjust for the imbalance in the Chinese goods markets. Regardless, it’s clear we’re not going to get the lift from the Chinese economy that we thought we would.

This explanation does get some credence from the fact that producer price trends in China have been worse than consumer price trends. In March, PPI was unchanged and down -2.5% YoY which is a further deterioration from the -1.4% YoY in February. However, the PPI report contrasted with the CPI report in that it didn’t get pushed down as much by food prices which were down only -0.1% MoM for producers. Alternatively, both manufacturing and raw materials firms had dismal pricing trends, with their PPIs down 0.0% MoM and -0.2% MoM respectively. The annual pace of pricing for both categories of firms has prices lower by -3% YoY. The results for March could have been worse if it weren’t for an improvement in metals pricing for Chinese firms which has been depressed for about a year now. Non-ferrous and ferrous metal materials were up 0.7% MoM and 1.1% MoM respectively but both are still down -3% YoY or worse. Outside of these gains, there wasn’t much else to talk about as most other categories were negative or basically unchanged.

While the Chinese service sector has strengthened in the last few years, it still has one of the strongest export complexes in the world and relies on that sector for growth. When there is weakness there, firms tend to have weaker pricing power and will respond by lowering supply. Because of this, we should expect to see weak production data for March and a disappointing Q1 GDP number (though it will still be strong because of base effects). Additionally, it would not be a surprise for the PBoC to react with more stimulus activity as leadership in Beijing has suggested that actions like rate cuts and reserve requirement reductions are clearly on the table to revive the economy.

US NFIB Small Business Optimism Index

The NFIB Small Business Optimism Index edged down -0.8 pts to 90.1 in March which means that it has been below the long-term average of 98 for fifteen consecutive months. The most jarring sub-index continues to be the measure tracking owners’ expectations of the economy to improve which has remained below -30% since September 2021 (-47% in March). That index is closely linked to sub-indexes tracking weak plans to increase inventory (-4%), sales expectations (-15%), and the earnings trends (-18%) which are all solidly negative.

But let’s get to the indexes that everyone is actually looking at. The Actual Price Changes and the Price Plans indexes both were mostly unchanged in March with the former falling -1 pt to -37, and the latter increasing 1 pt to 26. The flatness here suggests there was little to no change in the inflation situation for small businesses. Despite that, a smaller percentage of firms noted that inflation was the number one challenge for them, 24% in March, down -4 ppts from February. Other closely watched indexes describe the labor situation for small businesses which are sensitive to acute labor market imbalances. The Actual Employment Changes index, at just 2, pointed to flat hiring in the last three months despite the Job Openings index persisting at a high 43 (though down -4 pts from February). These openings continue to be hard to fill as the qualified labor supply remains slim. A net 53% of small businesses reported that there were few or no qualified applications for jobs. Even with labor shortages, there are some signs that labor demand is being shifted back, probably in response to weaker business activity developing. The Hiring Plans index dropped -2 ppts to 15 in March which is the lowest reading since May 2020.

Still to come…

7:30 pm (EST) - Japan Machinery Orders

7:30 pm - Japan PPI

Morning Reading List

The Westpac-Melbourne Institute Consumer Sentiment Index jumped 9.4% MoM to 85.8 in April, but it is still down -10.4% YoY. Economic expectations over the next year improved a sharp 16.5% MoM. The report notes that, "the decision by RBA Board to pause is the key to this resurgence."

The NAB Business Survey Business Conditions index fell -1 pts to 16 in March.

Business confidence improved 3 pts to -1 as forward orders also improved slightly, up 1 pt to 4. Labor costs fell sharply from 2.6% QoQ in February to 1.9% QoQ in March.

Euro area retail sales fell -0.8% MoM and -3.0% YoY in February. Food and non-food sales were both down a moderate amount, -0.6% MoM and -0.7% MoM respectively. Fuel sales fell the most on the month, down -1.8% MoM, but were still up 1.1% YoY.

The German truck toll mileage index decreased by a calendar and seasonally adjusted -2.6% MoM and -3.8% YoY in March.

China CPI & PPI

China: disappointing inflation data point to weakness in the economy (ING) - China's March CPI data were worse than expected and weaker compared to February. This is not the right sign for a full economic recovery. We expect next week's GDP report to show a partial recovery. The government needs to add more stimulus to the economy.

Euro Area Retail Sales

Eurozone retail sales down again in February despite upbeat surveys (ING) - The downward trend in retail sales volumes continued in February, making a positive contribution to first quarter GDP unlikely. While there may be strength in places other than retail, these figures do not provide any particular reason to expect a strong rebound in growth.

US

US Weekly Economic Commentary: Big wheel keeps on turning — but it’s slowing (S&P Global) - Data out last week — admittedly looking in the rearview mirror — showed the economy exhibiting decent forward momentum, but there are signs that momentum is slowing. In this month's forecast update, issued April 6, we revised up our forecast for first-quarter GDP growth to +1.9% (annualized), from last month's -0.4%. However, concerns over the potential tightening of financial conditions from a pull-back in bank lending led us to mark down growth over the remainder of the year, on average, by 0.3 percentage point.

Residential Building Wage Growth Slowing (NAHB) - Average hourly earnings for residential building workers* continue to rise in February 2023 but at a slower pace. Wage growth has retreated below or close to 3%, from the highest rate of 2021. Labor market data indicate that business hiring is softening as the economy shows signs of weakening.

How to Lose Reserve Currency Status (First Trust Portfolios) - History is full of economic and societal collapses. The Incan and Roman societies disappeared, the Ottoman Empire fell apart, the United Kingdom saw the pound lose its reserve

currency status. So, anyone who says the US, and the dollar, couldn’t face the same fate doesn’t pay attention to history.

Small Business Lending and the Paycheck Protection Program (San Francisco Fed) - The Paycheck Protection Program (PPP) and the PPP Liquidity Facility were launched early in the pandemic to help many small businesses survive. These programs encouraged banks to lend more extensively to small businesses over the first half of 2020. Since then, however, banks have reduced their exposure to these loans, leaving no significant changes in small business lending associated with participation in these programs over the three-year period from 2020 through 2022.

Employment March 2023: Moderation (EY Parthenon) - We anticipate tightening credit conditions will represent a drag on the US economy worth around 0.5% of GDP over the next 18 months. As a result, we now anticipate real GDP growth will be closer to 0.8% in 2023 and around 1.5% in 2024. We see the economy losing around 600,000 jobs in the coming quarters with the unemployment rate rising toward 4.6% by year-end.

Nonfarm Payrolls Increased 236,000 in March (First Trust Portfolios) - Even as the number of people working went up, the total number of hours worked slipped 0.1%. In other words, businesses were hiring but there was less for their workers to do. In turn, this is consistent with our view that the labor market will be a lagging indicator as we enter the next recession; businesses will keep hiring because they think they need to hoard workers to fulfill future increases in business activity. But if those increases don’t come, that just means more workers who get laid off later on.

Bank Term Funding Program Provides Liquidity to Depository Institutions (St Louis Fed) - On March 12, the Federal Reserve launched the Bank Term Funding Program (BTFP), a lending program for eligible depository institutions—banks, savings banks and credit unions—experiencing liquidity issues. The goals of the BTFP are to bolster institutions’ capacity to safeguard deposits and ensure the ongoing provision of credit to communities and the broader economy.

Europe

Spain | From tourism to passenger cars: the new geography of regional growth (BBVA) - Consumption picks up again in the first quarter of 2023, which continues to boost the most touristic regions. Furthermore, the more industrially oriented territories are benefiting from the gradual disappearance of bottlenecks and lower energy costs.

Weak Growth, High Inflation, and a Cost-of-Living Crisis (World Bank) - The Russian Federation’s invasion of Ukraine has had devastating economic and social consequences for Ukraine and profound negative impacts on developments in Europe and Central Asia (ECA). The expansion of economic activity in ECA slowed markedly to 1.2 percent in 2022, as disruptions to the supply of key commodities, surging inflation, and the tightening of monetary policy weighed on activity in the region.

Asia

Bank of Korea stands pat again amid slowing inflation (ING) - As widely expected, the Bank of Korea (BoK) left its policy rate unchanged at 3.5% for the second consecutive meeting. The BoK has pushed back against expectations of a rate cut later this year, but we continue to argue that the central bank has ended its rate-hike cycle and will eventually shift to easing by the end of the year.

Inflation

Weekly Pricing Pulse: Commodities higher as contagion fears wane (S&P Global) - The Material Price Index (MPI) by S&P Global Market Intelligence increased 0.7% last week, a return to growth after two consecutive weekly declines. The increase was widespread with seven of the ten subcomponents rising. The MPI still sits 30% below its year ago level which was near the all-time peak.

Rates

Interest Rates Likely to Return Toward Pre-Pandemic Levels When Inflation is Tamed (IMF) - How close will depend on the persistence of public debt, on how climate policies are financed and on the extent of deglobalization.

How Do Interest Rates (and Depositors) Impact Measures of Bank Value? (Liberty Street Economics, NY Fed) - The rapid rise in interest rates across the yield curve has increased the broader public’s interest in the exposure embedded in bank balance sheets and in depositor behavior more generally. In this post, we consider a simple illustration of the potential impact of higher interest rates on measures of bank franchise value.

Financial Markets

The 2022 Spike in Corporate Security Settlement Fails (Liberty Street Economics, NY Fed) - Settlement fails in corporate securities increased sharply in 2022, reaching levels not seen since the 2007-09 financial crisis. As a fraction of trading volume, fails that involve primary dealers reached an all-time high in the week of March 23, 2022. In this post, we investigate the 2022 spike in settlement fails for corporate securities and discuss potential drivers for this increase, including trading volume, corporate issuance, fails in bond ETFs, and operational problems.

Debt

How to Tackle Soaring Public Debt (IMF) - Timely and appropriate fiscal policy adjustments can reduce debt, but countries in distress will need a more comprehensive approach.

What’s New with Corporate Leverage? (Liberty Street Economics, NY Fed) - The Federal Open Market Committee (FOMC) started increasing rates on March 16, 2022, and after the January 31–February 1, 2023, FOMC meeting, the lower bound of the target range of the federal funds rate had reached 4.50 percent, a level last registered in November 2007. Such a rapid rates increase could pass through to higher funding costs for U.S. corporations. In this post, we examine how corporate leverage and bond market debt have evolved over the course of the current tightening cycle and compare the current experience to that during the previous three tightening cycles.

No rest for the leveraged (Allianz) - The rebound in business insolvencies is picking up speed: Our Global Insolvency Index is set to jump by +21% in 2023 and +4% in 2024.

Research

Intergenerational Altruism and Transfers of Time and Money: A Life Cycle Perspective (Minneapolis Fed) - Parental investments significantly impact children’s outcomes. Exploiting panel data covering individuals from birth to retirement, we estimate child skill production functions and embed them into an estimated dynastic model in which altruistic mothers and fathers make investments in their children. We find that time investments, educational investments, and assortative matching have a greater impact on generating inequality and intergenerational persistence than cash transfers.

Helicopter Drops and Liquidity Traps (Minneapolis Fed) - We show that if the central bank operates without commitment and faces constraints on its balance sheet, helicopter drops can be a useful stabilization tool during a liquidity trap. With commitment, even with balance sheet constraints, helicopter drops are, at best, irrelevant.

Subscribe to receive Econ Mornings every weekday at 9 am. More economic and finance content on Twitter, Reddit, and my website.