Early July Economic Data Leads to a Sharp Increase in Q3 Growth Expectations

Economic news and commentary for August 17, 2023

After a strong GDP report for Q2 there were a lot of expectations for some of the momentum in the US economy to fade. Despite Fed rate hikes, the economy has expanded at an annual rate of at least 2% over the last four quarters after the technical recession at the beginning of 2022. Personal consumption has also been strong since the end of the pandemic, growing by at least 1% in every quarter since the beginning of the pandemic. Surely these numbers couldn’t be maintained after more than 500 basis points of hiking? Early July economic data suggests that it is possible.

To start the week, retail sales topped expectations by a substantial margin coming in at 0.7% MoM compared to an 0.4% MoM consensus estimate. When excluding auto sales, the beat was even stronger at 1.0% MoM vs the same 0.4% MoM consensus estimate. Despite some weakness in sales of electronics and furniture (both down -1% MoM or more), non-durable and services spending more than made up the difference. Food & drinking services spending remains the leader on the consumption end, up 1.4% MoM and 11.9% YoY in July, which is representative of consumers maintaining strong demand for services throughout the year so far. That seems like it could be a trend that follows into Q3. Non-durable categories like food & beverage (0.8% MoM) and clothing (1.0% MoM) were right there with strong food services. Finally, we also strength in the nonstore retail sales category (1.9% MoM) which benefitted from Amazon’s Prime Day during the month.

A day later, the Federal Reserve released an update on industrial production which has been a notable segment of struggle for the economy so far in 2023. This is one sector that has actually seen weakness as a result of tighter financial conditions. Both the ISM and S&P Manufacturing PMIs have pointed to an industrial contraction in the last few months, and weak industrial production has followed. However, July results pointed to a slight turn around in the fragility. The headline index increased 1.0% MoM, the strongest increase since the first month of the year, which surged past the consensus forecast of a meager 0.3% MoM increase. The gain was boosted by final product manufacturing, specifically consumer goods up 1.4% MoM and business equipment up 1.0% MoM. Now this report is slightly less rosy than the retail sales data, both headline and manufacturing industrial production are down on a YoY basis (-0.2% MoM and -0.7% MoM), but the bright start to Q3 gives hope that a turn around is possible. This is especially true when considering that producer prices of goods have been negative for a few months now which is likely a huge relief for manufacturing firms.

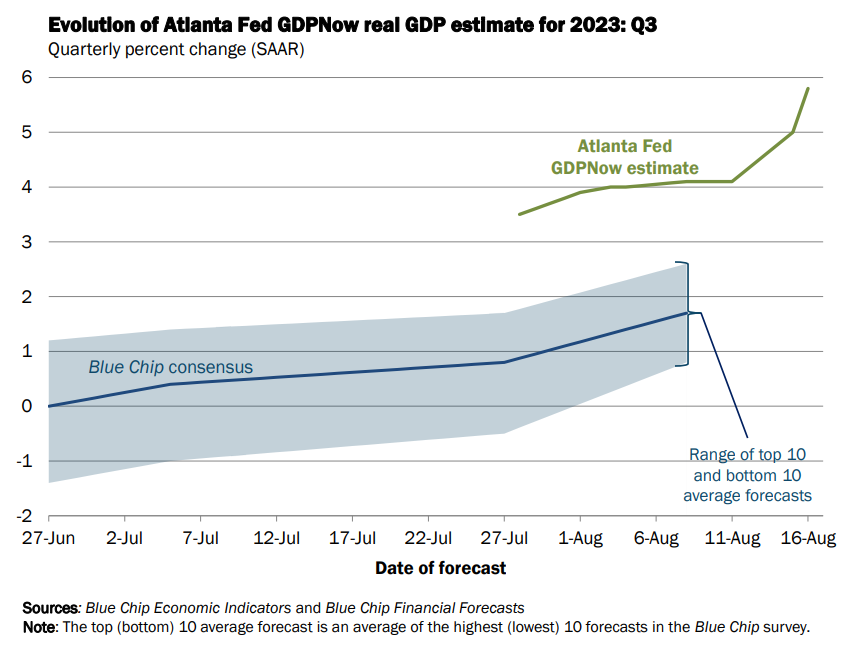

The early resilient economic data for July has many forecasters questioning the call for a slowdown in the second half of 2023 and a potential recession at the turn of the new year and the start of 2023. The most famous nowcasting model, the Atlanta Fed GDPNow estimate, has Q3 2023 GDP growth projected at a hot 5.8%, more than double the rate of growth in the first two quarters. The duo of July reports mentioned above caused the model to adjust this forecast up 1.7 ppts from 4.1% at the start of the week with estimates of consumption growth and equipment investment rising with it. While this model is often discounted for its volatility, top forecasters elsewhere are increasing Q3 GDP estimates from near nothing at the beginning of the quarter to close to 2% in August. The general sentiment is unquestionable: the US economy is not fading away, and the resilience will continue into Q3.

Still to come…

10:00 am (EST) - E-Commerce Retail Sales

10:00 am - US Leading Indicators

10:30 am - US EIA Natural Gas Report

4:30 pm - US Fed Balance Sheet

7:30 pm - Japan PPI

Morning Reading List

Other Data Releases Today

Some early signs of weakness in Australia's labor market. Australia's employment fell -14,600 & total unemployment increased 35,600. The unemployment rate ticked up 0.2 ppts to 3.7%, and the participation rate edged -0.1 ppt lower to 66.7%.

The euro area trade balance improved from -€0.3 bil to €223.0 bil in June. Exports increased 4.3% MoM, and imports fell -5.3% MoM. Energy imports in the first 6 months of 2023 are down -25.1% from the same period last year.

Japan's services activity index fell -0.4% MoM in June but is still up 1.8% YoY. The Personal Services index grew 0.6% MoM, and the Business Services index grew 1.0% MoM. Recreation-related services crashed -5.2% MoM (but up 7.1% YoY).

EU bankruptcies grew for the 6th quarter in a row, up 8.4% QoQ in Q2 2023 to the highest level since the series started in 2015. The largest gains vs Q4 2019 were in accommodation & services (82.5%) and transport & services (56.7%).

Jobless claims fell -11,000 to 239,000 last week. The insured unemployment rate was 1.2%, up 0.1 ppts. Continued claims fell -32k to 1.72 million.

The Philadelphia Fed Manufacturing Survey Business Activity index jumped 25.5 pts to 12.0 in August. New orders and shipments both flipped to expansion, up 31.9 pts to 16.0 and up 18.2 pts to 5.7. Prices paid increased 11.3 pts to 20.8.

US Housing Starts

Housing starts and permits rebound in July (TD Bank) - Housing starts rose 3.9% month-on-month (m/m) in July to 1.45 million (annualized) units, right in line with consensus expectation. Revisions to the two prior months subtracted a net 12k units from the previous reported tallies.

U.S. Housing Starts and Industrial Production Bounce Back (BMO) - U.S. housing starts exceeded expectations and rose 3.9% to a two-month high of 1.45 mln (annualized) in July. However, that comes after the prior month was revised down to show an 11.7% drop (prev. -8.0%). Excluding the South, starts jumped 10.7%, as every other region saw an increase. The turnaround in the headline number was powered by single-family units, which rose 6.7%, halting two straight months of declines, while volatile multis dropped 2.9%.

US housing market in gridlock, with risks emerging (ING) - High mortgage rates are crushing demand while owners that want to sell and move are trapped on cheap mortgages, which limits supply. The result is that prices are rising again in many areas. It may be that eventual Federal Reserve rate cuts unleash pent-up supply and that could potentially be the trigger for renewed price falls next year.

Single-Family Starts Edge Higher in July but Rising Rate Concerns Persist (NAHB) - A lack of existing inventory and solid demand for housing helped offset rising mortgage rates and push single-family production higher in July, even as builders continue to grapple with elevated construction and financing costs as well as a lack of skilled labor.

Housing Starts Increased 3.9% in July (First Trust Portfolios) - Industrial production surprised to the upside in July, easily beating consensus expectations to post the largest monthly gain since January. Looking at the details, the strength in today’s report was broad-based with every major category posting a gain. The manufacturing sector was the biggest positive contributor in July, with activity rising 0.5%, the first gain in three months.

Housing Starts Climb in July: Divergence Between Single-Family and Multifamily Construction On Display (Wells Fargo) - Residential construction continues to gradually gain steam. Total housing starts rose 3.9% to a 1.45 million-unit pace during July. The diverging trend between single-family and multifamily activity was once again evident, with single-family starts improving and multifamily starts declining during the month. Building permits took a similar trajectory, although the total increase in permits was fairly modest.

US Industrial Production

Revisions Take Some Flare Out of Upward Surprise in IP (Wells Fargo) - Industrial production jumped 1.0% in July, but downward revisions to June and concentrated strength in utilities and auto manufacturing take some of the flare out of the headline growth rate. Manufacturing production has more-or-less moved sideways this year amid a stalling in goods demand.

Industrial Production Jumped 1.0% in July (First Trust Portfolios) - Industrial production surprised to the upside in July, easily beating consensus expectations to post the largest monthly gain since January. Looking at the details, the strength in today’s report was broad-based with every major category posting a gain. The manufacturing sector was the biggest positive contributor in July, with activity rising 0.5%, the first gain in three months.

US FOMC Minutes

Fed minutes signal members are open to additional rate hikes (TD Bank) - Today's minutes confirmed that the Fed has kept the door open to additional rate hikes despite decelerating price pressures and signs that labor market conditions are beginning to come into better balance. This progress has seen the "soft landing" narrative become more popular, and has been reflected in financial markets, which expect the Fed to begin easing policy in the first half of 2024.

Fed minutes indicate a bias to hike, but we don’t think it will carry through (ING) - The Federal Reserve cites inflation concerns as a reason to keep further rate hikes on the table, but splits are starting to form. We expect a September pause that will end up lasting well into the first quarter of 2024 when rate cuts will come onto the agenda.

FOMC Minutes (July 25-26, 2023) – Policymakers still ‘significantly’ hawkish (EY Parthenon) - The Federal Open Market Committee (FOMC) minutes revealed that almost all participants favored raising the federal funds rate by 25 basis points (bps) to 5.25%-5.50% at the July policy meeting with only a couple of participants indicating that they favored leaving the target range unchanged. Most participants continued to see “significant” upside risks to inflation, which could require further tightening of monetary policy.

FOMC Minutes (July 25-26) — Rate Hike Door Still Open (BMO) - The Minutes from the FOMC’s confab on July 25-26 showed that the Fed is still open to raising policy rates again if the economic data indicate that further tightening is warranted. Although a “couple” of non-voters were in the pause camp for July as well, “almost all participants judged it appropriate to raise the target range for the federal funds rate to 5-1/4 to 5-1/2 percent at this meeting.”

US

One year on: America’s Inflation Reduction Act is closer to reshaping the US clean energy industry (ING) - The Inflation Reduction Act (IRA) has spurred massive investment announcements in clean energy, with greater tax credit implementation clarity sustaining investor and developer appetite. The US energy industry is set to change profoundly, and the IRA is responsible for much of this – but it is not a one-stop shop.

Decomposing an Economic Impact into Its Local and Spillover Effects (St Louis Fed) - U.S. states are highly interdependent, connected by interstate trade in goods and services, integrated capital markets and a common central bank, as just a few examples. Given this interconnectedness, it is natural to ask whether an economic event occurring in one state has not only a direct effect in that state but also an indirect effect on other states.

Europe

Tough Times Still Ahead For The U.K. Economy (Wells Fargo) - U.K. Q2 GDP was surprisingly resilient, showing moderate growth of 0.2% quarter-over-quarter, including gains in both consumer spending and business investment. Going forward, however, our view remains for slower U.K. growth and, eventually, a mild U.K. recession. Real household income dynamics and rising interest rates still appear likely to weigh on consumer activity, while softening sentiment surveys point to slower growth ahead.

Norges Bank hikes rates and signals a final move in September (ING) - Norway's central bank is poised for one final rate hike in September, and with other major central banks either at or close to the peak for policy rates, the impetus to raise rates further is fading. The domestic backdrop continues to improve for the krone.

Australia

NAB SME Business Insights: Supply Chain Update Q2 2023 (NAB) - Supply chain pressures on Australian SMEs continue to ease and are expected to continue easing over the next 12 months. Improving supply conditions were reported across most industries.

NAB SME Business Insights: Labour shortages Q2 2023 (NAB) - Labour shortages were a little more problematic for Australian SMEs in Q2. SMEs are also more worried about the impact labour shortages will have on their business in the next 12 months. Labour shortages were a “very significant” issue for 1 in 3 SMEs overall, but for around 4 in 10 in the Transport & Storage, Construction and Health sectors in the last 3 months.

Real Estate

Slight Decline for Single-Family Built-for-Rent (NAHB) - Single-family built-for-rent construction has cooled as investor interest has pulled back on tighter financial conditions. According to NAHB’s analysis of data from the Census Bureau’s Quarterly Starts and Completions by Purpose and Design, there were approximately 20,000 single-family built-for-rent (SFBFR) starts during the second quarter of 2023.

Energy

Tightness takes hold of the oil market (ING) - The last month has seen the oil market convincingly break out of the range it has been stuck in since early May. Tightening fundamentals and prospects for a softer-than-expected landing for the US economy have pushed the market higher. Constructive fundamentals should mean more strength in the months ahead.

FX

BRICS expansion and the dollar: Would a larger bloc mean faster de-dollarisation? (ING) - Despite talk of an enlarged BRICS alliance and the possibility of a new currency which could challenge the dominance of the dollar, we do not think the greenback is in any immediate danger of losing its status as the primary global currency. In this report, we explain why.

BRICS expansion and what it means for the US dollar (ING) - The BRICS grouping of major emerging economies is holding its fifteenth summit later this month. Up for discussion: an expansion of the bloc, greater use of local currencies and the possibility of a BRICS currency which may have the potential to challenge the dominance of the US dollar. We'll outline here the key points and link to our major new report.

Crypto

What Makes Cryptocurrencies Different? (Liberty Street Economics, NY Fed) - Permissionless blockchains, which support the most popular cryptocurrency networks like Bitcoin and Ethereum, have shown that it is possible to transfer value without relying on centralized trusted third parties, something that is new and remarkable (although perhaps most clearly useful for less developed financial markets). What makes permissionless blockchains able to transfer value without relying on a small number of trusted third parties is the combination of several components that all need to work together. The components themselves are not particularly new, but the combination of these components is more than the sum of its parts. In this post, we provide a high-level overview of these components and how they interact, taking Bitcoin as an example.

Looking for a way to take advantage of higher interest rates? I recommend SoFi’s high-yield savings account which has a yield of 4.5% (subject to change) and includes FDIC deposit insurance for both its checking and savings accounts just like a traditional bank. Use my referral link to get a sign-up bonus and start earning that rate today. (This is also a great way to support me since I get a bonus too!)

Subscribe to receive Econ Mornings every weekday at 9 am. More economic and finance content on Twitter, Reddit, and my website. You can also see my feed on the PiQSuite platform as a partnered feed.