ECB Hikes Again, China Announces Weak Economic Data

Economic news and commentary for June 15, 2023

ECB Announcement

The European Central Bank (ECB) has decided to raise its policy rates by 25 basis points, pushing the deposit rate up to 3.5%. Simultaneously, the ECB has announced a reduction of €15 billion in the Asset Purchase Program (APP) by the end of this month. Furthermore, starting from July 2023, the reinvestment of APP assets will be discontinued. These adjustments reflect the ECB's cautious approach towards monetary policy and its aim to gradually normalize its extraordinary measures implemented during the pandemic.

The decision to hike rates follows the ECB's upward revision of its forecast for core inflation. The central bank acknowledges that while indicators of underlying price pressures remain robust, there are tentative signs of softening in certain areas. Consequently, the ECB now projects core inflation to be at 5.1% in 2023, 3.0% in 2024, and 2.3% in 2025. The ECB has also revised its growth projections for the eurozone, downgrading them for this year and the next. It now anticipates the economy to grow by 0.9% in 2023, followed by a slightly improved outlook of 1.5% in 2024 and 1.6% in 2025. The downgrade this year likely reflects a more restrictive policy rate this year than previously expected.

The ECB emphasizes that its future actions will be dependent on incoming data, adopting a cautious and data-driven approach. The central bank will closely monitor inflation developments in the coming months, and unless there is a noticeable slowdown, market indicators suggest that more rate hikes may be on the horizon.

China Industrial Production, Retail Sales & Fixed Asset Investment

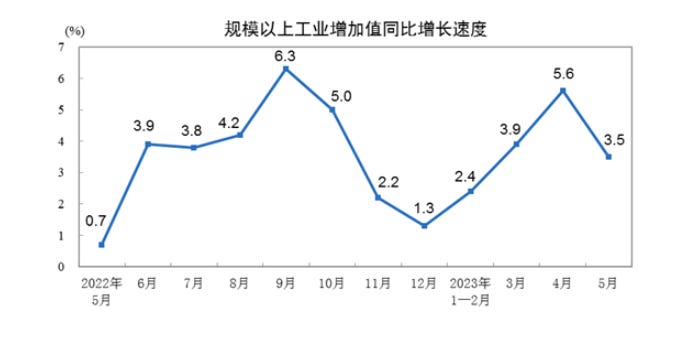

China's industrial production experienced a modest growth of 0.6% MoM and 3.5% YoY in May, marking a decline from the 5.6% YoY growth observed in April. The manufacturing sector saw a YoY increase of 4.1%, but of that, private production lagged with a mere 0.7% YoY growth. These figures highlight the persisting weaknesses in the goods side of China's economy, primarily due to sluggish demand for its exports.

However, despite these challenges, production growth remains focused on areas outlined as national priorities by President Xi Jinping's government. Notably, the automotive industry witnessed a robust YoY growth of 23.8%, while the electrical machinery sector experienced a significant upswing of 15.4% YoY. Furthermore, the production of solar cells and power generators witnessed substantial growth rates of 53.1% YoY and 45.4% YoY, respectively. Conversely, traditional sectors like crude steel and steel manufacturing saw a decline in production. Crude steel production experienced a significant YoY decrease of -7.3%, while steel production declined by -1.3% YoY. These figures indicate a shift in focus from traditional industries towards sectors aligned with the government's strategic objectives of modernizing the production sector of China’s economy.

On the consumer side of China's economy, there are signs of potential momentum loss. Retail sales in May grew by a modest 0.42% MoM and 12.7% YoY, a decline from the 18.4% YoY growth seen in April. The breakdown of sales reveals the strong impact of reopening effects, with food and beverage revenue increasing by 35.1% YoY and sports and entertainment goods sales rising by 14.3% YoY. However, building material sales experienced a significant decline of -14.6% YoY, which can be attributed to the persistent troubles in the real estate sector over the past two years. Despite these challenges, domestic consumption remains a key driver of China's economic growth in 2023. To achieve GDP targets, China cannot afford to witness a slowdown in consumer spending. Recognizing this, the Chinese government aims to maintain a strong focus on stimulating domestic consumption and ensuring its steady expansion.

The preemptive reduction in short-term policy rates earlier this week confirmed the presence of weak investment and liquidity in China in May. Fixed asset investment in China grew by 4.0% YoY in May, down from 4.7% YoY in April. This marks the third consecutive month of deceleration in the annual growth rate of investment. Private investment faced a YoY decline of -0.1%, but this was partially offset by public investment growth of 8.4% YoY. Notably, investment in the electrical machinery manufacturing sector experienced a sharp YoY increase of 38.9%. It is no surprise that the national priorities set forth by President Xi Jinping are shaping the direction of investment in China. Most of the investment growth is derived from fiscal or monetary sources, aligning with the government's strategic vision for the country's economic development.

In conclusion, China's industrial production and retail sales faced challenges in May, indicating a slowdown in certain sectors and potential loss of momentum on the consumer side. However, the government's focus on national priorities, such as the automotive and electrical machinery industries, has propelled growth in those sectors. China continues to rely on domestic consumption as the primary driver of its economic growth in 2023, necessitating sustained efforts to stimulate consumer spending. Additionally, the government's strategic direction and monetary policies play a significant role in guiding investment decisions, emphasizing the importance of aligning

Still to come…

10:00 am (EST) - US Business Inventories

10:30 am - EIA Natural Gas Report

4:30 pm - US Fed Balance Sheet

10:30 pm - Bank of Japan Announcement

Morning Reading List

Other Data Releases Today

Japanese machinery orders 11.5% MoM in April spurred on by strong private order growth of 8.5% MoM. Manufacturing orders fell -3.0% MoM while non-manufacturing orders increased 11.0% MoM. Foreign orders rebounded from a weak March, up 12.3% MoM.

Japan's trade balance fell to -¥1.37 tril in May, down from -¥0.43 tril in April. Exports fell -12.0% MoM, and imports only fell -0.6% MoM. Machinery exports declined sharply with gen machinery down -13.3% MoM and electrical machinery down -11.9% MoM.

Australia's employment increased 0.5% MoM in May, and the unemployment rate fell -0.1 ppts to 3.6%. However, the underemployment rate increased 0.2 ppts to 6.4%, and monthly hours worked fell -1.8% MoM to 1.98 mil.

French CPI inflation for May was confirmed at -0.1% MoM and 5.1% YoY. Only food inflation had a slight upgrade from 14.1% YoY previously to 14.3% YoY in the final results. Core CPI increased 0.1% MoM and 5.8% YoY.

The euro area trade balance fell from €25.6 bil in March to -€11.7 bil in April. Exports fell 19.8% MoM, and imports fell -6.5% MoM. Export growth flipped from up 7.5% YoY to -3.6% YoY, and intra-euro area trade is now negative at -5.2% YoY.

Retail sales increased 0.3% MoM and 1.6% YoY in April. Core sales (ex-auto & gas) were up 0.4% MoM and 3.9% YoY. Building material sales jumped 2.2% MoM, and auto & parts sales grew 1.4% MoM. Gas sales are down -16.1% YoY as a result of lower gas prices. Sales in most other categories were sluggish, up under 0.5% MoM.

Jobless claims were unchanged at 262,000 last week. The insured unemployment rate was 1.2%. Continued claims increased 20,000 to 1.78 million.

Import prices fell -0.6% MoM and -5.9% YoY in May, export prices fell -1.9% MoM and -10.1% YoY.

Fuel Imports: -35.2% YoY (-2.3% MoM)

Nonfuel Imports: -1.6% YoY (-0.1% MoM)

Ag Exports: -8.1% YoY (-2.1% MoM)

Non-Ag Exports: -10.5% YoY (-1.8% MoM)

The Philadelphia Fed Manufacturing Survey Business Conditions index fell -3.3 pts to -13.7 in June. New orders fell -2.1 pts to -11.0 while production flipped 15.6 pts to 9.9. The Number of Employees index increased 8.4 pts to -0.4. The Prices Paid index remained mostly unchanged at 10.5.

The Empire State Manufacturing Survey Business Conditions index reversed 38.4 pts to 6.6 in June. New orders and shipments both jumped 30+ pts to 3.1 and 22.0.

The Prices Paid and Prices Received index both declined 10+ pts to 22.0 and 9.0.

The employment index was in a slight contraction at -3.6.

Fed Announcement

FOMC hits pause, but points to a restart later this year (TD Bank) - The Federal Reserve is taking a breather after 5 percentage points in interest rate hikes since March 2022. Based on the Fed's own projections, members are of the view that this is a temporary reprieve rather than a hard stop. And understandably so. The labor market has continued to exude strength and underlying measures of inflation are showing far more stickiness than previously thought.

A Hawkish Pause: Landing Flare for the Fed? (NAHB) - The Federal Reserve’s monetary policy committee maintained the federal funds rate at a top target rate of 5.25% at the conclusion of its June meeting. The Fed will also continue to reduce its balance sheet holdings of Treasuries and mortgage-backed securities.

Hawkish hold from the Fed offers maximum flexibility (ING) - The Federal Reserve leaves US interest rates unchanged but signals more hikes are on the cards with some hawkish projections for the economy. July is a 'live' meeting, according to Powell, but a one-meeting pause makes little sense given the long lags involved with monetary policy. With the disinflationary trend set to accelerate, we see an extended pause.

Fed lays the groundwork for further tightening (CIBC) - The FOMC opted to exercise patience and skipped an interest rate increase at today’s announcement, but laid the groundwork for 50bps of hikes ahead. That's in line with our view that we will see a 25bp rate increase at each of the next two meetings to reach a terminal rate of 5.75% on the ceiling of the fed funds range.

FOMC Policy Announcement and SEP — Hawkish Hiatus (BMO) - The FOMC paused policy today, after 10 consecutive rate hikes over 15 months for a total of 500 bps. This was mostly expected; the OIS market had it priced around 85% odds. However, the hiatus should be considered a ‘hawkish pause’, with the Fed retaining a tightening bias.

The Fed Is All Mixed Up (First Trust Portfolios) - If the Federal Reserve were paying close attention to the money supply it would know that monetary policy is now tight. Through April, the narrow M1 measure of money has fallen for thirteen straight months. The broader M2 measure of money has dropped nine months in a row and is down 4.6% from a year ago. M3, a broader measure of money that includes large CDs, is down 4.1% from the peak last July. Meanwhile, bank credit at commercial banks as well as their commercial and industrial loans are both down. If this isn’t tight, we’re not sure what tight means.

Rising Macro Risks May Limit Fed From Reaching Its Projected Peak (PIMCO) - The Federal Reserve paused in June but raised its estimates for the policy rate later this year. We expect a July increase but remain skeptical about subsequent hikes.

Research US - Fed review: Powell's hawkish bluff (Danske Bank) - The Fed held rates unchanged at 5.00-5.25% as widely anticipated. However, the updated 'dots' surprised hawkishly, signalling two more 25bp rate hikes. Between the lines, Powell did hint that the Fed is seeing underlying inflation cooling. While the strong macro data calls for hawkish communication, we doubt the rate hikes will end up materializing, and make no changes to our Fed call.

FOMC Review: Higher but slower (Nordea) - The FOMC kept the Fed Funds Rate Target unchanged at 5-5.25% while also forecasting another 50bps of hikes will be needed in 2023 as inflation has proven more stubborn than expected.

Cognitive dissonance (EY Parthenon) - The Federal Open Market Committee (FOMC) statement along with the Federal Reserve’s new economic projections and Fed Chair Jerome Powell’s press conference were an illustration of the current “cognitive dissonance” at the Fed. While extreme data dependence has convinced policymakers of the need to raise the federal funds rate by an additional 50 basis points (bps), the FOMC unanimously decided to maintain the policy rate unchanged in June.

US | Fed skips rate rise but hints it is set to hike in July (BBVA) - The FOMC voted unanimously to keep the target range for the fed funds rate unchanged at 5.00-5.25% but a hawkish shift in the updated SEP signaled that, with a more resilient economy and more stubborn inflation, nearly all members think that the Fed needs to do more.

US

The Producer Price Index (PPI) Declined 0.3% in May (First Trust Portfolios) - Producer prices declined for the third time in four months, falling 0.3% in May. As you can see from the nearby chart, the year-ago comparison for producer prices, now up 1.1%, has been moderating since the 11.7% peak in March 2022. Keep in mind, though, that part of the moderation is due to outsized jumps in inflation immediately after the invasion of Ukraine last year, which are now rolling off year-ago calculations.

Europe

Swedish May inflation review: Stubborn core inflation (Nordea) - CPIF-inflation stood at 6.7% y/y in May, down from 7.6% in April. The outcome was higher than we and others had expected.

China

China: Further rate cuts and weak activity data (ING) - After the rate cuts yesterday, the 1Y medium-term lending facility (1Y MLF) was cut 10bp today. Weak activity data mean that this is probably not the end of the stimulus, though the more important measures are likely to be fiscal.

Australia

Australia: Why markets may be pricing in too much tightening (ING) - Australia’s economy is slowing, though not enough to quell inflation fears. Inflation itself is falling, though the pace of decline has been erratic and the labour market remains robust. Amidst all of this, the Reserve Bank of Australia has been hiking rates though is struggling to get its message across about the likely path from here.

AMW – Making sense of the RBA’s productivity focus (NAB) - In today’s Weekly, we delve into Australia’s productivity and labour cost data given the RBA’s recent focus on these metrics, and explain why timely signals on the inflation outlook may be better found elsewhere.

Canada

Households' wealth continued to climb in the first quarter of 2023 (TD Bank) - Canadian household wealth climbed higher for the second quarter in a row, rising by close to $520 billion (+3.4% quarter-on-quarter) in the first quarter of 2023 – building on a 0.9% to close out 2022.

Higher Rates Hitting Households (BMO) - Lower disposable income led to a deterioration in household debt ratios in Q1 despite a slowdown in mortgage demand following the Bank of Canada's aggressive rate hike campaign. Meantime, elevated interest rates are pushing debt service costs higher, which are poised to climb further in the coming quarters as the BoC raised policy rates again in June. That will likely act as a notable headwind on consumption and broader economic growth through the rest of this year and into 2024. Household debt remains a key vulnerability to the Canadian economy, and one that the Bank will watch closely as it determines how much more tightening is required this cycle.

Mexico

Mexico | Consumption fell in May amid the displacement of the Hot Sale week (BBVA) - The BBVA Research Big Data Consumption Indicator (BDCI) reported a fall of (-)4.0% in May, with real figures adjusted for seasonality, amid the displacement of the Hot Sale week to the month of June.

Inflation

Global Inflation Watch - Euro area inflation pressures remain sticky (Danske Bank) - Inflation drivers continue to paint a mixed picture, but inflation is likely to head lower through 2023 in the US and euro area. Price pressures from food, freight and energy have clearly eased. Underlying wage and inflation pressures have showed tentative signs of easing in the US. In euro area, broader price pressures also moderated in May, but tight labour markets and temporary factors related to German transport ticket suggest that inflation will remain sticky for now.

Energy

Crude oil rises on upbeat demand outlook and China stimulus focus (Saxo Bank) - Crude oil trades higher for a second session, supported by raised expectations that Beijing is considering a broad range of measures to rivive a sputtering economy. In addition, an in-line CPI print on Tuesday has raised expectations the FOMC may keep rates unchanged at today's meeting. OPEC and the IEA meanwhile maintains an upbeat estimate for global oil demand in 2023 but with half of the increase expected to occur during the next quarter, there will be some room for disappointment should demand fail to rise at that rate.

Real Estate

Mortgage Activity Increases as Affordability Improves (NAHB) - Per the Mortgage Bankers Association’s (MBA) survey through the week ending June 9th, total mortgage activity increased 7.2% from the previous week and the average 30-year fixed-rate mortgage (FRM) rate fell five basis points to 6.77%. The FRM rate has risen 20 basis points over the past month.

Fiscal Policy

Income Countries’ Resilience to Shocks (IMF) - The economic gains from $272 billion in pandemic support for 94 countries were strongest in the poorest and more vulnerable recipients of IMF concessional financing.

The Fiscal Responsibility Act: Reduced fiscal risks, modest fiscal restraint (S&P Global) - On June 3, President Biden signed into law the Fiscal Responsibility Act of 2023. The key provisions of the Act suspend the debt ceiling through 2024, establish statutory caps on discretionary spending for fiscal years 2024 and 2025, and set non-statutory caps for fiscal years 2026 - 2029 that limit growth of spending to 1`% annually.

Subscribe to receive Econ Mornings every weekday at 9 am. More economic and finance content on Twitter, Reddit, and my website.