Econ Mornings: April 16th, 2025

Macro releases and commentary released the morning of April 16th, 2025

(all times are in EST)

Japan's Manufacturing Sector Sees Modest Improvement Amid Persistent Concerns Over Trade Tensions

Released: April 15, 2025 18:00 - Link

This morning's macro data brought some mixed signals from Japan's manufacturing sector, with the Reuters Tankan index improving 10 points to 9 in April, driven by a modest boost in the non-manufacturing index to 30. However, the outlook for firms remains bearish, particularly among export-heavy businesses such as automotive and machinery makers, who expressed concerns about rising labour costs and falling volumes due to intensifying Sino-U.S. trade tensions. Notably, real estate and information service firms were more confident in their outlooks.

Japan's Machinery Orders Surge 18.9% Year Over Year in February

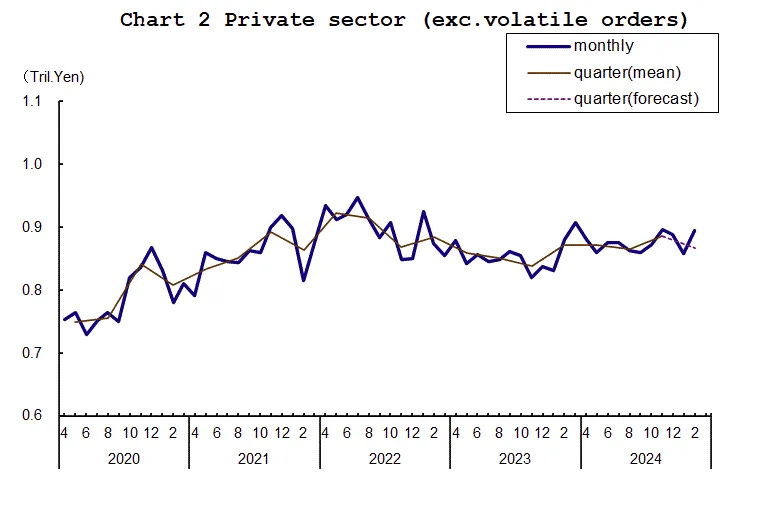

Released: April 15, 2025 18:50 - Link

In a surprise move, Japan's machinery orders rose 3.0% month-over-month and 18.9% year-over-year in February, outpacing expectations, as total private sector orders jumped 12.1% MoM, driven by a 4.3% MoM increase excluding volatile orders. Private manufacturing and non-manufacturing orders also saw significant gains, with the latter up 11.4% MoM. Foreign orders continued their upward trajectory for the third consecutive month, increasing 3.4% MoM and 15.5% YoY. While government orders have been volatile in recent months, they remain on an annual basis at 40.2% YoY, providing a notable boost to overall machinery orders numbers.

Westpac Lowers Growth Forecast as Index Shows Slowdown

Released: April 15, 2025 19:00 - Link

The latest release of the Westpac-Melbourne Institute Leading Index saw the six-month annualized rate slow to 0.6% in March, down from 0.9% in February. This represents a slowdown in growth momentum, with four key components contributing to the 0.87ppt improvement: commodity prices (+0.42ppts), widening yield spreads (+0.34ppts), improving US industrial production (+0.15ppts), and improved consumer expectations for jobs (+0.12ppts). Notably, this marked a reversal from September's -0.24% growth rate, highlighting a shift in market sentiment. Westpac has also revised its 2025 growth forecast downward to 1.9%, a decrease from the previously forecasted 2.2%.

China's Industrial Capacity Utilization Rises Sharply In Q1

Released: April 15, 2025 21:00 - Link

In a surprise move, China's Q1 industrial capacity utilization rose MoM by 0.5% to 74.1%, although it was down -2.1 ppts from Q4 2024 due to the Chinese holiday. The mining sector saw a decline of -0.4 ppts YoY to 74.6%, while manufacturing utilization increased by 0.3 ppts, reaching 74.1%. Notably, the automobile industry experienced a sharp uptick in utilization, jumping 7.0 ppts over the past year to 71.9%.

China's Fixed Asset Investment Exceeds Expectations with Strong Growth Across Industries

Released: April 15, 2025 21:00 - Link

China's fixed asset investment reported a 4.2% YoY increase in Q1 2025, beating expectations of a 4.1% rise. Public sector investment rose 6.5% YoY, while private investment grew just 0.4%. Industrial growth was particularly strong, with manufacturing up 9.1% and utility investments surging 26.0% YoY. Agricultural investment jumped 15.8% YoY, driven by a significant increase in infrastructure spending, which rose 5.8% YoY, led by water conservancy and water transportation investments that jumped 36.8% and 25.9% respectively.

China's Real Estate Investment Sector Sees Sharp Decline

Released: April 15, 2025 21:00 - Link

China's real estate investment sector saw significant declines in March, with overall development investment falling -9.9% YoY and new housing construction area shrinking -24.4% from the same period last year. Residential projects were also hit hard, seeing a -23.9% YoY drop in new construction area and a -14.7% YoY decline in completions. Commercial building sales, however, showed more resilience, with only a minor -0.4% YoY decrease in residential sales, while commercial values and areas fell -2.1% and -3.0% respectively. Notably, the available funds for developers decreased by -3.7% YoY, driven by sharp declines in self-raised funds (-5.8%) and personal mortgage loans (-7.0%).

China Sees Strongest Annual Increase in Industrial Production Since June 2021

Released: April 15, 2025 21:00 - Link

This morning's macro data saw Chinese industrial production rise 0.44% MoM, exceeding expectations, and hit a strong 7.7% YoY growth rate in March, marking the strongest annual increase since June 2021. Notably, mining production surged 9.3% YoY, driven by coal mining (+10.6%) and oil & gas extraction (+6.8%) growth. Manufacturing production also saw significant acceleration at 7.9% YoY, with high-tech manufacturing experiencing a notable jump of 10.7%. The private sector expanded at an impressive 8.2% YoY rate, while steel, iron, and cement production all saw accelerated growth in March. Strong demand for electrical vehicles continued to drive auto production up 4.9% YoY, as well as smartphone and integrated circuit production which rose 7.0% and 9.2% YoY respectively, suggesting tariff-related growth amid escalating trade tensions with the US.

Chinese Retail Sales See Strongest Annual Gain Since December 2023

Released: April 15, 2025 21:00 - Link

Chinese retail sales posted a surprise 5.9% year-over-year (YoY) gain in March, exceeding expectations by 1.7 percentage points. This marks the strongest annual increase since December 2023, driven by gains across multiple categories including food and beverage (+5.6% YoY), household appliances & A/V equipment (+35.1% YoY), recreational goods (+26.2% YoY), furniture (+29.5% YoY), and communications equipment (+28.6% YoY). While it's unclear if the broad acceleration was driven by pre-tariff spending, large electronics sales were likely impacted.

China's First-Quarter GDP Beats Expectations

Released: April 15, 2025 21:00 - Link

This morning's macro data from China provided some mixed results, with Q1 2025 GDP growth coming in at 1.2% QoQ and 5.4% YoY, narrowly beating expectations of a 1.4% QoQ increase but missing the mark on annual projections of 5.1% YoY expansion. The sectors driving growth were mining & extraction (3.5% YoY), manufacturing (5.9% YoY), and services (5.3% YoY). Agriculture also showed resilience, with planting activity up 4.0% YoY and meat production increasing 2.0%. Foreign trade was a mixed bag, with exports growing 6.9% YoY while imports fell -6.0% YoY. Notably, per capita disposable income rose 5.5% YoY nominal and 5.6% YoY real, while urban and rural nominal incomes saw 4.9% YoY and 6.2% YoY increases, respectively.

UK Inflation Steadies After February's Surge

Released: April 16, 2025 02:00 - Link

The UK CPI report for March 2025 revealed a mixed picture, with the headline rate rising 0.3% MoM (vs 0.4% expected) and 2.6% YoY (vs 2.7% expected), down from February's 2.8% YoY. Core inflation remained in line with forecasts at 0.5% MoM and 3.4% YoY, while goods inflation eased to 0.6% YoY from 0.8% previously. Notably, services inflation slowed more sharply, falling from 5.0% YoY to 4.0% YoY, with disinflation evident in key sectors such as recreation & culture (-1.0 ppts), communication (-1.3 ppts), and restaurant & hotels (-0.4 ppts).

Euro Area Current Account Posts Narrowly Below Expectations With �34 Billion Surplus

Released: April 16, 2025 04:00 - Link

The Euro Area Current Account reported a €34 billion surplus in February, below expectations but within narrow margins. The goods trade balance held steady at €34 billion, while services posted a €14 billion surplus. However, secondary income (€10 billion) and primary income (€3 billion) saw deficits, partially offsetting the overall result. Notably, the current account surplus has widened to 2.7% of euro area GDP in the past 12 months, up from 2.0% YoY. Meanwhile, financial account data showed a surge in net acquisitions of non-euro area portfolio investment securities by residents (€738 billion) and non-residents (€800 billion), reflecting strong demand for European assets.

Euro Area Inflation Slows Slightly as Energy Costs Decline

Released: April 16, 2025 05:00 - Link

The Euro Area's inflation data for March came in at 0.6% MoM and 2.2% YoY, marginally down from February's 2.3% YoY rate. Core inflation remained steady at 1.0% MoM and 2.4% YoY. Notably, energy inflation was revised downward by -0.3 ppts to -1.0% MoM, offsetting an upward revision in services that pushed the annual rate to 3.5% YoY, slightly above the initial estimate of 3.4%. Services still contribute significantly to the overall inflation rate, accounting for over 20%, albeit with a decline of 1.56 ppts from last month's contribution.

Italian March CPI Data Revisions Narrow Inflation Rate

Released: April 16, 2025 05:00 - Link

The Italian CPI data for March was released, showing a slight revision down in inflation rates compared to the initial release. Food and energy prices were both revised down to 0.0% MoM and 0.3% MoM, while services inflation was slightly increased by 0.1 ppts to 0.6% MoM. Core CPI inflation also saw a minor uptick of 0.1 ppts to 0.4%, although the YoY rate remained unchanged at 1.7%. The HICP inflation rates were in line with expectations, showing 1.6% MoM and 2.1% YoY.

Mortgage Applications Plummet in Largest Weekly Decline of 2025

Released: April 16, 2025 07:00 - Link

The MBA Mortgage Applications Composite Index plunged -8.5% WoW, marking its largest weekly decline so far in 2025, as both Refinance and Purchase indexes fell -12.4% and -4.9% WoW respectively. Despite this decline, total purchase applications remain up 9.0% MoM over the last four weeks and 30.5% YoY. Additionally, the 30-year fixed mortgage rate increased by 20 bps to 6.81%, while the 15-year fixed mortgage rate rose by 18 bps to 6.11%.

New York Fed Survey Shows Economic Outlook Slumps to Lowest Levels Since 2009

Released: April 16, 2025 08:30 - Link

The New York Fed Business Leaders Survey saw a significant downward trend in April, with the Business Activity index falling -0.5pts to -19.8, its lowest level since late 2023. The Business Climate index dropped -9.0pts to -60.7, its lowest in over four years, while the Employment index rebounded 6.0pts to 1.3 after briefly dipping below zero. Notably, the future business activity and future business climate indexes plummeted another -23.3pts and -23.1pts respectively, reaching their lowest levels since April 2020 and 2009, with the former also marking its lowest reading since April 2020. Conversely, the future prices paid index continued to rise, up 8.5pts to 71.8, its highest since the COVID supply chain crunch in 2022.

Retail Sales Make Strong Rebound

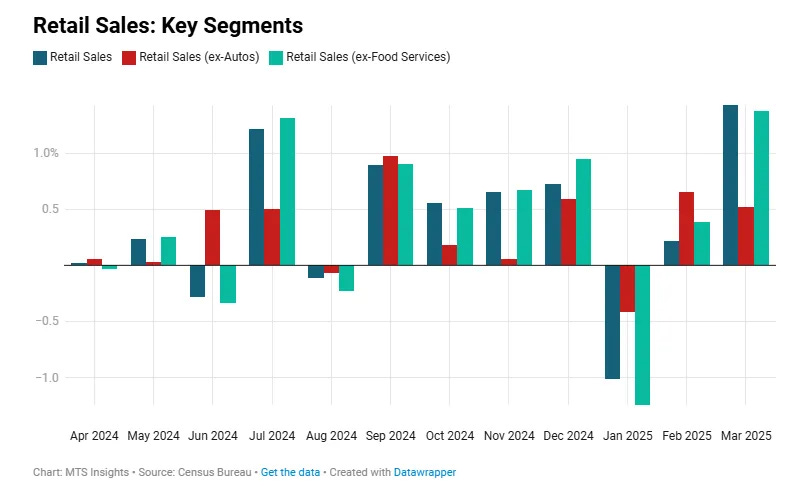

Released: April 16, 2025 08:30

US retail sales rebounded strongly in March, posting a 1.4% MoM gain, beating expectations and marking the strongest monthly increase since January 2023. The surge was largely driven by consumers front-running expected tariffs on auto imports, with auto sales surging 5.3% MoM and gas station sales declining -2.5% MoM due to falling oil prices. Excluding autos and gas, core retail sales posted a 0.8% MoM gain, while the building materials & garden equipment segment saw its largest monthly increase in four years, up 3.3% MoM. The strong result is not indicative of underlying economic strength, however, as the first-quarter growth rate suggests a weaker trend, with consumption growth showing signs of slowing down YoY and QoQ.

US Industrial Production Sees Modest Decline Amid Year-Over-Year Growth

Released: April 16, 2025 09:15

US industrial production decreased by 0.3% MoM in March but remains up 1.3% YoY. The February revision saw a slight uptick of 0.1 percentage points to 0.8% MoM, while manufacturing production grew 0.3% but was countered by a -5.8% MoM decline in utilities output. Notably, consumer goods production fell -1.0% MoM, while business equipment saw a 1.7% MoM surge. On an overall capacity utilization front, the numbers slipped -0.4 ppts to 77.8%, with manufacturing edging up 0.2 ppts to 77.3%. Q1 factory output expanded at a rate of 5.1% annually.

Bank of Canada Keeps Policy Rate Steady Amid Uncertainty Over US Trade Policies

Released: April 16, 2025 09:45 - Link

In its decision to keep policy rate at 2.75%, the Bank of Canada is exercising caution amidst heightened US trade policy uncertainty, citing increased prospects for economic growth and raised inflation expectations. While the BoC acknowledges monetary policy limitations in addressing trade tensions, it aims to maintain price stability for Canadians. The central bank has presented two scenarios highlighting differing outcomes: a weaker economy with contained inflation, or an economy weakening further resulting in higher inflation by early 2026 - a stark contrast that underscores the complexity of navigating tariffs' impacts on the inflation outlook and growth trajectory.

Builder Confidence Gains Modest Ground, Sales Expectations Show Slippage

Released: April 16, 2025 10:00

The NAHB Housing Market Index showed modest gains in builder confidence, increasing by 1 point to 40 in April, driven by a slight uptick in current sales conditions to 45 and traffic of prospective buyers, which rose 1 point to 25. However, sales expectations for the next six months decreased -4 points to 43, and price reductions remained unchanged at 5% YoY. Meanwhile, the use of sales incentives increased to 61%, up from 59% in March.

February US Business Inventories Remain Steady Despite Sales Decline

Released: April 16, 2025 10:00

US business inventories rose 0.2% MoM in February, aligning with expectations and building on the previous month's increase of 0.3%. On an annual basis, inventories are up 2.1%, influenced by two inventory builds at the start of 2025 that deviated from typical seasonal trends. Meanwhile, manufacturers' and retailers saw inventory gains of 0.1% MoM, while wholesalers increased their stockpiles by 0.3%. Notably, with sales declining in February, the inventories/sales ratio fell to 1.35x, down from 1.36x in January, as wholesale ratios also declined to 1.30x from 1.32x.

New Vehicle Affordability Hits 45-Month High

Released: April 16, 2025 10:00 - Link

In a positive start to the week for macro data, new vehicle affordability reached its best level in 45 months in March, driven largely by declining median weekly income needed to purchase an average new vehicle (down to 36.7 weeks). This improvement was also accompanied by a decrease in typical monthly payment ($739), which fell -0.2% MoM and -1.3% YoY from its peak of $795 in Dec '22, as well as a rise in income growth (3.4% YoY). Meanwhile, the average auto loan rate edged up slightly to 10.14%, albeit lower year-over-year by 45 bps. Additionally, Kelley Blue Book reported an -0.2% MoM decrease in new vehicle prices, providing further support for improved affordability.

US Crude Oil Stocks Rise 1.8% as Gasoline Levels Plummet

Released: April 16, 2025 10:30

US crude oil stocks rose by 515k barrels last week, in line with expectations, and now stand 1.8% above this time last year, a notable improvement over the previous week's decline of 3.3%. Gasoline stock levels plummeted -2.0 million barrels, exceeding forecasts, but still only 2.9% up YoY, a reversal from the 3.3% increase in the prior week. Domestic production remained steady at 13.46 million barrels per day, while net imports fell to 901k barrels per day, marking a -24.2% decline from this time last year. Refinery inputs also decreased, falling by 64k barrels per day, and total product supplied dropped slightly to 19.1 million barrels per day, with the 4-week average down -1.7% YoY.

Other data releases and commentary:

Creating a Recession to Lower Long Rates Is Not a Good Idea, Released: 04/16/2025 07:00

AAR Weekly Rail Traffic: Week of April 12th, Released: 04/16/2025 12:00