Econ Mornings: April 23rd, 2025

Macro releases and commentary released the morning of April 23nd, 2025

(all times are in EST)

Global Growth Slows Amid Declining Confidence

Released: April 23, 2025 00:00

April's S&P Global Flash PMIs revealed a complex and concerning picture of slowing private sector growth across major economies. While Japan experienced a welcome return to expansion driven by services, with improving customer demand and hiring, growth momentum elsewhere faltered. The Eurozone saw manufacturing activity unexpectedly improve, yet a contraction in services and persistently declining new orders, including a continuous drop in export orders since March 2022, dampened the overall outlook and significantly eroded business confidence. The UK composite PMI registered a sharp decline, attributable to waning demand and heightened uncertainty surrounding US tariffs, while US growth also decelerated, hampered by a pronounced drop in service exports and rising input costs fueled by tariffs and labor expenses.

Japan's Service Sector Shows Uneven Growth

Released: April 23, 2025 00:45 - Link

February's unchanged Index of Tertiary Industry Activity signals a potential softening in Japan's service sector momentum despite a robust January rebound, with overall activity up a modest 0.1% YoY. While Personal Services demonstrated strength, buoyed by a significant increase in non-essential spending, Business Services showed concerning weakness, registering the slowest growth since June 2024. Disparate sector performance characterized the month, as Finance & Insurance and Living & Amusement recorded sizable gains, offset by significant declines in Information & Communications and Transport & Postal Services, suggesting uneven underlying economic conditions.

Rising Borrowing and Debt Reach Historic Highs

Released: April 23, 2025 02:00 - Link

March's public sector net borrowing totaled £16.4 billion, reflecting a significant £2.8 billion increase YoY and contributing to a full-year borrowing figure of £151.9 billion, surpassing both prior year levels and OBR projections. While current receipts increased by £2.5 billion YoY, expenditure rose considerably more at £6.2 billion, driving a current budget deficit of £74.6 billion, a substantial £12.6 billion higher YoY, and pushing public sector net debt to 95.8% of GDP, the highest since the early 1960s, alongside a 2.6 ppts YoY rise in public sector net financial liabilities to 83.5% of GDP.

Euro Area Trade Balance Improves Significantly

Released: April 23, 2025 05:00 - Link

February's euro area trade balance registered a robust €21.0 billion, the strongest showing in over a year, fueled by a 4.5% MoM jump in exports and a 2.0% MoM rise in imports, despite a slight contraction in intra-area commerce. A significant acceleration in exports to the US, coupled with increased imports, contributed to a substantial widening of the trade balance with that nation to €23.6 billion; this represents a considerable improvement from the €14.8 billion recorded a year prior. While imports from China remain elevated, their growth rate has decelerated, while exports to China experienced a minor decline, suggesting a gradual recalibration in trade dynamics with that key partner.

Euro Area Construction Production Declines

Released: April 23, 2025 05:00 - Link

February construction production in the Euro area experienced a modest decline, contracting 0.5% MoM despite a slight 0.2% gain YoY, largely driven by substantial weakness in building construction, which fell 2.2% MoM and 3.4% YoY, and a contraction in civil engineering activity. While special construction activities showed resilience with a 0.1% MoM decrease and a 0.7% YoY increase, performance varied considerably across member states, with notable declines in Slovenia, Germany, and Poland offset by gains in Portugal, France, and Sweden.

Mortgage Applications Fall Amid Rising Rates

Released: April 23, 2025 07:00 - Link

Mortgage applications experienced a significant downturn last week, with the MBA Composite Index declining 12.7% WoW, driven primarily by a sharp 20.0% WoW drop in refinancing activity and a 6.6% WoW decrease in purchase applications. While overall application volume remains substantially higher YoY, up 17.4%, the recent weekly slide suggests a sensitivity to the upward movement in mortgage rates, which saw the 30-year fixed rate climb 9 bps to 6.90% and the 15-year fixed rate increase 9 bps to 6.20%.

Building Permits in March Revised Lower

Released: April 23, 2025 08:00

Residential construction activity demonstrated unexpected weakness in March, with finalized permit data revealing a downward revision across key indicators. The total permits issued registered at 1.467 million, a change from the initially reported 1.482 million. The monthly increase in permits was significantly curtailed, settling at a modest 0.5% MoM, a notable decline from the preliminary 1.6% estimate. Furthermore, the annual rate of change worsened considerably, now reflecting a 1.2% YoY decrease, underscoring a broader cooling trend in homebuilding despite earlier positive signals.

Canadian Housing Prices Stagnate

Released: April 23, 2025 08:30 - Link

March data on Canada's new housing price index revealed a surprising standstill, defying expectations of a modest monthly increase and suggesting a potential cooling in the sector. The index remained flat MoM, while the minimal 0.1% YoY increase signals a significant deceleration from previous periods of stronger price appreciation, potentially reflecting the impact of higher interest rates and evolving buyer sentiment within the housing market.

New Home Sales Show Unexpected Gains

Released: April 23, 2025 10:00

March new home sales demonstrated surprising strength, rising 7.4% MoM and 6.0% YoY to 724k, exceeding forecasts and marking the best performance in nearly a year. While the market remains tight, indicated by a 6.7% MoM drop in total months' supply to 8.3x, price pressures are easing, with the median sales price declining 1.9% MoM and a more substantial 7.5% YoY to $403,600. The trend of improving sales is supported by a 1.3% YoY increase in Q1 sales, and a notable shift towards more affordable options is visible, as evidenced by the 31% share of homes sold above $500k, a level not seen since August 2024.

Mixed Signals in Petroleum Data

Released: April 23, 2025 10:30

The latest petroleum data reveal a complex picture for the energy sector, with crude inventories unexpectedly rising while gasoline stocks experienced a larger-than-anticipated drawdown. While total crude stocks remain notably lower YoY, the Strategic Petroleum Reserve saw a significant build contributing to an 8.7% YoY increase in its level. Despite essentially flat domestic production and a decline in the 4-week average for refinery inputs, total products supplied demonstrated resilience, exceeding levels from a year prior, although a considerable increase in net imports is tempering overall supply trends reflected in the 4-week average being down -9.7% YoY.

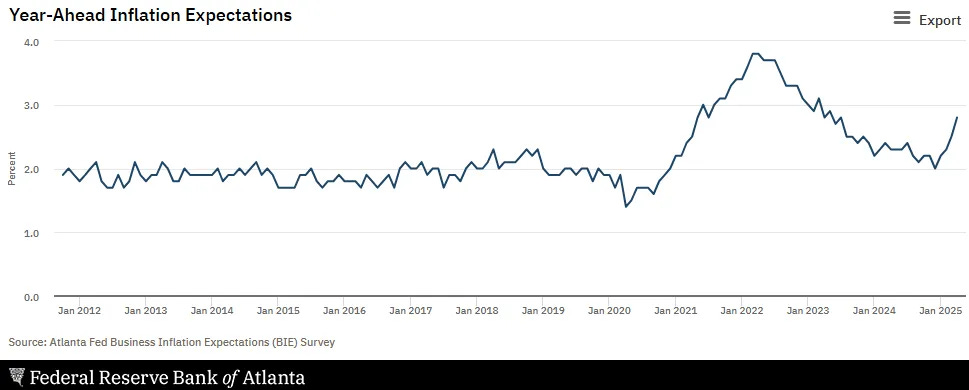

Inflation Expectations and Recession Concerns Rise

Released: April 23, 2025 11:00 - Link

Atlanta Fed business inflation expectations edged higher to 2.8% in April, fueled by declining sales and profit margins relative to typical operating conditions, despite a moderation in YoY unit cost growth to 2.2%. While firms are demonstrating some ability to pass on cost increases, responses suggest persistent challenges in maintaining pricing power, underscored by a notable shift in sentiment regarding recession risk; a quarter of respondents now express significant concern about a recession within the next year, a considerable change from earlier assessments.

US-China Tariffs Impact Container Trade

Released: April 23, 2025 12:00

The recent imposition of US tariffs on Chinese goods has triggered a pronounced slowdown in China-US container trade, despite President Trump's attempts to soften the blow with exemptions. Shippers are canceling orders due to sharply increased costs, leading carriers to aggressively blank sailings and importers to utilize existing inventories and secure bonded warehousing space while awaiting potential tariff reductions. While Asia-Europe trade appears to be gaining traction, possibly absorbing diverted Chinese exports, the US's broader trade strategy, including pressure on partners to curb trade with China and the potential for further tariff actions in July, is driving frontloading of goods elsewhere. This dynamic, coupled with the imminent end to US de minimis eligibility for Chinese imports, is contributing to a surge in air cargo rates and operational disruptions, while the potential for revised port call fees targeting Chinese carriers introduces further uncertainty and threatens to impact ocean freight costs. Overall, these actions suggest a contraction in US container import volumes for the second half of the year, although a swift de-escalation could lessen the impact.

Other data releases and commentary:

Investing Implications of Stagflation, Released: 04/23/2025 07:00

IMF Fiscal Monitor: April 2025, Released: 04/23/2025 09:00