Econ Mornings: May 22nd, 2025

Macro releases and commentary released the morning of May 22nd, 2025

(all times are in EST)

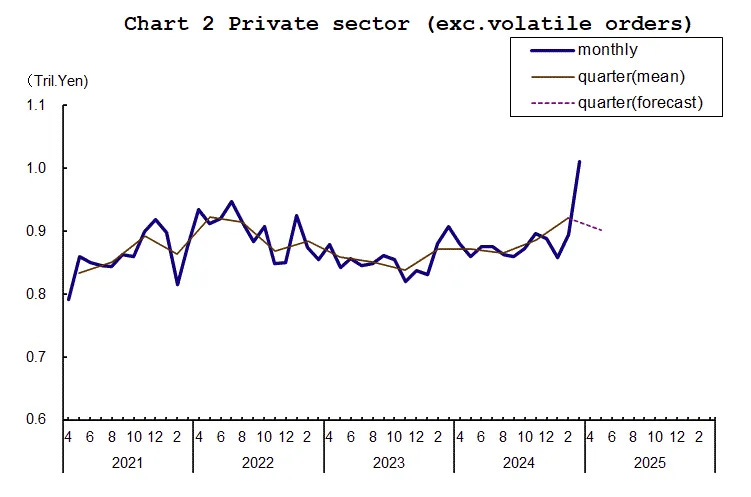

Japanese Machinery Orders Signal Mixed Trend

Released: May 21, 2025 18:50 - Link

March machinery orders in Japan registered a substantial -9.4% MoM and -1.6% YoY decline, contrasting with earlier gains in Q1, though this headline figure obscures a surprisingly robust underlying trend within the private sector. Non-volatile orders surged 13.0% MoM and 8.4% YoY, driven by strength in non-manufacturing activity, while manufacturing orders also showed positive momentum. Despite a notable -13.1% MoM drop in foreign orders, they remain up considerably on a YoY basis. Overall, Q1 private sector, non-volatile orders increased 1.3% QoQ and 7.1% YoY, with non-manufacturing leading the way; however, the immediate outlook suggests a pullback in the coming quarter, with current forecasts projecting a -2.1% QoQ and -1.0% YoY decline in private sector, non-volatile orders.

Japanese Investors Favor Debt, Sell Equities

Released: May 21, 2025 19:50

Japanese investors demonstrated a significant shift in strategy during the week ending May 17th, with a substantial ¥2,824.6 billion net purchase of foreign long-term debt, marking the largest such inflow since September 2023, while simultaneously reversing a recent trend and reporting ¥226.3 billion in net sales of foreign equities. This activity occurred alongside net foreign investment of ¥714.9 billion into Japanese equities and outflows of ¥241.4 billion from Japanese long-term debt, suggesting a divergence in investor sentiment regarding global versus domestic asset classes.

Mixed Global PMI Signals and Inflation Risks

Released: May 22, 2025 00:00

May's S&P Global Flash PMIs revealed a mixed global picture, with Japan experiencing a slight contraction in private sector activity, driven by weakened service and manufacturing output, while India's expansion continued to strengthen. The Eurozone saw private sector growth soften to a six-month low, partially offset by an improvement in manufacturing, though services activity declined to a 16-month low. In contrast, the US saw a rebound in private sector growth, spurred by improvements in both manufacturing and services, though a notable drop in service exports and a surge in price pressures, particularly for manufacturers and services, suggest underlying inflationary risks and potentially warrant closer monitoring of future data releases.

UK Borrowing Exceeds Expectations

Released: May 22, 2025 02:00 - Link

April 2025 public sector borrowing landed at £20.2 billion, exceeding expectations and marking the fourth-highest figure for the month on record, reflecting persistent fiscal pressures. While the current budget deficit narrowed slightly YoY to £13.9 billion, driven by a decline in debt interest, overall borrowing was bolstered by robust receipts, particularly a £3.6 billion rise in tax revenues, which were nonetheless outpaced by increased departmental spending and benefit payments. Year-to-date, total borrowing for FYE March 2025 reached £148.3 billion, surpassing both prior year levels and Office for Budget Responsibility projections, pushing the net debt burden to 95.5% of GDP.

French Retail Sales Show Signs of Recovery

Released: May 22, 2025 02:45 - Link

April retail sales in France showed a welcome rebound, increasing 0.5% MoM after a stagnant March, driven by gains in both food and manufactured goods. Strong performance in discretionary categories like DIY, furniture, and bikes & motorcycles, which had previously struggled, suggests a potential shift in consumer spending patterns. While the three-month average sales were modestly higher, only up 0.5% QoQ, the latest data offers a tentative sign of renewed momentum in the French consumer landscape after a soft start to the year.

French Business Climate Weakens Amid Sector Disparities

Released: May 22, 2025 02:45 - Link

France's overall business climate indicator deteriorated in May, slipping 0.7 points to 95.8, signaling persistent headwinds despite mixed sector performance. Services and manufacturing sectors experienced notable declines, evidenced by weakening activity expectations and order books, with the services workforce expectation hitting a multi-year low; however, supply-side pressures eased somewhat. While wholesale trade showed modest gains on the back of better past sales, retail trade rebounded from a significant prior downturn due to improved sentiment and workforce expectations, and construction registered a substantial uptick fueled by a surge in future activity prospects, suggesting potential for future growth within that sector.

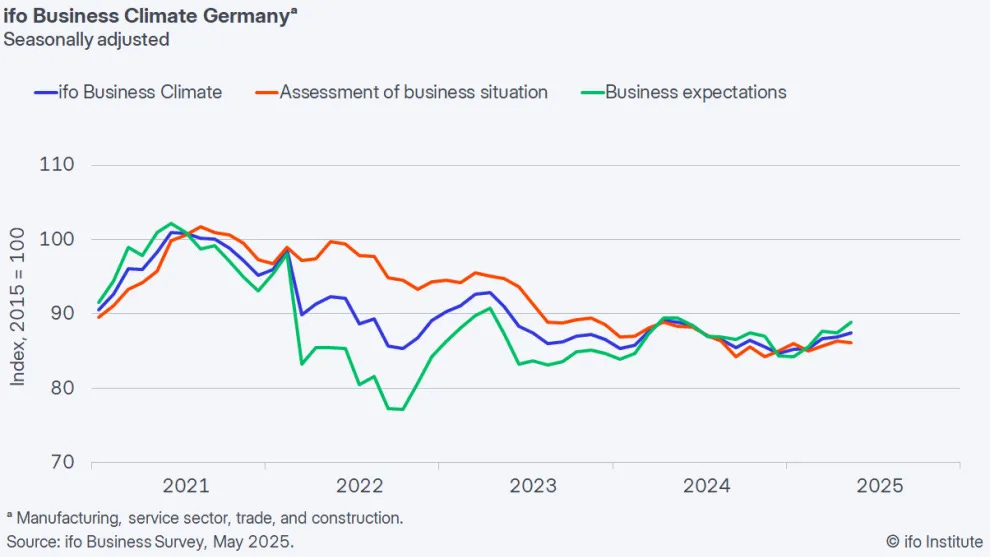

German Economy Shows Signs of Improvement

Released: May 22, 2025 04:00 - Link

Germany's macroeconomic outlook appears to be gaining traction, as evidenced by a May ifo Business Climate Index rise to 87.5, surpassing forecasts and marking its strongest reading since June 2024. While current conditions edged slightly lower, a substantial increase in expectations across multiple sectors points to an improving sentiment. Manufacturing and trade are showing particular strength, benefiting from stabilized order intake and positive assessments, respectively, alongside a notable upswing in the food industry. Even with a slight pullback in chemicals, the broad-based improvement, including a two-year high in construction, suggests a cautiously optimistic trajectory for the German economy.

OECD Economic Growth Decelerates

Released: May 22, 2025 06:00 - Link

The OECD experienced a marked deceleration in economic activity during Q1 2025, with overall GDP growth registering a modest 0.1% QoQ, considerably lower than the 0.5% QoQ observed in the previous quarter. This slowdown was broad-based, particularly impacting the G7 where growth similarly weakened to 0.1% QoQ, driven by contractions in both Japan and the United States. Annual growth figures also reflected this cooling, with the OECD reporting 1.6% YoY and the G7 posting 1.5% YoY, downward revisions from prior estimates. The weakening trend was widespread across the OECD, with a majority of economies exhibiting slower growth rates compared to the prior quarter, including four that slipped into negative territory.

UK Manufacturing Activity Contracts

Released: May 22, 2025 06:00 - Link

UK manufacturing activity is experiencing a concerning contraction, with output volumes plummeting to the lowest level since late 2020, driven by broad-based declines across numerous sub-sectors and depressed order books that remain significantly below historical averages despite a slight improvement in export orders. Rising input costs and ongoing uncertainty surrounding US tariffs are contributing to a palpable lack of customer spending and dampened sentiment within the sector, suggesting further output weakness is likely through the summer months while finished goods inventories remain marginally elevated.

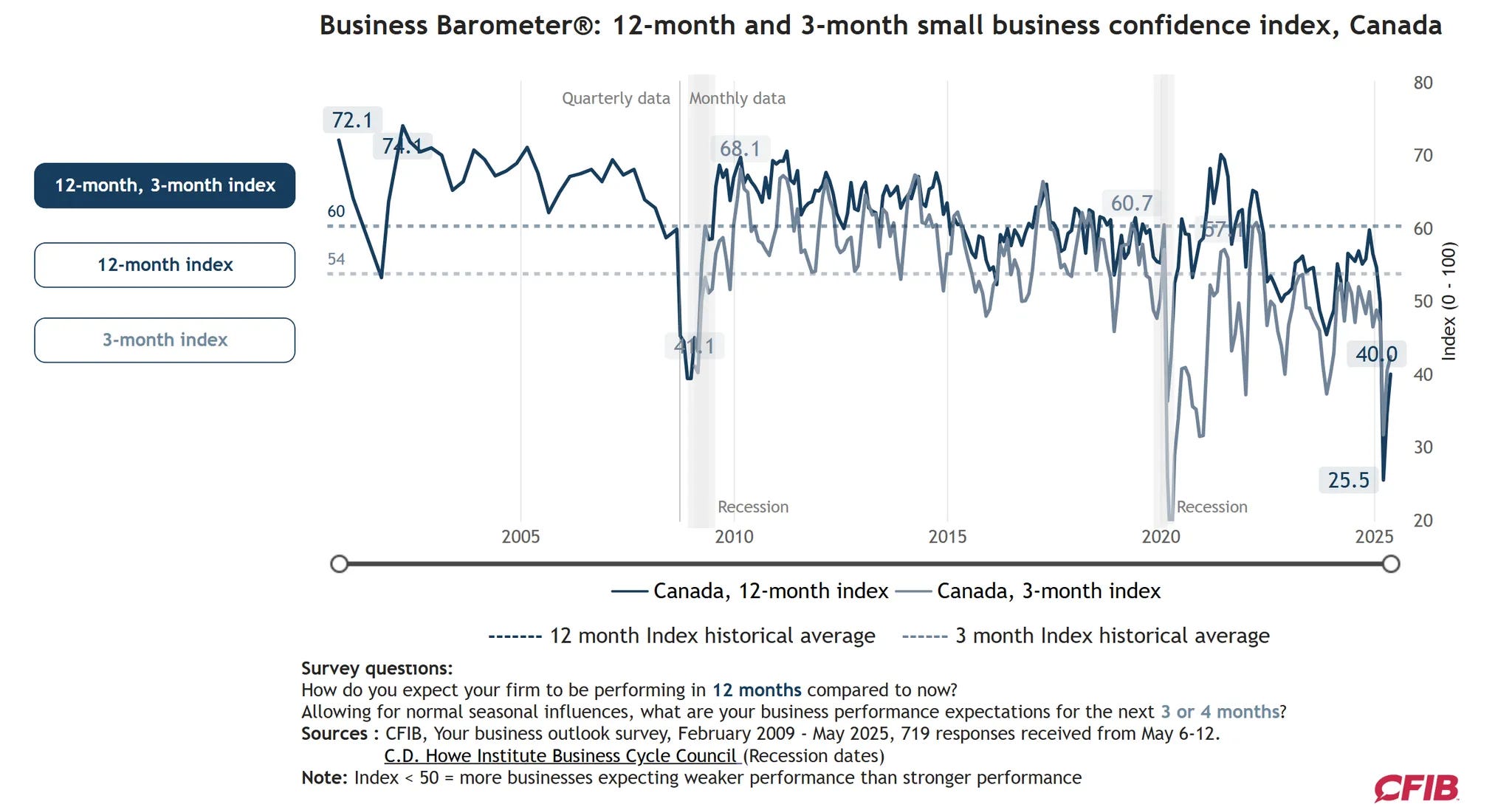

Canadian Small Business Sentiment Shows Slight Improvement

Released: May 22, 2025 07:00

Canadian small business sentiment, as measured by the CFIB Barometer, improved modestly in May, with both short-term and 12-month optimism indexes displaying gains despite remaining in pessimistic territory. Lower price increase expectations, alongside stable wage growth plans, suggest easing inflationary pressures, though challenges related to insufficient demand persist as the dominant concern for SMEs. While certain sectors like manufacturing and hospitality experienced notable confidence improvements, hiring intentions remain cautious, and businesses engaged in international trade continue to express considerably lower optimism compared to their domestic-focused counterparts, highlighting ongoing economic headwinds.

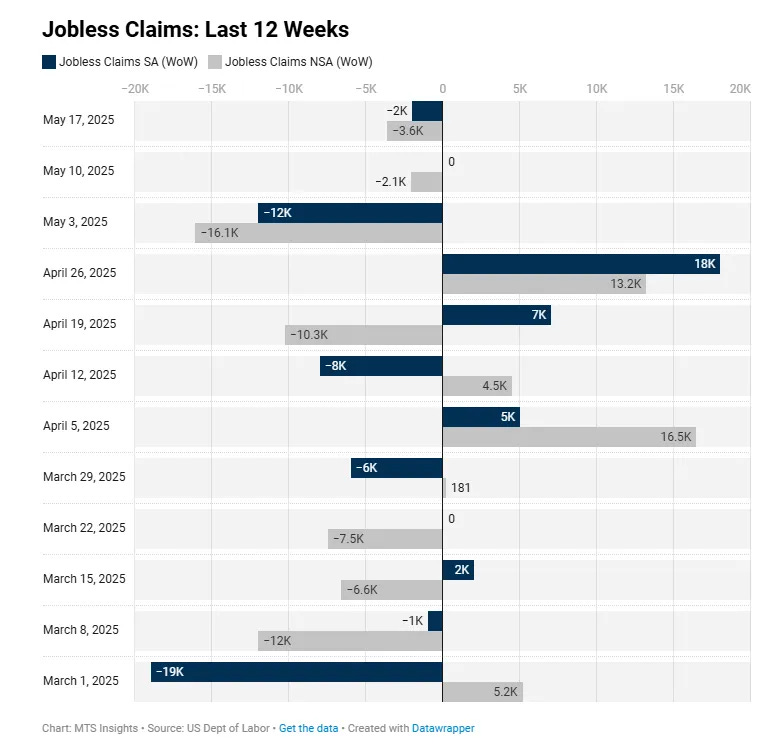

US Labor Market Shows Mixed Signals

Released: May 22, 2025 08:30

The latest unemployment insurance data reveal a mixed picture of the US labor market. While initial jobless claims declined to 227k, driven by a stronger-than-expected not seasonally adjusted figure, continued claims unexpectedly rose to 1.903 million, suggesting a potential slowdown in re-employment. The insured unemployment rate remained steady, but elevated federal employee claims and a notable spike in Virginia due to manufacturing layoffs indicate persistent pockets of vulnerability within the broader economy, complicating assessments of the labor market's overall health.

Chicago Fed Index Signals Economic Slowdown

Released: May 22, 2025 08:30

April's Chicago Fed National Activity Index reading of -0.25 suggests a deceleration in economic activity relative to recent months, with several key components signaling moderating growth. While the CFNAI-MA3 held steady, the diffusion index weakened, and production-related indicators saw a noticeable downward revision. Sales, orders, and inventories also contributed negatively, reversing prior gains, while personal consumption and housing demonstrated a similar trend. Though employment indicators offered a marginal positive contribution, the overall picture points to a slowing pace of expansion and potential headwinds impacting several areas of the economy.

Canada's IPPI Signals Moderating Inflation

Released: May 22, 2025 08:30 - Link

April's industrial price data revealed a concerning shift in Canada's macroeconomic landscape, as the IPPI posted its first monthly decline in seven months, falling -0.8% MoM despite a still-elevated 2.0% YoY increase. This broad-based weakness was principally driven by significant drops in energy and petroleum products, primary non-ferrous metals, and lumber, attributable to lower crude oil prices and a stronger Canadian dollar. While food-related product prices demonstrated resilience with MoM increases, the accompanying -3.0% MoM and -3.6% YoY decline in the Raw Materials Price Index, especially when considering the considerable drop in crude energy products, suggests moderating inflationary pressures and potential headwinds for commodity-dependent sectors, even as certain precious metal ores show persistent strength YoY.

Container Rates Rise Amid Trade Policy Shifts

Released: May 22, 2025 09:45

The Drewry World Container Index rose 2% WoW to $2,276, building on last week's 8% surge, primarily driven by a 4% WoW rate increase on routes from Shanghai to Genoa and New York. This continued upward pressure on spot rates is anticipated to persist into next week, spurred by recent shifts in US-China trade policy and the subsequent need for container lines to adjust capacity in response to rising cargo bookings originating from China.

US Services Show Mixed Quarterly Performance

Released: May 22, 2025 10:00

Q1 2025 saw a mixed performance for US selected services, with seasonally adjusted revenue growing 1.0% QoQ and a robust 5.6% YoY, though unadjusted figures declined -1.8% QoQ. While overall growth was supported by a significant rebound in utilities revenue, climbing 10.5% YoY compared to 2.8% in the prior quarter, the information services sector presented a more nuanced picture, experiencing a -3.4% QoQ decrease despite a strong 7.1% YoY rise driven by software publishing gains that partially compensated for weakness in telecom and related areas.

April Existing-Home Sales Decline

Released: May 22, 2025 10:00 - Link

April existing-home sales weakened, falling -0.5% MoM and -2.0% YoY to 4.00 million units, underscoring ongoing headwinds despite a substantial increase in housing inventory, up 9.0% MoM and 20.8% YoY to 1.45 million units and representing 4.4 months' supply. While the median existing-home price reached a record $414,000, a 1.8% increase YoY, single-family sales also declined, though first-time buyers comprised a notable 34% of purchases, and days on market slightly lengthened from the prior month. The continued rise in inventory is slowly shifting the market dynamic, reducing the advantage for sellers, although it maintains a mild seller's market.

Chicago Fed Survey Shows Divergent Economic Signals

Released: May 22, 2025 10:00

May's Chicago Fed Survey paints a mixed picture of economic progress, with the overall Activity Index showing a substantial rebound from deeply negative readings, though growth remains close to trend. While nonmanufacturing activity demonstrated considerable strength, the manufacturing sector experienced a sharp contraction, creating a divergence in sectoral performance. Despite this improvement, a significant portion of respondents still anticipate reduced activity over the coming year, and concerns persist regarding capital spending and hiring, alongside rising nonlabor cost pressures, suggesting underlying caution regarding a sustained recovery.

Natural Gas Storage Exceeds Five-Year Average

Released: May 22, 2025 10:30

Last week's natural gas storage report revealed a build of 120 Bcf, aligning with market forecasts and contributing to overall inventories of 2,375 Bcf. While the drawdown remains substantial, the year-over-year deficit narrowed from -14.3% to -12.3%, indicating a moderation in the pace of depletion. Notably, storage levels are now exceeding the five-year average by 3.9%, a significant improvement from last week's 2.6% surplus, suggesting a shift in the supply-demand dynamics influencing natural gas markets.

Tenth District Manufacturing Contracts

Released: May 22, 2025 11:00 - Link

The Kansas City Fed's May survey reveals a persistent, albeit moderated, contraction within the Tenth District manufacturing sector, characterized by a Composite Index at -3. Production and new orders experienced notable declines, alongside a significant drop in export demand, and a concerning backlog of orders, outweighing a slight increase in employment. Easing price pressures on both inputs and finished goods offer some relief, but a majority of firms maintain consistent hiring and capital expenditure plans, while a substantial portion anticipates reductions, signaling cautious expectations for the remainder of 2025.

Gasoline Prices Remain Low Amidst Oversupply

Released: May 22, 2025 12:00 - Link

Gasoline prices experienced a slight increase of 0.3 cents to $3.195 last week, marking a modest MoM rise but remaining significantly below last year's levels, down 41.5 cents YoY. This current pricing environment, the lowest seen for Memorial Day since 2021, reflects a market where crude oil supply is outpacing demand, contributing to the relative affordability at the pump.

Other data releases and commentary:

The Negative Impact of Tariffs on Earnings, Released: 05/22/2025 07:00

ECB Monetary Policy Account: Meeting of 16-17 April 2025, Released: 05/22/2025 07:30