Econ Mornings: May 6th, 2025

Macro releases and commentary released the morning of May 6th, 2025

(all times are in EST)

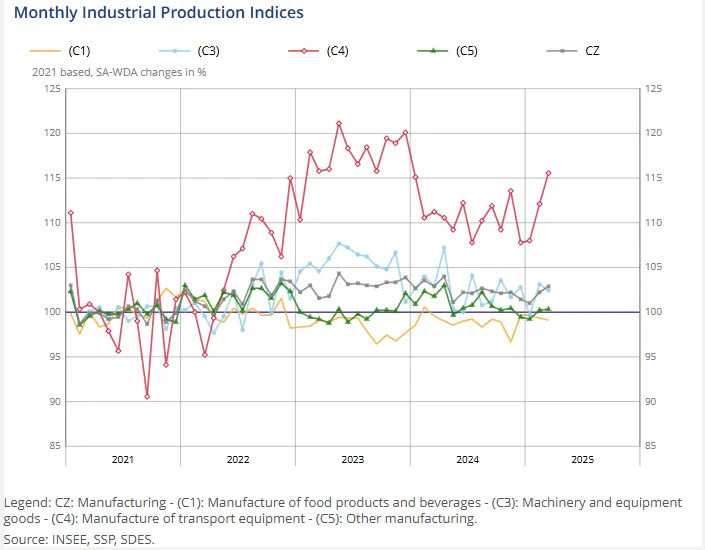

French Industrial Production Shows Mixed Signals

Released: May 06, 2025 02:45 - Link

March industrial production in France edged up 0.2% MoM, falling short of anticipated gains, though buoyed by robust expansion in transport equipment and energy products. While manufacturing activity increased 0.6% MoM, it remains considerably down -1.0% YoY, revealing persistent headwinds. The report highlights a concerning divergence, as food and machinery production contracted, and the construction sector continues to struggle with a -0.9% MoM decline and a more substantial -4.0% YoY drop. Notably, energy-intensive industries, including iron and steel and basic chemicals, demonstrated significant weakness relative to 2021, suggesting ongoing challenges related to energy costs and global demand.

German Car Market Weakens, EV Adoption Surges

Released: May 06, 2025 03:00 - Link

German passenger car registrations in April 2025 revealed a continuing softening in the market, with new registrations declining 0.2% YoY, marking the sixth consecutive period of annual contraction. While commercial registrations maintained stability, falling only marginally YoY at -0.7%, private registrations showed resilience with a 1.1% YoY increase. This shift in demand is mirrored in the changing powertrain mix, as gasoline car registrations plummeted -26.4% YoY, while electric vehicle adoption accelerated, capturing 18.8% of the total market and posting a robust 53.5% YoY gain.

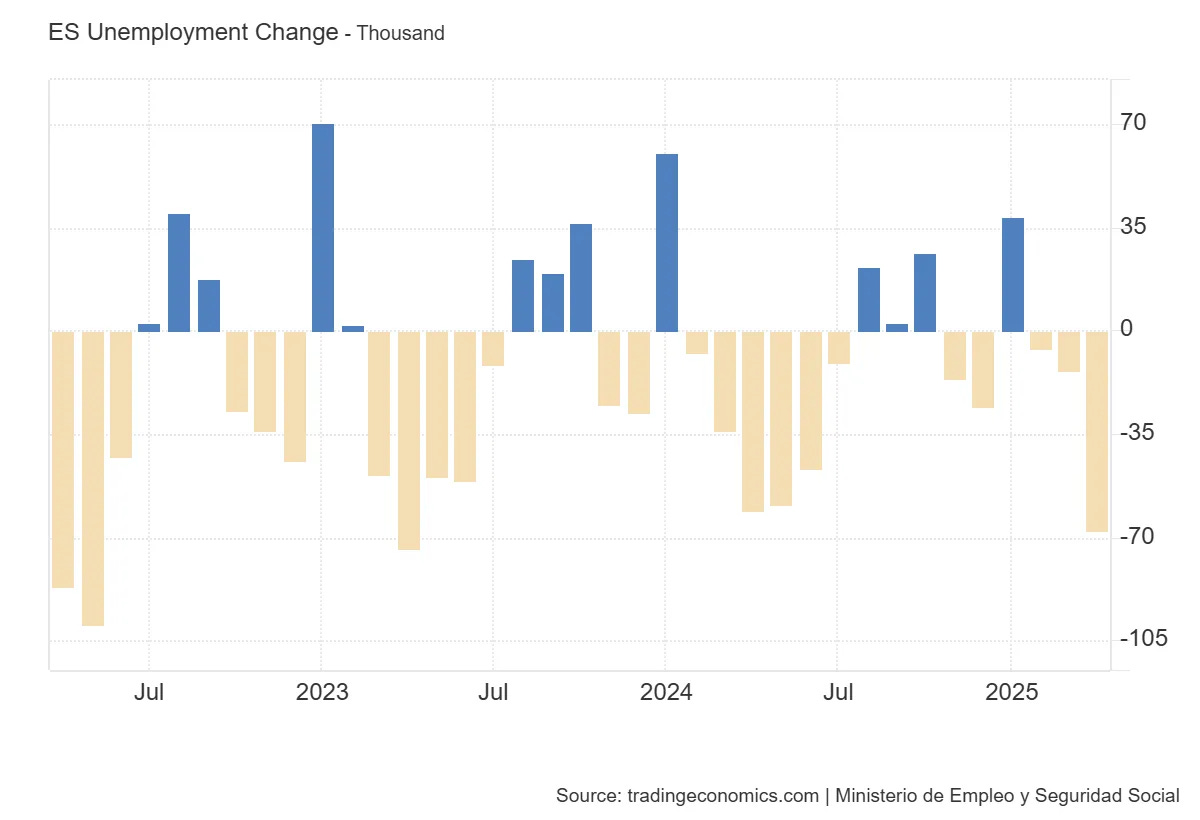

Spain's Unemployment Declines to 17-Year Low

Released: May 06, 2025 03:00 - Link

April's labor market data for Spain reveal a notably positive shift, with total unemployment decreasing by 67.4k, representing a substantial 2.61% MoM drop, the most significant decline observed in over two years. This improvement has brought registered unemployment to 2.51 million, the lowest level in nearly seventeen years, largely driven by a considerable contraction of 49.7k, or 2.66% MoM, within the services sector, suggesting a strengthening of domestic demand and overall economic activity.

UK Light Commercial Vehicle Registrations Decline

Released: May 06, 2025 04:00 - Link

UK light commercial vehicle registrations experienced a sharp contraction in April, falling -14.9% YoY to 20,332 units, reflecting broader economic headwinds and impending regulatory shifts. The decline was broad-based, with large vans seeing the steepest drop at -22.9%, although smaller vans also posted losses. Countering the overall trend, pickup and 4x4 registrations saw notable increases, possibly anticipating April's tax changes. While battery electric van uptake demonstrated positive momentum with a 77.5% YoY rise, representing 8.3% of the market, the industry remains concerned that evolving tax policies and grid infrastructure limitations threaten the pace of decarbonization efforts needed to meet the 16% 2025 mandate.

UK Car Registrations Decline Amidst BEV Growth

Released: May 06, 2025 04:00 - Link

April's UK new car registrations experienced a significant -10.4% YoY decline to 120,331 units, reflecting broad-based weakness across private, fleet, and business buyers, and extending the recent trend of contraction. While battery electric vehicle (BEV) registrations saw a positive 8.1% YoY increase, capturing 20.4% market share, this remains below the mandated target and highlights the need for further stimulus to bolster electric vehicle adoption. Plug-in hybrid electric vehicle (PHEV) sales demonstrated notable strength, increasing 34.1% YoY, though hybrid electric vehicle (HEV) and conventional powertrain vehicles continued to suffer substantial losses. Despite the concerning April figures, the year-to-date market is up 3.1%, driven by robust BEV growth of 35.2%, suggesting ongoing fragility in consumer confidence and the need for sustained policy support.

Eurozone Lending Conditions Ease

Released: May 06, 2025 04:00 - Link

Eurozone lending conditions eased in March, as evidenced by a significant -19 bps drop in the new corporate loan rate to 3.93%, the lowest level in nearly two years, while mortgage rates remained steady. Corporate deposit rates also saw declines, notably a -17 bps MoM reduction in the composite rate with agreed maturity to 2.33% and a -5 bps MoM decrease in overnight deposit rates. Household deposit rates followed a similar, albeit milder, trend, with the composite rate falling -10 bps to 2.11% and overnight rates showing little movement, suggesting easing monetary policy is gradually impacting both lending and savings across the region.

Euro Area Producer Prices Continue to Decline

Released: May 06, 2025 05:00 - Link

Euro area producer prices declined further in March, with the headline PPI falling 1.6% MoM, slightly below expectations, while still registering a 1.9% rise YoY, a moderation from previous readings. The slowdown in producer inflation was broad-based, with energy prices plummeting 5.8% MoM despite remaining 7.6% higher YoY, and excluding energy, PPI rose only 1.3% YoY. Gains in consumer-facing goods, particularly non-durables up 0.5% MoM, offered some offset to the weakness in intermediate and capital goods, which saw minimal change.

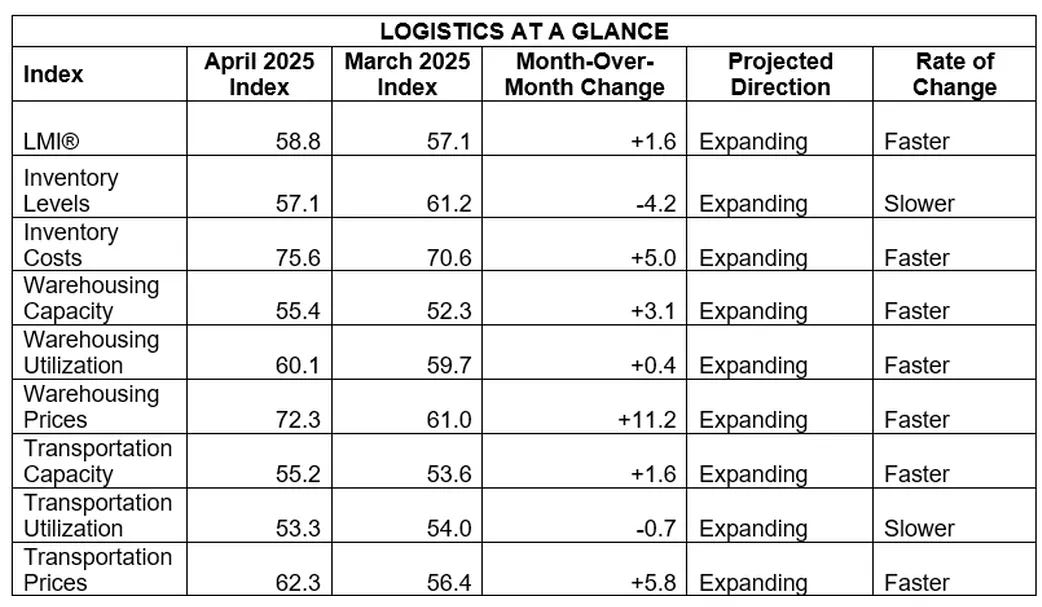

Diverging Inventory Expectations Highlight Supply Chain Discrepancies

Released: May 06, 2025 06:00 - Link

April's Logistics Managers' Index advanced to 58.8, signaling continued expansion despite a deceleration in inventory levels to 57.1, partially attributable to the dissipation of earlier tariff-related accumulation. Rising storage and transportation costs, with warehousing prices surging 11.2 pts and transportation prices up 5.9 pts, are indicative of increasingly expensive inventory that is not rapidly moving through the supply chain. While upstream firms foresee a significant reduction in inventories over the coming year, downstream respondents anticipate a substantial inventory build, revealing a widening divergence in expectations between industrial caution and retail optimism, supported by forecasts for sharp increases in downstream inventory and warehousing costs.

Canada’s Merchandise Trade Deficit Shrinks in March

Released: May 06, 2025 08:30 - Link

Canada's merchandise trade deficit significantly eased in March, driven by a contraction in both exports and imports, though the dynamics were uneven. While overall exports edged down 0.2% MoM, influenced by a notable 6.6% decline in shipments to the US due to new tariffs, exports to non-US markets experienced a robust 24.8% surge. Weakness in consumer goods, particularly meat and pharmaceuticals, and a pullback in energy exports, notably nuclear fuel and natural gas, were partially offset by a rebound in motor vehicles. The decline in imports, the first since September 2024, was spearheaded by substantial drops in energy and metals/minerals, reflecting a cooling in domestic demand and reduced reliance on US-sourced goods.

Record Trade Deficit Signals US-EU Economic Shift

Released: May 06, 2025 08:30 - Link

March's trade deficit reached a record $140.5 billion, driven by a surprisingly large 4.4% MoM surge in imports, including record levels of capital and consumer goods, largely attributable to anticipatory front-loading ahead of anticipated reciprocal tariffs and heightened uncertainty regarding US-EU trade relations. While export growth was modest, increasing just 0.2% MoM, the widening deficit reflects a significant increase in imports from key European economies and a concerning decline in US travel services exports, potentially signaling a broader decoupling of US-EU business relationships amid looming trade negotiations and the threat of substantial EU tariffs.

Canadian Business Sentiment Declines

Released: May 06, 2025 10:00

April's Ivey PMI revealed a notable softening in Canadian business sentiment, dropping sharply to 47.9, the lowest level in several months, signaling a potential slowdown in economic activity. This contraction was underscored by a worrying decline in the Employment Index, hitting a more than two-year low, while a slight increase in inventories and quicker supplier deliveries suggest ongoing adjustments within supply chains. Although price pressures appear to be easing, as evidenced by the Prices Index's significant MoM drop, readings remain elevated compared to historical averages, hinting at persistent inflationary headwinds that could restrain future growth.

Easing of Global Supply Chain Pressures

Released: May 06, 2025 10:00

April's Global Supply Chain Pressure Index (GSCPI) registered -0.29, marking a further decrease from March's revised reading of -0.17 and signaling continued easing of supply chain bottlenecks. This decline, measured as standard deviations from the historical average, suggests that pressures impacting global trade and production are still diminishing, albeit at a slower pace than previously observed.

Consumer Sentiment Declines Amid Financial Stress

Released: May 06, 2025 10:00 - Link

May's RCM/TIPP Economic Optimism Index revealed a concerning shift in consumer sentiment, declining 2.4% MoM to 47.9 amid broad-based weakness across both near-term and longer-term outlooks. The pronounced drop in sentiment, particularly among non-investors, was accompanied by a significant uptick in the Financial-Related Stress Index, reaching its highest level since late 2023, suggesting growing financial pressures are impacting households. Despite a minor improvement in confidence regarding Federal policies, the persistent readings below 50.0 and the overall decline in optimism indicate lingering anxieties about the economic trajectory.

EIA Outlook: Slowed GDP Growth and Energy Trends

Released: May 06, 2025 11:00

The EIA's latest Short-Term Energy Outlook signals a muted economic landscape, evidenced by downward revisions to both U.S. and world GDP growth, now projected at 1.5% and 1.6% for 2025 and 2026, respectively, largely attributable to new trade policy and broader global trade friction. Despite unchanged forecasts for global liquid fuels production, the outlook anticipates lower inventory builds in 2025 and increased builds in 2026, reflecting evolving supply-demand dynamics. Concurrent with these developments, the report highlights rising coal inventories and production expectations, with U.S. coal production anticipated to reach 506 million short tons in 2025 and 475 million in 2026, spurred by increased power generation needs.

Other data releases and commentary:

Australia Household Spending: March 2025, Released: 05/05/2025 19:30

After Liberation Day, Released: 05/06/2025 07:00

March U.S. International Trade: An Imports Surge Led To Another Record Trade Deficit, Released: 05/06/2025 11:30