Euro Area GDP Growth Remains Sluggish in Q1 2023, Hampered by Weak Consumption and Productivity

Economic news and commentary for June 8, 2023

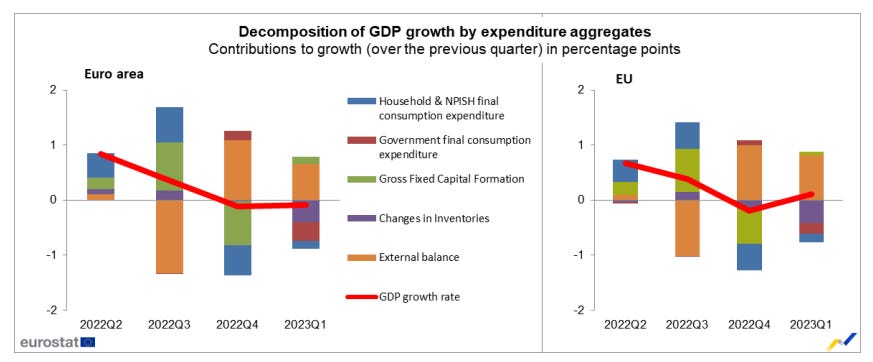

Euro Area GDP

The Euro area's GDP growth in Q1 2023 confirmed a sluggish expansion of 0.1% quarter-on-quarter (QoQ). The lackluster performance was primarily attributed to a decline in household and government consumption, resulting in a negative impact on overall GDP. Although gross fixed capital formation saw marginal growth and trade remained steady, the release of excess inventories by firms weighed down the economy.

Euro area household consumption experienced a decline of -0.3% QoQ in Q1 2023, while government consumption fell by a sharper -1.6% QoQ. Combined, these factors contributed to a -0.4 percentage point (ppt) drag on GDP growth. Gross fixed capital formation, on the other hand, recorded a modest growth of 0.6% QoQ. The slight increase in capital formation, coupled with a decline in imports (-1.3% QoQ) and stagnant exports, drove the marginal overall growth observed.

Trade played a crucial role in driving euro area growth during the quarter. The trade sector made a significant positive contribution, accounting for a 0.7 ppt boost to GDP growth. Meanwhile, firms' decision to release excess inventories had a substantial negative impact, resulting in a -0.4 ppt drag on the economy. The adjustment of inventory levels reflects a cautious approach by businesses and their response to uncertain market conditions.

Euro area productivity faced ongoing challenges, posing a significant roadblock for the ECB's inflation management objectives. With employment growing at a faster pace than GDP, productivity suffered in Q1 2023. Labor productivity declined by -0.6% QoQ based on the number of employees and by -0.9% QoQ based on hours worked. Weak productivity levels constrain the potential for economic expansion and hinder efforts to tame inflationary pressures. The persistently weak productivity growth poses a significant challenge for the ECB as it strives to address inflationary concerns. Insufficient gains in productivity limit the potential for economic expansion and make it challenging to bring down inflation to desired levels.

Still to come…

10:00 am (EST) - US Wholesale Inventories

10:30 am - US EIA Natural Gas Report

4:30 pm - US Fed Balance Sheet

9:30 pm - China CPI & PPI

Morning Reading List

Other Data Releases Today

Australia's trade balance dropped -$3.6 bil to $11.2 bil in April with exports down -5.0% MoM and imports up 1.6% MoM. Goods exports continues to decline from a Jun 2022 peak, down another -7.0% MoM as demand for general merchandise declines.

Japan's Q1 2023 GDP growth sees a strong upgrade from 0.4% QoQ to 0.7% QoQ.

Upgrades in inventories and private non-residential investment which grew 1.4% QoQ instead of 0.9% QoQ were the reason for the revision.

The Reserve Bank of India keeps its policy rates unchanged after inflation improved in March and April. The RBI remains in data-dependence mode as it vows "to take further monetary actions promptly and appropriately as required..."

French employment increased 0.3% QoQ, or 92,400 jobs, in Q1 2023. This tops the previous quarter's growth of 55,400. The services sector added a majority of the jobs, growing by about 85,400 jobs. The goods sector added just 8,200 jobs.

Jobless claims grew 2,000 to 232,000 last week. The insured unemployment rate was unchanged at 1.2%. Total continued claims grew 6,000 to 1.80 million.

Euro Area GDP

Eurozone in technical recession after all (ING) - The latest revisions of the GDP figure for the first quarter resulted in a 0.1% drop. That makes for a second decline in a row. These declines are so minimal that current economic circumstances are better described as broad stagnation.

Australia GDP

Australia: GDP slows further (ING) - Further moderation of growth should support the idea that the restrictive rates policy is working and that further hikes are unnecessary - all we now need is for inflation to fall...

Bank of Canada Announcement

Bank of Canada delivers surprise 25 basis point hike (TD Bank) - The Bank of Canada raised the overnight rate by 25 basis points, to 4.75%, while stating that it will continue with Quantitative Tightening (QT).

Bank of Canada surprises with a hike and hints at more to come (ING) - The Bank of Canada has resumed interest rate increases after a five-month hiatus. Demand is proving to be more resilient and inflation could be more persistent. Another hike looks likely in July, but we are wary about pushing for more aggressive action. The attractive risk-adjusted carry can keep CAD in investors' favour for longer.

Bank of Canada does some fine tuning (CIBC) - The Bank of Canada opted to act now rather than wait for a revised forecast, but its rate 25 basis point rate hike had the appearance of to a fine tuning move rather than the start of an extended addition to the prior course of tightening. Although it lifted the overnight rate to 4.75%, it opted not to state that with that additional hike, rates might not yet be high enough to do the job. That suggests that it's again now going to take some time to see how the data evolve.

US

Balancing a brokered hawkish pause on a tightrope (EY Parthenon) - The Federal Reserve’s brokered hawkish pause will be put to the test at the upcoming Federal Open Market Committee (FOMC) meeting. Extreme data point dependence has convinced Fed hawks that additional rate hikes are warranted given the unacceptably slow cooling of inflation.

Export Flop Causes U.S. Trade Deficit to Widen to Six-Month High (Wells Fargo) - U.S. exports slipped by the most since pandemic-related lockdowns in 2020 in April, pushing the U.S. trade deficit to its widest in six months. Some one-off factors are to blame for the weakness, but the data continue to demonstrate an unusual volatility in trade flows. Net exports are tracking to be a meaningful drag on Q2 GDP growth.

The Trade Deficit in Goods and Services Came in at $74.6 Billion in April (First Trust Portfolios) - The trade deficit in goods and services rose to $74.6 billion in April as exports declined while imports grew. We like to focus on the total volume of trade, imports plus exports, as it represents the extent of business and consumer interactions across the US border. This measure fell by $4.4 billion in April, is down 3.2% versus a year ago, and is now 4.2% lower than last year's peak in June.

Europe

ECB Watch: Not sufficiently restrictive yet (Nordea) - The ECB will continue on a path of 25bp rate hikes next week, and we think such a path will extend at least to the July meeting. New staff forecasts are set to illustrate that inflation is not under control yet.

Norway: Our updated Norges Bank and NOK calls (ING) - Norges Bank kept trimming daily FX purchases, but not enough to turn the tide for the weak Norwegian krone. NOK’s underperformance is what will – in our view – prompt hikes beyond the projected peak, to 3.75% or potentially even 4.00%. We expect the undervalued NOK to outperform in 2H23 thanks to a risk sentiment improvement and solid fundamentals.

Poland: Rising chances for a 2023 rate cut (ING) - During his press conference, National Bank of Poland Governor Glapiński underlined a further decline in inflation and emphasised that it has fallen by more than 5 percentage points since its peak in February. Current data and NBP rhetoric suggest that the odds of a 2023 rate cut have soared to about 50%, which we find a bit premature.

Canada

Canada's Trade Accounts Register Healthy Surplus in April (TD Bank) - Canada's merchandise trade account registered a $1.9 billion surplus in April. This comes after March's surplus was revised down to $231 million and marks the largest Canadian trade surplus since June 2022.

PMI

Financial services lead global growth higher in May, stoking inflation (S&P Global) - S&P Global PMI survey data show global growth to have been led by the financial services industry in May, for which a broad-based upturn was recorded across the US, Europe and Asia. Demand for financial service grew at the steepest rate since 2014, with new business placed at banks surging at rate amongst the quickest since comparable data were available in 2009.

Trade

Tighter fit: Resilience versus cost in apparel supply chains (S&P Global) - Supply chain managers are emerging from a period of upheaval driven by the pandemic and now have to make decisions about their long-term supply chain structures in the face of a weak economy and high interest rates.

Agriculture

Key crops on the move amid rising weather concerns (Saxo Bank) - The grain and soybean sectors have started June with strong gains, led by growing concerns that a current dry spell across Northern Europe, the Black Sea region, and parts of the US may negatively impact this year's crop production.

Subscribe to receive Econ Mornings every weekday at 9 am. More economic and finance content on Twitter, Reddit, and my website.