Euro Area Retail Sales Bounce Back in January

Economic news and commentary for March 6, 2023

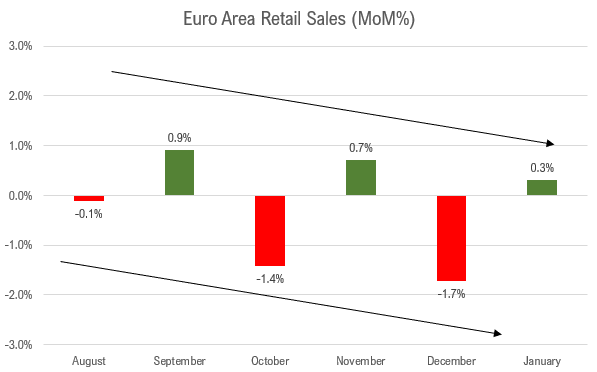

Euro Area Retail Sales

Euro area retail sales grew 0.3% MoM in January but were down -2.3% YoY. Consumers spent at a solid rate to start the year as consumption of food and non-food goods, up 1.8% MoM and 0.8% MoM, was offset by weak spending on fuels, down -1.5% MoM. These figures track the volume of sales, so the decline in energy prices is not related to the decrease in spending here. This month follows a notably weak December where sales were down -1.7% MoM, and food and non-food sales were both down by more than 2%. This favors the monthly trend. The choppiness has been a feature of the data for the last six months as sales have bounced between positive and negative monthly readings since August 2022. However, the gaining months have continued to get weaker as the declining months have gotten sharper. This all adds to a mixed view of the economy in Europe where economic data is making it hard to discern what is going on underneath the hood on a month-to-month basis. The general trend does seem to suggest that there is significant weakness in most sectors of the economy, but incomes are strong, firms are adding jobs, and inflation data keeps surprising to the upside. February sales should bounce back to the downside but will the trend of sharper declines continue? Likely not.

Still to come…

10:00 am (EST) - US Factory Orders

10:00 am - Canada Ivey PMI

12:30 pm - US Investor Movement Index

7:30 pm - Australia Trade

10:30 pm - Reserve Bank of Australia Announcement

Morning Reading List

Other Data Releases Today

The S&P Global Eurozone PMI was 47.6 in February, up from 46.1 in January, the weakest decline since May 2022. Home-building activity was the weakest in the last 7 months. Input cost growth was at the lowest rate in the last 26 months.’

The S&P Global UK Construction PMI jumped 6.2 pts to 54.6 in February, the strongest expansion in 9 months. Input cost growth was the weakest since November 2020. Commercial activity was the strongest at 55.3 while residential activity was still weak at 47.4.

The S&P Global Europe Sector PMI showed that 10 of the 20 monitored sectors register higher activity in February. Tourism & Recreation records strongest output and new order growth. The wider Basic Materials group continues to struggle.

Euro Area Retail Sales

Eurozone retail sales tick up less than expected in January (ING) - A small increase in retail sales in January suggests a weak start to the year for the consumer amid stubbornly high prices. While surveys about the first quarter have been relatively upbeat so far, these sales data don’t give much evidence that a rebound has started. We expect GDP growth in the first quarter to be flat.

China

China's Growth Target for 2023 Set at Around 5% in a measured Government Work Report (Saxo Bank) - China sets a real GDP growth target of "around 5%" for 2023 in the Government Work Report to the National People's Congress. This target is at the lower end of expectations ranging from 5% to 5.5% going into the meeting.

The Chinese economy is on track for stronger growth in 2023 (DWS Group) - The Chinese New Year holiday ended on the 15th February. Initial concerns of an uncontrollable Covid outbreak and medical resources capacity constraints were abated. Instead, there has been a swifter than expected recovery, particularly in the travel industry. Travel and related spending climbed over the Chinese New Year holiday. Total passenger traffic volume by all transportation types returned to 53.5% of the pre-Covid level in 2019 with both railways and airlines reaching close to 90% of pre-Covid level.

China’s Two Sessions sets 5% growth, with a focus on technology and ESG (ING) - China has set a GDP growth target of around 5%, which is lower than market expectations. The main focus of this year will be Environmental, Social and Governance (ESG) and technology self-reliance. This note highlights the important points of the Two Sessions' economic targets for 2023.

US

The services sector expanded in February (TD Bank) - Services continued to expand in February at a basically the same pace as in January, and slightly above the fourth quarter average. The stark contrast to the contraction in the manufacturing index confirms that the rotation of spending away from goods and towards services continues.

Service Sector Expansion Keeps Pressure on Prices, Labor (Wells Fargo) - The key thing to understand from today's ISM services report is that activity is not slowing much and that is keeping pressure on prices and on margins. The fact that this is occurring alongside an upswing in hiring gives the Fed the green light for further rate increases.

U.S. Economy: Still in Service (BMO) - The ISM services PMI barely wavered in February after unexpectedly galloping 6 pts in the prior month—the biggest jump since June 2020. Looking ahead, momentum for the still-strong services sector will depend on labour market conditions. Robust services demand could keep inflation sticky, putting more pressure on the Fed to keep going with rate hikes.

February ISM Non‐Manufacturing Index (First Trust Portfolio) - The major measures of activity were mixed in February. The new orders index increased to 62.6 from 60.4, while the business activity index declined to 56.3 from 60.4. The employment index increased to 54.0 from 50.0, while the supplier deliveries index declined to 47.6 from 50.0.

First Looks Point to February Activity Holding Firm (Wells Fargo) - Data this week did little to alter the picture that, to the extent the underlying trend in the economy is softening, it is not weakening nearly enough to put a quick end to inflation. Manufacturing activity is contracting only gradually, while the service sector continues to expand at a solid clip according to the February ISM releases.

Hard To Achieve A Soft Landing (Northern Trust) - We’re fielding a lot of questions lately asking for a description of how the current cycle might end. Do we hold out hope for a soft landing, with no significant economic damage, or a soft-ish landing, with limited pain? Could we see no landing at all, with activity never slowing and unemployment never rising? These visions feel optimistic after digesting a paper presented at last week’s Chicago Booth Monetary Policy Conference, showing ample precedents for a recessionary hard landing.

Europe

Italian GDP contraction driven by consumption and inventories (ING) - Italian GDP contracted by 0.1% quarter-on-quarter in the final quarter of 2022. We now tentatively anticipate flat growth in 1Q23.

French strikes will cause limited economic impact (ING) - France is currently facing a movement of protests against the pension reform proposed by the government. This Tuesday 7 March marks the 6th day of mobilisations and the unions hope that the movement will strengthen. Although this is an important event from a political and social point of view, the economic impact of the strikes should not be overestimated.

The New Brexit Protocol (Northern Trust) - For some, the process of the U.K.’s departure from the European Union (EU) has been a little like taking some of the eggs out of an omelet. For others, Brexit has simply been a nightmare. However, this week’s developments present a glimmer of hope that the Brexit saga may finally move on from a state of confusion to a path toward conclusion.

Canada

Monkey see, monkey not do (CIBC) - A central banker’s word is their bond, at least if they want to have markets take heed the next time they try to provide guidance on what lies ahead. So having pledged to pause on rate hikes to see how things unfold, Governor Macklem has little choice but to keep Canada’s policy rate unchanged when the Bank of Canada meets in the week ahead.

Nord-Storm (BMO) - And on the ninth meeting, the Bank rested. Following a year-long blast, which saw interest rates hiked in eight consecutive meetings by a cumulative 425 basis points, markets fully expect the Bank of Canada to hold steady at next week’s decision.

Inflation

Underlying inflation (Philip Lane, ECB) - When inflation has been far from target for a sustained period and the process of monetary tightening has been under way for some time, there are three primary inputs into monetary policy decisions. My focus today is on the second input: underlying inflation.

Key Inflation Driver Still Motoring (BMO) - The Fed received more bad news on the inflation front this week with the latest revisions to productivity and unit labour cost data. In the nonfarm business sector, productivity growth was carved in half to 1.7% annualized in Q4, which marked a small improvement from Q3’s trimmed gain of 1.2%.

AI

AI Arrives (Northern Trust) - enerative AI promises to have the same kind of broad economic impact as past technological revolutions. It will raise productivity, and free workers to focus on higher-order tasks. As an analog, optimists point to the automation of factories, whose output is higher than ever even though employment is about the same as it was seventy years ago.

Commodities

China growth and inflation remain key drivers (Saxo Bank) - Commodities started March on a firmer footing after data from China confirmed that activity in the world’s biggest consumer of raw materials is picking up momentum.

Global | Oil in 2023: tight market and prices still high (BBVA) - We will see a very tight market throughout 2023, despite what is likely to be a significant economic slowdown due to various shocks, following the trend seen in recent years.

Fiscal Policy

Fiscal Outlook: The Fire Next Time (BMO) - after this inflation episode is over, we suspect that the next big concern will be the (wounded) state of government finances in many major economies. After being dealt a terrible blow by the pandemic, public finances now face the ugly combination of much higher borrowing costs, prospects of chillier economic growth, and challenging demographic trends.

Demographics

The End of Rapid Population Growth (St Louis Fed) - The era of rapid population growth is coming to an end. The United Nations projects that the world’s population will peak at around 10.5 billion people later this century before beginning to decline.

Research

The Covid-19 Pandemic Spurred Growth in Automation: What Does this Mean for Minority Workers? (Chicago Fed) - The Covid-19 pandemic has accelerated trends in automation as many employers seek to save on labor costs amid widespread illness, increased worker leverage, and market pressures to onshore supply chains. While existing research has explored how automation may displace non-specialized jobs, there is typically less attention paid to how this displacement may interact with preexisting structural issues around racial inequality.

Labor Market Effects of Global Supply Chain Disruptions (San Francisco Fed) - We examine the labor market consequences of recent global supply chain disruptions induced by COVID-19. Specifically, we consider a temporary increase in international trade costs similar to the one observed during the pandemic and analyze its effects on labor market outcomes using a quantitative trade model with downward nominal wage rigidities.

The Productivity Slowdown in Advanced Economies: Common Shocks or Common Trends? (San Francisco Fed) - This paper reviews advanced economy productivity developments in recent decades. We focus primarily on the facts about, and explanations for, the mid-2000s labor-productivity slowdown in large European countries and the United States. Slower total factor productivity growth was the proximate cause of the slowdown.

Subscribe to receive Econ Mornings every weekday at 9 am. More economic and finance content on Twitter, Reddit, and my website.