Euro Area Services Inflation Surges in July

Economic news and commentary for July 31, 2023

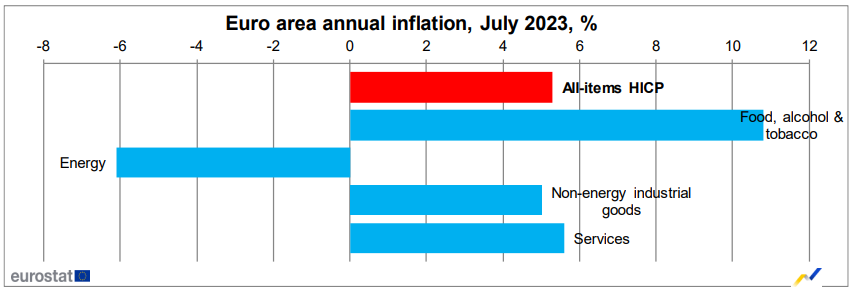

Euro Area Inflation

It’s only been a few days since the ECB made another move against elevated euro area inflation, and we’ve got an update already. Euro area inflation was -0.1% MoM and 5.3% YoY in July, down from 5.5% YoY in June. The slowing of the annual rate continues a string of decelerations since inflation plateaued briefly in April which confirms a general trend of disinflation but a gradual one at best. Once again, food and energy inflation were at odds with each other as the former increased 0.2% MoM and the latter fell -0.3% MoM. However, base effects have been especially favorable to the trend in overall inflation as both categories saw their annual rates decline. Annual food inflation is now at its lowest point since a year ago. Annual energy inflation was negative for the third month in a row and was a low -6.1% YoY in July. It is good that food price growth is slowing and that the energy crisis has mostly abated, but for the most part, these segments aren’t the focus.

Instead, core inflation has become the main point of contention for policymakers and investors. In July, core prices fell -0.1% MoM but the annual rate remained stuck at 5.5% YoY. The movement in goods prices has been less pronounced in recent months, but the latest release revealed a sharp fall in ex-energy goods prices, down -2.7% MoM, leading to a YoY rate of 5.0%. Goods inflation experienced a resurgence at the end of 2022 and the beginning of 2023, so the return to deflation in this category is seen as positive. This new disinflation is likely driven by demand destruction caused by higher interest rates rather than improved supply situations which were the main reasons for goods inflation improving last year.

In stark contrast with goods prices, services prices saw a notable 1.4% MoM increase, resulting in a new cycle high of 5.6% YoY, surpassing both core inflation and goods inflation. It appears that the weakening demand on the goods side is fueling services spending as consumers remain very willing to spend on experiences in the post-pandemic European economy. Additionally, the absence of job losses on an aggregate level in Europe has kept wages high, contributing to increased general costs for businesses. Although the ECB has not committed to a rate hike in the upcoming meeting, its data-driven approach suggests that the sharp rise in services prices in July might influence the ECB's decision. If no other data contradict this development, it could lead to another interest rate hike in September.

Still to come…

9:45 am (EST) - US Chicago PMI

10:30 am - US Dallas Fed Manufacturing Survey

7:30 pm - Japan Unemployment Rate

Morning Reading List

Other Data Releases Today

Italy's GDP fell -0.3% QoQ in Q2 2023 after a strong 0.6% QoQ increase in Q1 2023. YoY growth is down to 0.6% YoY (2.0% YoY prev). The main negative contribution came from domestic demand in inventories.

Euro area GDP grew 0.3% QoQ in Q2 2023 after no growth in Q1 2023. The YoY GDP growth rate has fallen to 0.6% YoY, down from 2.4% YoY a year ago in Q2 2022.

Italy's CPI grew 0.1% MoM and 6.0% YoY in July, down from 6.4% YoY in June.

Core CPI: 5.2% YoY (0.3% MoM)

Food: 10.7% YoY (0.2% MoM)

Energy: 0.7% YoY (-1.4% MoM)

Goods: 7.1% YoY (-0.1% MoM)

Services: 4.1% YoY (0.3% MoM)

German import prices fell -1.6% MoM and -11.4% YoY in June which is the largest YoY decline since September 2009. The prices of intermediate goods were down a sharp -8.8% YoY. Consumer goods import prices were still up 2.7% YoY.

Euro Area Inflation

Eurozone inflation dropped to 5.3% in July as all eyes turn to services (ING) - Services inflation remains the main concern for the European Central Bank as inflation moves slowly in the right direction. While base effects muddy the picture, inflation should be materially lower towards the end of the year.

US Personal Income & Spending

Consumer Spending Grows, Even as Prices Remain Elevated in June (TD Bank) - Personal income grew 0.3% month-on-month (m/m) in June, which was below market expectations for 0.5% growth. This marked a deceleration from the prior month's gain of 0.5%. Gains were led by compensation to employees, which also rose by 0.5% for the third consecutive month.

U.S. Personal Spending: The Real Deal (BMO) - A data-dependent Fed will see mixed results in today's reports. Inflation and labour compensation are moderating, but consumers (and the economy) appear to be picking up steam. Many more reports will be in hand before the September 19-20 policy meeting rolls around; but, for now, we lean toward no further rate hikes, assuming inflation and wage growth continue to calm down.

Personal Income Rose 0.3% in June (First Trust Portfolios) - Income and spending closed out the first half of 2023 on a healthy note, but consumer strength is also keeping the Fed on guard. The best news in today’s report was that incomes rose 0.3% in June and are up 5.3% in the last year, led by gains in private-sector wages & salaries (+0.6% for the month and up 5.9% year-to-year). Consumer spending outpaced incomes in June, with a pickup in spending across all major categories.

Personal Income Rises 0.3% in June (NAHB) - The most recent data release from the Bureau of Economic Analysis (BEA) showed that personal income increased 0.3% in June. The pace of personal income growth slowed after reaching a 0.7% monthly gain in January 2023. Gains in personal income are largely driven by increases in wages and salaries.

Warmer consumer spending and cooler inflation (EY Parthenon) - US consumers appeared to be in a spending mood heading into the summer amid slower but resilient labor market gains and cooler inflation trends. Real personal outlays rose more than expected in June, up 0.4% month over month (m/m) with spending rising strongly across consumer goods categories, including autos (+2.2%) and recreational goods (+1.8%).

Consumers Keep on Spending in June (Wells Fargo) - The 0.4% rise in real spending sets personal consumption to start Q3 on a solid note. A jump in durables despite shifting spending patterns highlights household's resiliency. Inflation is moving in the direction that will be liked by the Fed.

Bank of Japan Announcement

Bank of Japan Adopts Flexible Approach to Yield Curve Control with Implications for the Japanese Yen (Saxo Bank) - The Bank of Japan (BoJ) maintained its yield curve control (YCC) target for 10-year Japanese Government Bonds with a range of plus and minus 50 basis points around zero at the July monetary policy meeting. However, it introduced a more flexible approach, allowing deviations from the target range and setting a 1% cap on the maximum rise in the 10-year JGB yield.

BOJ Moves Toward Phasing Out Yield Curve Control (PIMCO) - July’s monetary policy meeting could well be remembered as the moment the Bank of Japan (BOJ) began phasing out its seven-year-old yield curve control (YCC) program, or at least took a major step toward an eventual exit. In our view, the changes in YCC could help the program phase out gradually as the conditions that prompted its creation (persistent low inflation and low growth) also diminish, without prompting a disruptive rise in yields. We also do not expect a significant adverse impact on global financial markets from the YCC changes.

Bank of Japan Delivers Another Hawkish Policy Tweak (Wells Fargo) - The Bank of Japan (BoJ) sprung a surprise at today's monetary policy announcement, delivering another hawkish tweak to its Yield Curve Control policy. While the BoJ did not change its main policy parameters, it said it would conduct yield curve control with greater flexibility, regarding the upper and lower bounds of the range as references, not as rigid limits, in its market operations.

US Employment Cost Index

Wage inflation is (slowly) easing (EY Parthenon) - The latest Employment Cost Index (ECI) data points to pesky wage growth persistence well above the Fed’s comfort zone. It should favor another 25 basis points Fed rate hike next week, but the two-day Federal Open Market Committee meeting will likely feature intense discussions around the perceived robustness of the economy and stickiness of inflation with doves and hawks benefiting from plenty of data to support their respective views.

Labor Cost Growth Is Gradually Slowing (Wells Fargo) - The Employment Cost Index (ECI) increased 1.0% quarter-over-quarter in Q2, the smallest increase in two years. The Fed's preferred measure of labor cost growth is still running faster than it was before the pandemic and above what would be consistent with 2% inflation over the medium term. That said, compensation growth appears to have turned a corner as supply and demand in the labor market have come into better balance.

US

Ground Control to Major Powell: Odds of Soft Landing Rising (Wells Fargo) - Economic data continued to beat expectations this week. Real GDP came in at a stronger-than-expected 2.4% annualized rate in Q2. Inflation and compensation costs have decelerated; yet, we suspect the FOMC would like to see continued moderation before it concludes that inflation is sufficiently low and stable.

Soft Landing: Are We There Yet? (Northern Trust) - The journey has been anything but smooth. Equity markets offered little reason for cheer throughout 2022. A rolling recession has imperiled several sectors that have since returned to growth. Crises surrounding gilt markets, cryptocurrency and the banking industry all had the potential to spark a broad downturn, but one has not emerged.

U.S. Economy: Resilience 4, Recession 0 (BMO) - We’ve been wavering for a while on whether to shift to the soft-landing camp long staked out by Chair Powell and, now, apparently by his staff. Not anymore. Rarely is one economic report the straw that breaks the camel’s back in one’s thinking. But the broad strength shown in the Q2 GDP release has convinced us that the economy is more durable than we thought.

Macroeconomic impulses ripple through the advanced manufacturing and mobility sectors with implications for sector business leaders (EY Parthenon) - General labor market resilience, moderating inflation and gently slowing final demand growth offer hope of an economic soft landing. With headline inflation cooling rapidly, real wage growth is turning positive, providing a tailwind to consumer spending. Simultaneously, the need to address supply shortages across the economy has supported robust construction activity, prevented a severe manufacturing pullback, and helped price and wage pressures ease.

Fed raises rates but refuses to guide on next move (ABN AMRO) - The FOMC raised rates by 25bp, as widely expected, taking the target range for the fed funds rate to a new 22-year high of 5.25-5.50%. The only notable change to the accompanying statement was a small upgrade to the assessment of the economy, which is now judged to be growing ‘moderately’ rather than ‘modestly’, reflecting the recent resilience in US economic data.

US economy defies gravity (ABN AMRO) - Economy continues to defy gravity – Q2 GDP surprised to the upside, with activity expanding 2.4%, above our and consensus expectations (1.9% and 1.8% respectively). As we expected, the strength was driven by both resilient consumption (+1.6% q/q saar) and a rebound in fixed business investment (+7.7%), with the upside surprise driven by somewhat stronger consumption and a bigger fall in imports than we had pencilled in.

Europe

The U.K. Is In A Rough Patch (Northern Trust) - Britain is enduring the same post-pandemic economic afflictions that other countries are, but their manifestation in the U.K. has been more severe. Real gross domestic product is still below its 2019 level, long after other developed countries pushed through that threshold. U.K. inflation reached a much higher peak than it did elsewhere, and remains elevated in spite of aggressive interest rate increases from the Bank of England.

Eurozone economy returns to positive growth but underlying weakness remains (ING) - GDP growth beat expectations at 0.3% quarter-on-quarter in 2Q, but underlying weakness remains significant. For the data-dependent European Central Bank, this GDP reading will not be a dovish argument at the September meeting, leaving a further hike on the table.

Europe | ECB raises rates but changes phase (BBVA) - There were no surprises at Thursday's European Central Bank (ECB) meeting, nor at Wednesday's US Federal Reserve (Fed) meeting. In both cases, it was decided to raise reference interest rates, the ECB to 4.25% (the refi rate) and the Fed to 5.50%.

Swedish Q2 flash GDP: Ouch (Nordea) - GDP for Q2 declined by 1.5% on the quarter, which was much weaker than the Riksbank’s expectations.

ECB opens door to September pause (ABN AMRO) - The ECB raised its policy rates by 25bp as was widely expected, which took the deposit facility rate to 3.75%. In the press conference, President Christine Lagarde sounded much less sure about further rate hikes, saying that both a pause and an additional hike were possibilities in September. Our base line is that July marked the peak in policy rates and that we will see a pivot around the turn of the year as we expect growth and inflation to come in significantly lower than the ECB projects.

China

China: PMI’s show non-manufacturing growth slowing further (ING) - The decline in manufacturing eased slightly in July, but the non-manufacturing sector showed a larger-than-expected slowdown in growth and further falls could see it skirting with contraction.

China holiday wrap-up - part 2: Stimulus and private sector plan lift Chinese markets (Danske Bank) - This weeks' stimulus signals from China's Politburo were stronger than expected and lifted Chinese markets. It follows a 31-point plan to support the private sector released last week. China has also taken more steps to show support of big tech.

Emerging Markets

Emerging Markets Mostly Hanging Tough (BMO) - Broadly, the major EMs are displaying a strong degree of resilience just like their developed-market peers. Coupled with elevated commodity prices, we think that the decision by a number of central banks, particularly in the Latam region, to tighten monetary policy early on to tackle inflation was critical in cushioning the fallout from sharply higher U.S. interest rates over the past year.

India’s food supply chain intervention (S&P Global) - The Indian government has banned exports of non-basmati rice grades to tackle domestic food price inflation. India accounted for 32% of all rice exports in 2022 compared with 24% in 2013 as the government sought to boost export supplies.

Monetary Policy

Some hard truths about soft landings (CIBC) - We at CIBC Economics have never joined the herd calling for outright recessions in the US and Canada as a necessary evil to return to a 2% inflation target. With inflation having been chopped in half without an economic slump, we’re now in good company, not just among private sector forecasts, but importantly including the central banks that are no longer aiming for a recession, but gaining confidence that a soft landing could do the job.

How Much Progress Has the Fed Made? (BMO) - Progress is progress, and the Fed’s aggressive tightening cycle appears to be paying dividends in calming inflation pressures. The relative headway compared with past cycles suggests the latest rate hike could be the last, and that a soft landing might be more than a Powell pipe dream.

The Winds of Change Are Blowing (BMO) - Lots of twists and turns this week, from a couple of central banks. The biggest brow-raiser would be from the ECB, which swung from June’s hawkish 25 bp hike to a less-hawkish/more dovish 25 bp hike in July. President Lagarde was clearly prepared for the hundreds of ways reporters tried to squeeze out some forward guidance from her.

Real Estate

Housing Affordability Expectations Slide Back, Again (NAHB) - After a reprieve in the first quarter of 2023, buyers’ outlook for housing affordability turned bleaker again in the second quarter. According to the latest Housing Trends Report, 76% of buyers are able to afford less than half the homes for-sale in their markets, up from 73% in the first quarter of 2023. On the flip side, the share able to afford most homes available fell from 27% to 24%. The shift provides evidence that recent upticks in home prices and mortgage rates are filtering directly into home buyers’ affordability expectations.

We’re All Data-Dependents Now (BMO) - The one common theme to this week’s slew of central bank pronouncements is that policymakers are keeping the door open to further tightening moves, depending on how the inflation and economic data unfold in the coming months. While central bankers may not all be using the buzzwords “data dependent”, that’s how the entire financial community now views them.

Commodities

Commodity markets calm as traders await Fed’s next move (S&P Global) - The Material Price Index (MPI) by S&P Global Market Intelligence was flat last week, following on from two consecutive weekly increases. Despite the lack of movement in the overall MPI at a headline level, there were small declines recorded in eight out of the ten subcomponents. And the story of this year has been declining prices with the index 28% lower than its year-ago level.

Markets

The Waiting Is Now the Hardest Part (BMO) - Equity markets rallied this week on signs that the economy is holding firm despite ongoing rate hikes, while inflation continues to ebb. The S&P 500 gained 1.0%, with telecom services charging ahead almost 7%. Defensives and rate-sensitives lagged the pack. While the Fed raised rates as expected, the BoJ's tweak to yield curve control lifted bond yields, while the ECB also raised rates.

Research

What determines passthrough of policy rates to deposit rates in the euro area? (Federal Reserve) - Interest rates on bank deposits are sticky and move only sluggishly following changes in central bank policy rates. As deposits are typically the largest share of bank liabilities, deposit rate stickiness plays a key role for bank funding costs and profitability. This note examines passthrough from European Central Bank (ECB) policy rates to bank deposit rates across euro-area banking sectors.

Are Signs of Labor Market Normalization Reflected in Wage Growth? (Richmond Fed) - There have been two salient features of the U.S. economy in the past two years: a tight labor market and high inflation. In the Richmond Fed business surveys, the tight labor market has manifested in a high employment index combined with a low availability of skills index; high inflation has corresponded with extreme elevation in our survey's measures of growth in prices paid and prices received.

The Persistent Urban Shortfall in Leisure and Hospitality Employment (Federal Reserve) - As a high-contact service sector with limited capacity for remote work, the US leisure and hospitality sector—which includes restaurants, bars, hotels, museums, and movie theaters—was hit particularly hard by the COVID-19 pandemic. In the first two months of the pandemic, leisure and hospitality lost over 8 million jobs, nearly half its employment. In those same two months, the rest of the private sector lost about 13 million jobs—such that leisure and hospitality accounted for almost 40 percent of private-sector job losses, despite comprising just 13 percent of pre-pandemic private employment.

Empirical assessment of SR/CA small-dollar lending letter impact (Federal Reserve) - Guidance is used by bank regulators to communicate supervisory expectations to both examiners and banks. In March 2020, in response to pandemic shut-downs, financial regulators issued a joint statement encouraging small-dollar lending to meet temporary cash-flow imbalances, unexpected expenses, or income short-falls. The letter further highlighted that offering short-term, unsecured credit products to creditworthy borrowers would be considered favorably for Community Reinvestment Act (CRA) purposes. A follow-up letter was issued on May 20th elucidating lending principles for responsible small-dollar loans.

How Are Financial Conditions Tracked? (St Louis Fed) - How are financial conditions tracked? And are they tighter today than they were in early 2022 when the Federal Reserve began raising the federal funds rate? How about compared with the average over the past 10 years—and the past 20 years?

Looking for a way to take advantage of higher interest rates? I recommend SoFi’s high-yield savings account which has a yield of 4.4% (subject to change) and includes FDIC deposit insurance for both its checking and savings accounts just like a traditional bank. Use my referral link to get a sign-up bonus and start earning that rate today. (This is also a great way to support me since I get a bonus too!)

Subscribe to receive Econ Mornings every weekday at 9 am. More economic and finance content on Twitter, Reddit, and my website. You can also see my feed on the PiQSuite platform as a partnered feed.