German Business Climate Hits Lowest Level in Months

Economic news and commentary for June 26, 2023

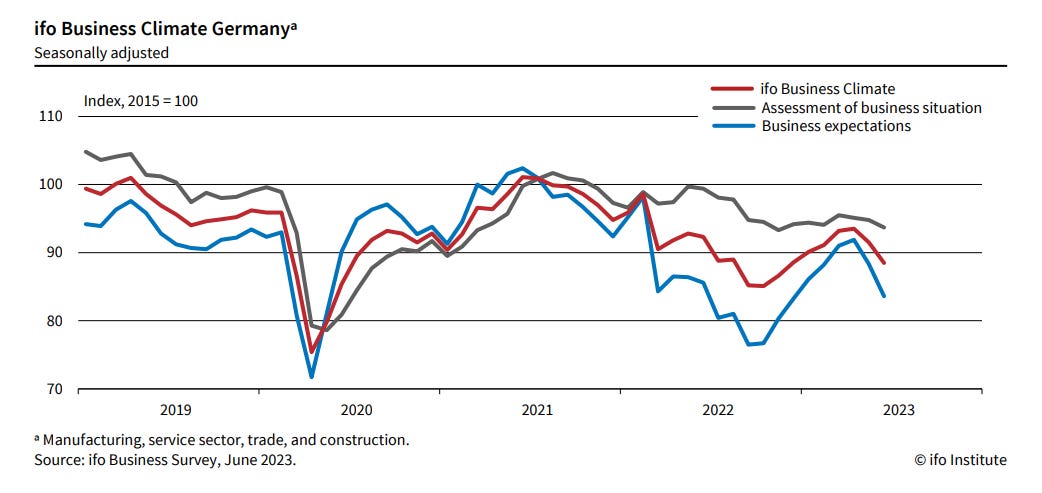

Germany Ifo Index

The ifo Business Climate Germany index, which measures the sentiment of German businesses, experienced a notable decline in June, dropping from 91.5 in May to 88.5. This marks the lowest level since December 2022 and raises concerns about the state of the German economy. The decline in the index was driven by deteriorating assessments of both current situations and future expectations. The Current Situation index fell by -1.1 points to 93.7, indicating that companies' evaluations of their present conditions worsened. Similarly, the Future Expectations index plummeted by -4.7 points to 83.6, highlighting significantly pessimistic outlooks for the coming months.

One of the primary causes of concern is the weakening manufacturing sector, which is having a profound impact on the German economy. The business climate in manufacturing experienced a substantial deterioration, with expectations reaching their lowest level since November 2022. The service sector, which had been performing relatively well, also saw a significant drop in the index. In June, it fell by -4.1 points to 2.7. However, this level is still higher than the lows witnessed earlier this year in January and February.

The recent results of the ifo survey align with the findings of the Purchasing Managers' Index (PMI) surveys released last week, further emphasizing the economic challenges faced by Germany. These developments serve as additional evidence that German GDP, as well as the broader Euro area GDP, may contract in the second quarter of the year.

Still to come…

10:30 am (EST) - US Dallas Fed Manufacturing Survey

Morning Reading List

Other Data Releases Today

The CBI Distributive Trades Survey retail sales volume index remained low at -9% in June, up from -10% in May. Suppliers' orders were still weak (-10%) but improved substantially from last month (-30%).'

German Ifo

German Ifo index plunges in June (ING) - The Ifo index has dropped or more accurately, collapsed, for the second month in a row, suggesting that the rebound of the German economy has ended before it ever really began

US

Fed’s Progress Warrants Patience (BMO) - Still, there’s reason to believe the Fed is nearing the end of the tightening cycle. As the Chair said, “We’re at least close to where we think our destination is… and it only makes common sense to move… at a careful pace”. Given the relative progress to date in slowing the economy, employment and inflation, a little patience would be a virtue in reducing the risk of a hard landing.

Economic Resilience Suggests the Fed Has More Work to Do (Wells Fargo) - Chair Powell noted this week in Congressional testimony that economic activity has been resilient in the face of higher interest rates, suggesting there is more work to be done by policymakers in order to achieve their 2% inflation target. Housing was the dominant theme this week and intimated the housing market is holding up reasonably well in the face of higher interest rates and the potential for recession early next year.

Fed confirms more hikes are coming (Nordea) - Powell repeated the FOMCs hawkish stance before congress while both the BOE and Norges Bank hiked rates by 50bps this week.

Europe

BoE surprises with 50bp hike; more to come (ABN AMRO) - The Bank of England surprised markets yesterday by raising its policy rate by 50bp. We expect further rate hikes given the re-acceleration in core inflation in the UK, but the pace and magnitude of further rate moves is highly uncertain and hinges on incoming data flow.

Europe’s Inflation Outlook Depends on How Corporate Profits Absorb Wage Gains (IMF) - Rising corporate profits account for almost half the increase in Europe’s inflation over the past two years as companies increased prices by more than spiking costs of imported energy. Now that workers are pushing for pay rises to recoup lost purchasing power, companies may have to accept a smaller profit share if inflation is to remain on track to reach the European Central Bank’s 2-percent target in 2025, as projected in our most recent World Economic Outlook

Spain | Why are house prices not receding? (BBVA) - In recent months, the country’s real estate market has not been performing as one might expect, in the sense that house prices are not receding as sales decline.

Asia

APAC tourism surges in first half of 2023 (S&P Global) - There have been significant headwinds to Asia-Pacific (APAC) merchandise exports during the first half of 2023 due to weak growth in key export markets. However, the strong rebound in international tourism inflows evident in the first half of 2023 signals that the rebound in the tourism economy in 2023 will help to mitigate the negative impact of weak merchandise exports for a number of APAC economies.

Canada

Canadian Economy Remains Resilient (BMO) - Resilience was the theme this week, and something BoC policymakers keyed on to drive the June 7 decision to hike rates. We get another set of top-tier data next week, none of which are expected to change the outlook for another 25 bp hike at the next policy meeting on July 12.

Provinces: We’re All in This Together (BMO) - The Canadian economy has held up well through the first two quarters of the year, though momentum looks to fade with a mild downturn in the cards for later in the year. Real GDP growth is expected to average 1.3% this year before slowing to 1.0% in 2024, and the regional outlook is very balanced by historical standards.

Inflation

The Elusive Finish Line (BMO) - While inflation remains above target in many countries, the finish line looks even further away for some. That means policymakers have to be nimble in responding to data and be open to the prospect of faster tightening.

PMI

UK Flash PMI surveys signal growth slowdown in June as rate hikes take their toll (S&P Global) - June's flash PMI survey data rounded off a solid quarter of growth for the UK economy, though the pace of expansion slowed amid signs of a growing toll from the rising cost of living and higher interest rates. Most notably, consumer spending on services, a core growth driver earlier in the year, is now showing signs of faltering.

Eurozone flash PMI shows inflation pressures cooling in June as economic upturn fades (S&P Global) - Eurozone business output growth came close to stalling in June, according to the latest HCOB flash PMI survey data produced by S&P Global, pointing to renewed weakness in the economy after the brief growth revival recorded in the spring.

Flash PMI data for June signal cooler global price trends amid mounting growth risks (S&P Global) - June's flash PMI surveys rounded off a solid second quarter, with all four largest developed world economies having continued to grow in June. However, the recent growth surge seen in the spring has lost momentum, and almost petered out in the eurozone, as a deepening manufacturing downturn has been accompanied by slower growth in service sector activity. The latter had been buoyed by resurgent post-pandemic spending in the spring, but this impact now appears to be waning as the reality of higher interest rates and the rising cost of living dominates.

Trade

Critical relationship: Supply chain implications of US-UK Atlantic Declaration (S&P Global) - The "Atlantic Declaration" between the US and UK includes provisions to negotiate a Critical Minerals Agreement. If ratified, it could give UK exporters of cobalt, graphite, lithium, manganese and nickel eligibility under the US Inflation Reduction Act (IRA) funding for electric vehicle components.

FX

FX Update: Euro down on PMI miss. USD resurgent (Saxo Bank) - The US dollar is resurgent as risk sentiment went on tilt in Asia and the Europe offered up woeful flash June PMI’s, taking EURUSD well south of 1.0900 again and challenging a reversal of the recent attempt to rebuild an up-trend. Elsewhere, NOK and GBP failed to sustain rallies in the wake of larger-than-consensus 50-bp hikes from Norges Bank and Bank of England yesterday with NOK even poking at new local lows on the weakening of energy prices and the weak Eurozone numbers.

"The International Role of the U.S. Dollar" Post-COVID Edition (Federal Reserve) - For most of the last century, the preeminent role of the U.S. dollar in the global economy has been supported by the size and strength of the U.S. economy, its stability and openness to trade and capital flows, and strong property rights and the rule of law. As a result, the depth and liquidity of U.S. financial markets is unmatched, and there is a large supply of extremely safe dollar-denominated assets.

2nd Annual International Roles of the U.S. Dollar Conference (Federal Reserve) - The U.S. dollar plays a central role in the global economy. In addition to being the most widely used currency in foreign exchange transactions, it represents the largest share in official reserves, international debt securities and loans, cross-border payments, and trade invoicing. The ubiquity of the U.S. dollar in global transactions reflects several key factors, including the depth and liquidity of U.S. capital markets, the size of the U.S. economy, the relatively low cost of converting dollars into other currencies, and an enduring confidence in the U.S. legal system and its institutions.

Outlook

With the global economy growing at a moderate pace, inflation will gradually subside (S&P Global) - Global economic performance exceeded expectations in early 2023. Led by post-pandemic surges in mainland China and India, world real GDP grew an annual rate of 3.2% quarter over quarter in the first quarter of 2023, double the pace of the previous quarter. This increase was achieved despite stagnation in Western Europe and fragile 1.3% growth in the United States. S&P Global Purchasing Managers' Index™ (PMI) surveys through May highlight a dichotomy between resilient services and struggling manufacturing sectors, reflected in output, new business and prices.

Week Ahead Economic Preview: Week of 26 June 2023 (S&P Global) - A series of inflation readings will be highlights in the final week of June as markets grapple with the likelihood of further interest rate hikes. Specifically, US core PCE will be due, in addition to Canada and eurozone CPI. US consumer spending will also shed light on the expected inflation path while UK GDP and industrial production figures from various APAC economies will help assess recession risks.

Research

Addressing Traditional Credit Scores as a Barrier to Accessing Affordable Credit (Kansas City Fed) - Affordable credit enables consumers to better manage their finances, cope with unexpected emergencies, and pursue opportunities such as entrepreneurship or higher education. However, many consumers face difficulties obtaining the credit they need. A major impediment is lenders’ reliance on traditional credit scores to assess consumers’ creditworthiness. These credit scores affect not only loan approval decisions but also the interest rates consumers pay on their loans. While credit scores are intended to help lenders make informed decisions about consumers’ risk of default, they do not always accurately reflect a borrower’s ability to repay. Traditional credit scores may also disproportionately punish consumers from economically disadvantaged groups.

Accumulated Savings During the Pandemic: An International Comparison with Historical Perspective (Federal Reserve) - The COVID-19 pandemic gave rise to unprecedented global economic conditions. Due to a mix of government-imposed restrictions and voluntary personal decisions, mobility levels collapsed in March 2020 and subsequently closely tracked the successive waves of the pandemic. To mitigate the health and economic fallout from the COVID-19 pandemic, governments around the world engaged in large fiscal support programs which increased the demand for consumption goods, but production of these goods did not adjust quickly enough to meet the sharp increase in demand. This imbalance between supply and demand across countries contributed to the ongoing inflation outburst (see de Soyres, Santacreu and Young, 2023).

Distressed Firms and the Large Effects of Monetary Policy Tightenings (Federal Reserve) - The stance of U.S. monetary policy has tightened significantly starting in March 2022. At the same time, the share of nonfinancial firms in financial distress has reached a level that is higher than during most previous tightening episodes since the 1970s (Figure 1). What are the consequences of a high share of distressed firms—i.e., firms close to default—for the transmission of monetary policy?

Subscribe to receive Econ Mornings every weekday at 9 am. More economic and finance content on Twitter, Reddit, and my website.