Hot Services Inflation Sets Up the ECB for a Hawkish Announcement

Economic news and commentary for May 2, 2023

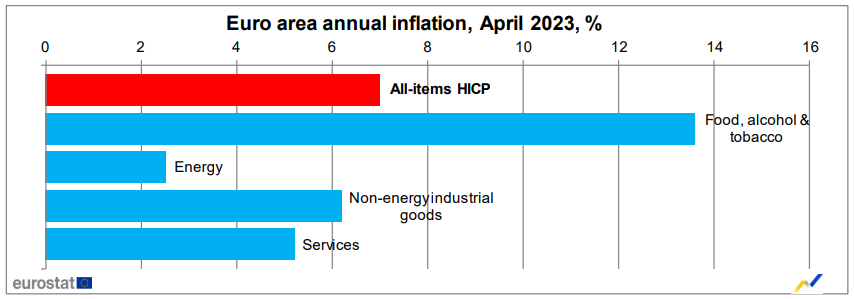

Euro Area Inflation

If this inflation report was to provide some color to the ECB meeting this week, then that color is red. Euro area inflation was 0.7% MoM and 7.0% YoY in April, up from 6.9% YoY in March. The acceleration in the pace of annual inflation came even on the backs of an apparent peak in food inflation and another monthly decline in energy prices. The index for food prices grew just 0.2% MoM on the month which lead to a -1.9 ppts decline in the annual pace of price increases to 13.6% YoY. This is the lowest since November 2022. A further deceleration in food inflation could be observed if monthly gains stay muted as base effects start to have a major impact on the year-over-year comparison going forward. Energy prices declined -0.8% MoM which is a positive for sure, but some base effects led the annual pace to turn positive at 2.5% YoY after a brief period in negative territory at -0.9% YoY in March. This segment may continue to be volatile as energy markets in Europe settle on a consistent trend.

The worrying trends came out of the core parts of inflation which are the ones that the ECB will be focused on in its meeting. As headline inflation has seen a consistent downtrend over the last few months, core inflation has been more resistant to downward pressure. In April, core inflation grew 1.0% MoM and 5.6% YoY which is only a slight decline from the 5.7% YoY pace recorded in March. The strong monthly pace means that core inflation is neutralizing base effects and keeping the annual rate of inflation near peaks. Non-energy goods prices saw a moderate pace of growth in April, up 0.7% MoM, which means that there was a small improvement in the annual pace, down -0.4 ppts to 6.2% YoY. This reading means that goods inflation has been above 6% for six months now which is troubling considering other developed countries like the US and Canada have seen clear downtrends in their goods inflation readings. It seems that supply chain disfiguration that is lingering from the Russia-Ukraine conflict remains the most impactful to the neighbors of the conflict.

While the dynamics of goods inflation are discouraging, services inflation is the real area of focus for the ECB because it has advanced again. Services prices were up a strong 1.2% MoM, pushing the annual pace to a new high of 5.2% YoY. The pressures from high wages and possibly from the lasting tenacity of demand from reopening effects. The former factor seems more likely the major driver of persistent services inflation. Employment trends in the euro area do not point to any major depressurization in wage growth as unemployment remains near all-time lows. Measures of wages in the euro area are only released on a quarterly basis, so it’s hard to be clued into where that is trending in non-quarter-ending months. The latest data point we got was for nominal labor costs in Q4 2022. In that report, labor costs growth had risen to a new high of 5.7% YoY with services labor costs up 6.2% YoY. It is hard to see how that has come down in Q1 2023.

While services inflation and wage growth dynamics play against the ECB, it does have some relief in the current trends in credit conditions. Today, its report on monetary policy found that the expansion of the euro area money supply is slowing. In fact, the narrow reading of money supply, the M1 monetary aggregate, was down -4.2% YoY in March (-2.7% YoY in February). The report also showed that lending to households and non-financial corporations was slowing which confirms the findings in the Q1 2023 bank lending report. In that report, the ECB notes that a net 27% of banks tightened lending standards in Q1 2023 which is the sharpest tightening since the 2011 debt crisis. ECB members will seek to balance inflammatory services inflation with the cooling of credit conditions. However, the former priority will likely take precedence in the meeting this week since the inflation number will be on everyone’s mind. The ECB will have to move by at least 25 bps (the likely option) and will likely prepare for another rate hike in the next meeting. Additionally, it will keep hawkish language in its communications to assure that markets understand its commitment to reducing inflation.

S&P Manufacturing PMIs

Russia: 52.6 (Mar 53.2)

Spain: 49.0 (Mar 51.3)

UK: 47.8 (Mar 47.9)

Italy: 46.8 (Mar 51.1)

Poland: 46.6 (Mar 48.3)

France: 45.6 (Mar 47.3)

Netherlands: 44.9 (Mar 46.4)

Germany: 44.5 (Mar 44.7)

Czech Republic: 42.8 (Mar 44.3)

Manufacturing PMIs came out a day late for Europe due to a bank holiday starting the week. The many reports indicate that the manufacturing contraction in Europe is not over, and a substantial rebound is likely not happening anytime soon. The effects of higher interest rates were very apparent in the April PMIs as most reported that demand contracted and the momentum of inflation started to pull back. The two nations that saw manufacturing expansions in March, Italy and Spain, both turned to contractions. All other countries saw their rates of contraction worsen. The Eurozone Manufacturing PMI summarizes it well. The April reading of 45.8, down from 47.3 in March, was a 35-month low. Output deteriorated to start the second quarter after it had increased for the last two months. New orders declined for the 12th month in a row, and in April, the rate of decline was the sharpest in four months. Weak conditions led to the positive trend of shrinking costs. Manufacturers in the eurozone saw input costs fall for the second month in a row, and the drop in operating expenses was the fastest in around three years. The weak April PMIs set up Europe for a weak Q2 2023 which could be the start of the rate-induced recession. This is especially likely since further ECB rate hikes are likely on the way as it continued to combat elevated inflation.

Still to come…

10:00 am (EST) - US Factory Orders

10:00 am - US JOLTS

9:30 pm - Australia Retail Sales

Morning Reading List

Other Data Releases Today

The Reserve Bank of Australia increased its cash rate by 25 bps to 3.85% in its May meeting after pausing in April. The RBA asserts that inflation is "passed its peak," however, it is not slowing enough. The RBA also comments that “some further tightening may be required.”

The UK Nationwide House Price Index grew 0.5% MoM and was down -2.7% YoY in April with an average price of £260,441. The 0.5% increase ends a streak of 7 consecutive monthly declines as mortgage rates fall from their peaks.

German retail sales (nominal) fell -1.3% MoM and -0.2% YoY in March. Real sales were down -2.4% MoM and -8.6% YoY.

The S&P Global Eurozone Manufacturing PMI dropped to a 35-month low of 45.8 in April, down from 47.3 in March. Output turned to contracting after two months of expansion. Weak conditions lead to the sharpest decline in operating costs in almost 3 years.

The growth of the M1 money supply in the euro area was -4.2% YoY in March, down from -2.7% YoY in February. Loans to households increased 2.9% YoY (down from 3.2% YoY), and loans to non-financial corporations increased 5.2% YoY (down from 5.7% YoY).

The ECB reports that a net 27% of banks tightened lending standards in Q1 2023.

This is the highest level since the euro area sovereign debt crisis in 2011.

Italy's CPI grew 0.5% MoM and 8.3% YoY in April, up from 7.6% YoY in March.

Core CPI: 6.3% YoY (0.7% MoM)

Food: 12.3% YoY (0.7% MoM)

Energy: -16.7% YoY (-0.8% MoM)

Non-Energy Goods: 5.4% YoY (0.3% MoM)

Services: 4.7% YoY (0.8% MoM)

Italy's PPI fell -1.5% MoM and was up 3.8% YoY in April Excluding energy, PPI was only down -0.1% MoM and was up 6.2% YoY. Producer prices for consumer goods were up 0.2% MoM and 8.9% YoY on strong non-durable price gains.

RBA Announcement

Australia: Reserve Bank surprises with 25bp hike (ING) - Despite falling inflation, Reserve Bank of Australia (RBA) Governor Philip Lowe justified the latest hike by saying it would take time to bring inflation down and hinted that more hikes might be necessary.

Euro Area Inflation

Eurozone inflation surprisingly increased in April (ING) - Headline inflation was slightly up while core inflation was slightly down. This makes April inflation in the eurozone sticky and underlines the need for further rate hikes, albeit at a slower pace and smaller magnitude than before.

Italian headline inflation bounces in April on base effects (ING) - The road to headline disinflation is proving a winding one, and the profile is affected by the timing of past administrative decisions. Stable core inflation is comforting, but we will likely need more time for a clear decline.

US Manufacturing PMI

Manufacturing Sector Downturn Continued in April According to ISM (TD Bank) - The ISM Manufacturing Index gained a sliver of ground in April, up to 47.1 from 46.3 in March. That is slightly better than market expectations, but marks six months of contractionary readings for the factory sector.

U.S. ISM Manufacturing PMI ... Up and Yet, Still Down (BMO) - Looks like a number of the regional surveys had the right idea: despite some big declines in their diffusion indexes (example: Motown Philly), their ISM-adjusted series all rose and that is what happened with the national figure.

The ISM Manufacturing Index Increased to 47.1 in April (First Trust Portfolios) - Today’s report on the US factory sector was moderately good news, with the ISM Manufacturing Index posting a rebound from the lowest reading since the early months of COVID. That said, the overall index remains in contraction territory and only five of eighteen industries reported growth in April.

Amid Smolders of Contracting ISM, Some Coals of Inflation Still Burn (Wells Fargo) - Today's ISM report for April illustrates the difficulty in getting inflation fully in check. Despite a headline that remains underwater, prices paid and employment are both in expansion territory.

US

Shedding Light on U.S. Office CRE Risks (TD Bank) - Office CRE fundamentals remain sluggish – a narrative highlighted by the fact that the sector’s vacancy rate recently eclipsed its Global Financial Crisis peak and rose to a new all-time high. The persistence of remote and hybrid work arrangements, an expected deceleration in U.S. economic growth, and the fact that more office inventory is slated to hit the market this year, suggest that there’s no relief on the horizon.

The last Fed hike? (ABN AMRO) - The Fed is expected to hike rates one last time on Wednesday, but we could be in for some further rate rises if the economy doesn't cool more quickly.

All Eyes on the Fed (First Trust Portfolio) - For nine of the last fifteen years, few people thought about the Fed. Sure, we discussed QT and QE, but the Federal

Reserve held interest rates at zero year after year. In 2017 and 2018, they lifted rates and it was all anyone talked about. Then they cut them to zero and the noise went away. Now, with rates headed up, all eyes are again on the Fed, and investors are parsing every word of its statements and the Powell press conferences.

FOMC meeting PREVIEW, May 2-3 (EY Parthenon) - We anticipate the Fed will proceed with a 25 basis points rate hike at the upcoming May 2-3 Federal Open Market Committee (FOMC) meeting, bringing the federal funds rate range to 5.00% to 5.25%. Given the current market fluidity and numerous possible interpretations of economic data, policymakers are unlikely to be unanimous in their decision.

Construction Spending Rose in March: Nonresidential Gain Outweighs Another Residential Decline (Wells Fargo) - Construction spending rose 0.3% during March, which translates to a 3.8% year-over-year gain. The improvement in overall spending masks diverging trends between the residential and nonresidential sectors.

Private Residential Construction Spending Dips in March (NAHB) - Private residential construction spending inched down 0.2% in March, as spending on single-family construction decreased 0.8%. Spending on private residential construction declined for the tenth month in a row amid elevated mortgage interest rates. Consequently, this spending is 10% lower compared to a year ago.

Banking Strains Will Stress Economy (BMO) - With the risks of additional bank failures fading, a sense of calm has returned to financial markets. This follows the failure of three sizable U.S. banks, the latest being First Republic. The banking stress has eased with the initial sharp drop in deposits and lending now stabilizing, leaving the financial system still flush with liquidity. The Fed's emergency support to banks has also ebbed. However, higher deposit rates have increased bank funding costs and pressured loan margins, reducing the incentive to lend.

US Weekly Economic Commentary: Storm clouds building (S&P Global) - Economic and financial developments this week provided mixed signals on the state of the economy. On balance, these signals point towards an economy experiencing slowing growth, persistently high inflation, and building storms clouds that could spell trouble ahead.

US Economic Update – May 2023 (NAB) - GDP growth slowed in Q1 to a sub-trend 0.3% q/q, but this was largely due to inventories, with domestic final demand growth strengthening. There were some positive signs in the March PCE inflation data – with underlying measures printing on the low side (by recent standards) but further low prints are required to confirm inflation is decelerating, particularly given still elevated wage growth.

Europe

Negative impact of ECB tightening cycle and banking turmoil is unfolding (ING) - Weaker demand for loans, tighter lending standards and already muted loan growth support our view of a 25bp rate hike at Thursday's European Central Bank meeting.

ECB cheat sheet: Difficult to pull away from the Fed (ING) - The European Central Bank looks set to deliver at least two more hikes in this cycle. EUR swap forwards roughly agree with our forecast but EUR rates can only de-couple from their USD equivalents for so long. We see some downside risks for EUR/USD ahead of a 25bp compromise hike by the ECB this week, especially after the FOMC risk event.

China

China: Manufacturing PMI contracts in April (ING) - After avoiding monthly contractions since the start of 2023, China's manufacturing PMI showed activity contracted again in April. This is a warning signal to the Chinese economy. The slower expansion in non-manufacturing activity is not a concern just yet as it is usually quieter anyway for retailers in April before the long holidays in May.

Asia Poised to Drive Global Economic Growth, Boosted by China’s Reopening (IMF) - Asia and the Pacific is a relative bright spot amid the more somber context of the global economy's rocky recovery. The region will contribute about 70 percent of global growth this year—a much greater share than in recent years.

Canada

I'm Feeling '22 (BMO) - Most provinces benefitted from the lifting of pandemic-era restrictions in 2022. The Prairies received an added boosted from a jump in resource prices following the invasion in Ukraine, and from a rebound in agricultural production following the previous year’s drought. Altogether, the Canadian economy looks to have grown at a stronger-than-expected pace last year.

Inflation

Inflation Monitor for May 1 (BMO) - While inflation may be slowing, the path back to the 2% target may prove to be long and bumpy.

Real Estate

Improved Affordability Expectations Lead to More Engaged Buyers (NAHB) - Improvements in affordability expectations have led to an increase in the share of prospective buyers who have moved beyond just the planning phase of their home search: 56% report being actively engaged in the purchase process in the first quarter of 2023, up from 46% a quarter earlier.

Subscribe to receive Econ Mornings every weekday at 9 am. More economic and finance content on Twitter, Reddit, and my website.