Inflation and Tight Financial Conditions Weigh on the German Consumer

Economic news and commentary for August 29, 2023

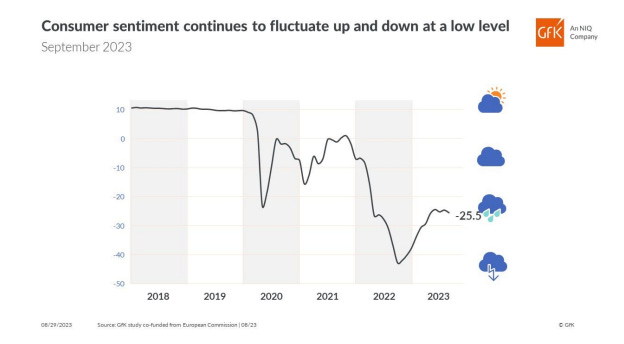

Germany GfK Consumer Sentiment

German economic data continues to point in the same direction, down. The latest GfK Consumer Sentiment report finds that there has been no improvement in consumer sentiment in August and that trend will continue going into the last month of the quarter. The reading for August was slightly above July, up 0.6 pts to -24.5, but that gain will immediately dissipate with a -0.9 pt drop to -25.5. From the GfK commentary: “Since consumer sentiment is likely to remain at a low level in the coming months, the assumption that private consumption will not make a positive contribution to overall economic development this year and will rather be a burden on growth prospects in Germany is confirmed.”

Some notable trends in the subindexes further outline the weakness of the German economy. The economic expectations index dropped -9.9 pts to the lowest value so far this year at -6.2. However, it’s still more than ten points above a year ago. Similarly, income expectations are worsening with a -6.4 pt decline to -11.5 in August. While the inflation situation has improved, it is still weighing on consumers. The propensity to buy has stagnated at a very low level overall, with no clear trend, since the summer of 2022 thanks to both high prices and tighter financial conditions. Today’s GfK data for August and September combined with the weak Ifo survey last week and the confirmation of stagnation in Q2 likely means that we’re set for a contraction in Q3 2023.

Still to come…

10:00 am (EST) - US Consumer Confidence

10:00 am - US JOLTS

Morning Reading List

Other Data Releases Today

Japan's unemployment rate increased 0.2 ppts to 2.7% in July, the highest since March. The total number of employed fell -10k while the total number of unemployed increased 11k. The 25-44 yr old age group saw the largest increase in joblessness.

The Germany GfK Consumer Sentiment index is estimated at -25.5 in September, down from -24.6 in August. The economic expectations indicator was the lowest so far this year in August at -6.2, down from 3.7 in July.

French household confidence was unchanged for the third month in a row at 85 in August. Expectations of household finances worsened -4 pts to -16 as the index tracking future inflation rebounded from lows, up 7 pts to -45.

US

At Jackson Hole, Fed Reinforces Policy Stance (PIMCO) - Federal Reserve Chair Jerome Powell is a good golfer, and if (as I thought going in) the goal of his speech at the Jackson Hole Symposium was to strike the ball down the middle of the fairway, then he achieved it – with perhaps a gentle draw in a hawkish direction. Powell’s clear, brief reiteration of the Fed’s monetary stance lent support to PIMCO’s outlook for perhaps one more interest rate hike this fall followed by an extended pause. He also noted Fed policy is likely to remain highly data-dependent.

Stocks Look Pricey (First Trust Portfolios) - So, if a large drop in the Treasury yield would likely come with a recession and lower earnings, and a sharp increase in profits would likely mean higher long-term interest rates, the market is stuck at current levels. And this, in our opinion, leaves only one main mechanism to bring actual stock prices and fair value back toward alignment: a drop in equity values.

US Weekly Economic Commentary: ‘Until the job is done’ (S&P Global) - Federal Reserve Chair Jay Powell, in strong and direct language, reiterated the Fed's commitment to bring inflation down to its 2% target in his remarks to the annual monetary policy conference hosted by the Kansas City Fed at Jackson Hole, Wyoming. He concluded his speech with this quote: "We will keep at it until the job is done."

AMW – What else occurred at Jackson Hole (NAB) - Jackson Hole is a three-day international central bank talkfest dating back to 1981, with its location a nod to US Fed Chair Volker for its proximity to fly fishing. This year’s conference was on “Structural Shifts in the Global Economy”. While no major central bank policy announcements were made, there were a few interesting themes relevant to markets which we explore in this week’s Weekly.

Economic Uncertainty, Rising Interest Rates Challenge Banks (St Louis Fed) - The U.S. banking system is sound and resilient, with strong capital and liquidity, according to the latest report on bank supervision and regulation released in May by the Federal Reserve Board of Governors. Nevertheless, bank supervisors are actively monitoring risks associated with credit, liquidity and interest rates. These risks have risen in 2023 because of prevailing economic conditions and uncertainty about the future path of the economy.

Inflation

It is all about lags and the wage inflation spiral (Saxo Bank) - Jackson Hole turned out to be a non-event for markets with the Fed keeping all options open. However, Powell did touch on two important topics of assessing lags of monetary policy into the economy and the stronger link observed in wage dynamics and inflation. These two topics mean that risks to the monetary policy path are still high and warrant higher for longer to avoid the mistakes made in the 1970s. We maintain our defensive view on equities which means that we are still overweight energy, utilities, health care, and consumer staples.

Inflation Monitor for August 28 (BMO) - U.S. inflation has eased meaningfully over the past year. Still, favourable base effects are fading, with retail gasoline now practically in line with year-ago levels.

Commodities

Weekly Pricing Pulse: Commodities up as supply concerns grow (S&P Global) - The Material Price Index (MPI) by S&P Global Market Intelligence increased 0.9% last week, returning to growth following two consecutive weekly declines at the start of August. Last week's increase was mixed with exactly half of the ten subcomponents rising. The trend so far in 2023 remains down with the index 30% lower than its year-ago level.

Trade

The High Cost of Global Economic Fragmentation (IMF) - Growing trade restrictions may reverse economic integration and undermine the cooperation needed to protect against new shocks and address global challenges.

Real Estate

Wood-Framed Home Share Increased for Three Straight Years (NAHB) - Wood framing remains the most dominant construction method for single-family homes in the U.S., according to NAHB analysis of 2022 Census Bureau data. For 2022 completions, 94% of new homes were wood-framed, another 6% were concrete-framed homes, and less than half a percent was steel-framed.

Research

Failing Just Fine: Assessing Careers of Venture Capital-backed Entrepreneurs via a Non-Wage Measure (Philadelphia Fed) - This paper proposes a non-pecuniary measure of career achievement: seniority. Based on a database of over 130 million resumes, this metric exploits the variation in how long it takes to attain job titles. When non-monetary factors influence career choice, assessing career attainment via non-wage measures, such as seniority, has significant advantages. Accordingly, we use our seniority measure to study labor market outcomes of VC-backed entrepreneurs.

Falling College Wage Premiums by Race and Ethnicity (San Francisco Fed) - Workers with a college degree typically earn substantially more than workers with less education. This so-called college wage premium increased for several decades, but it has been flat to down in recent years and declined notably since the pandemic. Analysis indicates that this reflects an acceleration of wage gains for high school graduates rather than a slowdown for college graduates.

Looking for a way to take advantage of higher interest rates? I recommend SoFi’s high-yield savings account which has a yield of 4.5% (subject to change) and includes FDIC deposit insurance for both its checking and savings accounts just like a traditional bank. Use my referral link to get a sign-up bonus and start earning that rate today. (This is also a great way to support me since I get a bonus too!)

Subscribe to receive Econ Mornings every weekday at 9 am. More economic and finance content on Twitter, Reddit, and my website. You can also see my feed on the PiQSuite platform as a partnered feed.