Inflationary Pressures Gradually Improve for Small Businesses in July

Economic news and commentary for August 8, 2023

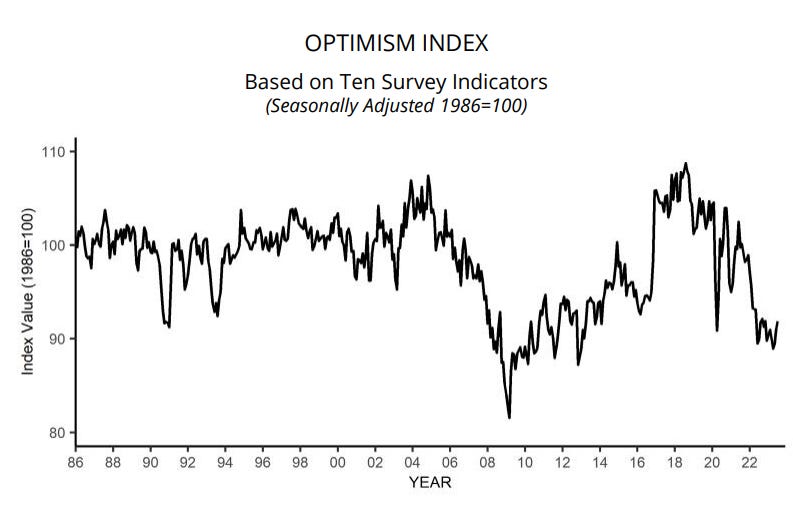

US NFIB Small Business Optimism

The NFIB Small Business Optimism Index grew 0.9 pts to 91.9 in July. Small businesses displayed optimism about the economy's potential improvement, which played a significant role in driving growth in the headline index. The economic expectations index saw a notable 10 pt increase, reaching -30, the highest level since August 2021. However, historically, this value remains considerably negative. While economic expectations improved, small business uncertainty continued to rise. The uncertainty index added 4 pts, reaching 80, marking the highest level since June 2021.

When it comes to hiring, small businesses reported marginally negative employment changes in July, with the Actual Employment Changes index remaining at -2, unchanged from the previous month. Despite this, the Job Openings index stayed robust at 42, which is above the pre-pandemic range of 33-39 but only slightly. Similarly, the Hiring Plans index showed positivity, albeit on the lower end of the pre-pandemic range of 16-21, with a value of 17. This suggests that small businesses are cautiously looking ahead to future hiring decisions but are still showing signs of expanding their labor forces.

In terms of inflation, July saw a slight easing of inflationary pressures for small businesses. The Actual Price Changes index dropped by 4 points to 25, the lowest since February 2021, indicating a moderation in price increases. Likewise, the Price Plans index fell by 4 points to 27, the lowest since December 2022, reflecting a decline in businesses' planned price adjustments. However, the compensation outlook remained somewhat concerning. The Actual Compensation Changes index increased by 2 points to 38, suggesting that small businesses may be facing challenges in managing employee compensation as it struggles with labor shortages.

Overall, it appears that the economic environment is starting to become more favorable to small businesses as inflation subsides. However, the effects of tighter financial conditions are still keeping optimism restrained and uncertainty high. Inflation concerns are receding but just gradually, and they remain one of the most pressing issues facing small business owners with 21% reporting it is their main concern (2nd to quality of labor). Interestingly, only 4% of firms see interest rates and financing as the single most important. Finally, employment appears to be slightly contracting in small businesses but only marginally. This does contradict the high level of job openings and a moderate level of hiring plans still reported, so the likely conclusion is that the labor supply is still an issue which is an inflationary concern. In the end, the July NFIB report is another piece of evidence that the Fed’s actions are bringing about a gradual improvement in the inflation issue, and there is still room for disentanglement despite the US’s economic resilience.

Still to come…

10:00 am (EST) - US Wholesale Inventories

9:30 pm - China CPI & PPI

Morning Reading List

Other Data Releases Today

Japanese household consumption fell -3.8% MoM and -0.5% YoY in June, down from -0.4% YoY in July. Both goods and services spending declined, down -1.3% MoM and -5.2% MoM. Both are down on a real YoY, -2.9% YoY and -3.2% YoY.

The NAB Business Conditions index fell -1 pt to 10 in July, and the Business Confidence index grew 3 pts to 2. The growth rate of labor costs and purchase costs grew from 3.7% QoQ (prev 2.3% QoQ) and 2.6% QoQ (prev 2.2% QoQ) respectively.

Germany's inflation rate was confirmed at 6.2% YoY in July. Core inflation was also confirmed at 5.5% YoY. Services inflation was 5.2% YoY, partially affected by a low base in Jun-Aug 2023 when the 9-euro ticket reduced transport prices.

US

Here’s Something to “Fitch” About (First Trust Portfolios) - Fitch said they downgraded the US because of massive deficits, “fiscal deterioration” and “erosion of governance.” Obviously, this downgrade, like the one by Standard & Poor’s in 2011 created political heat. We hope it creates action.

Is Recession Coming? Framework Says Yes (Wells Fargo) - Last year, we released a three-report series that outlined a couple methods to predict recessions and monetary policy pivots. Today, all three major tools still signal a recession within the next year. Despite the odds of a soft landing rising amid resilient economic data, the framework aligns with our base case expectation for a mild recession in early 2024.

US consumer spending remains vulnerable to credit dynamics (ING) - Consumer credit grew more than expected in June, led by car loans, but credit card spending contracted as borrowing costs hit record highs. With banks increasingly reluctant to finance consumer credit and with consumer spending responsible for two-thirds of economic activity, consumption expenditure looks set to come under intensifying pressure.

Danske Morning Mail: Weaker than expected NFP (Danske Bank) - The most important data release this week is US CPI for July due on Thursday. The lower than expected June number played a big role in the improving risk sentiment we saw last month and in lowering rate expectations. Also Norway, Denmark and Switzerland, and several euro area countries, will release CPI data this week, but not Sweden.

More Unequal We Stand? Inequality Dynamics in the United States, 1967–2021 (Minneapolis Fed) - Heathcote et al. (2010) conducted an empirical analysis of several dimensions of inequality in the United States over the years 1967-2006, using publicly-available survey data. This paper expands the analysis, and extends it to 2021. We find that since the early 2000s, the college wage premium has stopped growing, and the race wage gap has stalled. However, the gender wage gap has kept shrinking. Both individual- and household-level income inequality have continued to rise at the top, while the cyclical component of inequality dominates dynamics below the median. Inequality in consumption expenditures has remained remarkably stable over time. Income pooling within the family and redistribution by the government have enormous impacts on the dynamics of household-level inequality, with the role of the family diminishing and that of the government growing over time.

Europe

Europe: Well-positioned to get through next winter without major gas shortages (Federal Reserve) - Following Russia's invasion of Ukraine in early 2022 and resulting international sanctions, natural gas imports from Russia to Europe declined drastically to well below their historical averages (Figure 1). This reduction raised concerns about Europe's energy supply, given its dependence on Russian gas. One question that was prominent last year was whether Europe would be able to get through the winter without significant gas shortages. In the event, Europe weathered the past winter reasonably well, and the energy-related economic costs appear to have been more muted than initially feared.

Scarcity of collateral will contribute to European steepeners until inflation concerns revive (Saxo Bank) - Buba’s decision to stop paying interest on domestic government deposits provided fertile ground for the German yield curve to steepen today. If 2-year Schatz yields close below 2.95%, they will enter a bearish trend that might take them as low as 2.45%. Yet, as we approach the fall and inflation remains elevated, short-term yields are poised to rebound before a bond bull market forms.

Monitoring Turkey: Inflation fever (ING) - Turkey's inflationary downtrend ends as most factors are likely to exert upside pressure in the near term. While the Government pledges to fight inflation, its target is a soft landing in economic activity that implies quite a slow normalisation in economic policies amid a challenging disinflationary process.

National Bank of Romania review: It’s largely going according to plan but… (ING) - The National Bank of Romania (NBR) delivered as expected by us and the market, maintaining the key rate at 7.00% and making no changes to the standing facilities. The recently announced fiscal changes are added to the list of uncertainties marking the inflation outlook, which has shifted somewhat higher in the mid-part of the two-year forecast horizon.

Hungarian disinflation continued in July (ING) - While food deflation was weaker than expected, price pressures in other items showed a more marked easing. The July inflation figure does not change the big picture as we anticipate that disinflation will continue.

Japan

Does Japan’s higher rate cap materially hurt Treasuries? (ING) - The Bank of Japan allowed its 10yr yield to rise, just as the US 10yr yield broke above 4% and the curve started to dis-invert. Was that the causation? We think not. The lowering of the US rate cut discount is the biggest driver. Bigger deficits impact here too. The BoJ move is certainly pushing in the same direction, but it's far from the dominating influence.

Australia

Some favourable signs for inflation in Australian capacity use figures but labour market still very tight (NAB) - With this cycle having had particularly pronounced demand and supply shocks and central banks globally trying to achieve a better balance between demand and supply, we examine the aggregate and disaggregated measures of capacity utilisation in the NAB Business Surveys in greater detail in this week’s Australian Markets Weekly.

Inflation

Where Is Shelter Inflation Headed? (San Francisco Fed) - Shelter inflation has remained high even as other components of inflation have fallen. However, various market indicators, including house prices and rents, suggest that the housing market has slowed significantly with the rise in interest rates. Forecasting models that combine several measures of local shelter and rent inflation can help explain how recent trends might affect the path of future shelter inflation. The models indicate that shelter inflation is likely to slow significantly over the next 18 months, consistent with the evolving effects of interest rate hikes on housing markets.

Trade

Global trade downturn accelerates in July (S&P Global) - The worldwide Purchasing Managers' Index (PMI) surveys compiled by S&P Global Market Intelligence indicated a seventeenth successive monthly fall in global export orders for goods and services, signalling an extension of the deterioration in global trade performance into the second half of 2023. Falling to 47.8 in July from 48.3 in June, the seasonally adjusted PMI New Export Orders Index signalled a steepening of the downturn in global trade at the joint-fastest pace since last December.

Real Estate

Dramatic Apartment Construction Time Lengthening in 2022 (NAHB) - The average length of time to complete construction of a multifamily building, after obtaining authorization, was 19.8 months, according to the 2022 Survey of Construction (SOC) from the Census Bureau. The permit-to-completion time in 2022 was 2.3 months longer than in 2021, as supply-chain issues and the ongoing skilled labor shortage challenged the industry.

Real Estate Helped Drive Wealth Gains during the Pandemic (St Louis Fed) - How did the performance of different assets (what households own) influence racial wealth outcomes during the COVID-19 pandemic? Despite recent wealth gains during the pandemic, the average Black family owned about 24 cents for every $1 of white family wealth as of the first quarter of 2023.1 Similarly, the average Hispanic family owned about 23 cents for every $1.

Research

Scalable Demand and Markups (Philadephia Fed) - We study changes in markups across 72 product markets from 2006 to 2018. A growing literature has documented a rise in markups over time using a production function approach;

we instead employ the standard microeconomic method, which is to estimate demand and then invert firms’ first-order pricing conditions to infer their markups. To make the method scalable, we propose estimating nested logit demand models, using household panel data to automate the assignment of products to nests. Our results indicate an overall upward trend in markups between 2006 and 2018, with considerable heterogeneity across and within product markets. We find that changes in firms’ marginal costs and households’ price sensitivity are the primary drivers of markup increases with changes in firm ownership playing a much smaller role.

Crypto

Feeling the winter: The liquidity dries up (Saxo Bank) - The crypto spot volume has fallen off a cliff in the past one and a half years, as the crypto market struggles to find its role in the present high interest rate environment. Too, it does not help with the market’s efficiency and liquidity that market makers cannot trade as efficiently as previously after Silvergate Bank and Signature Bank ceased operations.

Looking for a way to take advantage of higher interest rates? I recommend SoFi’s high-yield savings account which has a yield of 4.5% (subject to change) and includes FDIC deposit insurance for both its checking and savings accounts just like a traditional bank. Use my referral link to get a sign-up bonus and start earning that rate today. (This is also a great way to support me since I get a bonus too!)

Subscribe to receive Econ Mornings every weekday at 9 am. More economic and finance content on Twitter, Reddit, and my website. You can also see my feed on the PiQSuite platform as a partnered feed.