Service Sector Data to Start the Week

Macro and market developments for 2/5/2024

S&P finishes reporting its PMIs with the composite and services reports. Meanwhile, the euro area PPI report comes in with positive signs of easing inflation, and German trade data takes another tumble in December.

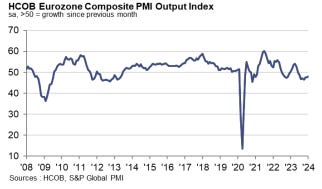

Eurozone: Services and Composite PMIs Still Contracting

The S&P Eurozone Composite PMI grew to a 6-month high of 47.9 in January, up from 47.6 in December. Business activity and new orders remained in contraction, but that was balanced by a strong increase in growth expectations which reached a 9-month high. The survey noted that European economies in the south separated themselves from the greater region with growing services sectors. Spain and Italy, the southern economies in question, saw six and eight-month highs in their Composite PMIs respectively. Despite a broad decline in the eurozone economy, input and output price growth was the strongest in 8 months as a result of services inflation.

Though the sector was still inflation, services activity maintained a decline going into the new year. The S&P Eurozone Services PMI fell to 48.4 in January, down from 48.8 in December, a 3-month low. This means that the service sector has been in a contraction for six straight months with new business depleting for seven straight months. Again, it is worth noting that Spain and France stood out from the rest with services PMIs in expansion, at 52.1 and 51.2 respectively.

Elsewhere, euro area PPI growth eased to -0.8% MoM in December, the lowest since May 2023, and the YoY rate fell to -10.6% YoY, down from -8.8% YoY in November. Excluding energy, producers enjoyed a third straight month of falling YoY prices at -0.4% YoY. While energy was a broad driver of deflation, down -27.5% YoY, other commodities also maintained a price decline over the last year, down -4.9% YoY. On the other hand, PPI inflation rates for capital goods, durable consumer goods, and non-durable consumer goods all eased and landed around 3%.

Other S&P Services PMI for January

Asia

India: 61.8 (Dec 59.0)

Russia: 55.8 (Dec 56.2)

Japan: 53.1 (Dec 51.5)

China: 52.7 (Dec 52.9)

Australia: 49.1 (Dec 47.1)

Europe

UK: 54.3 (Dec 53.4)

Spain: 52.1 (Dec 51.5)

Italy: 51.2 (Dec 49.8)

Eurozone: 48.4 (Dec 48.8)

Germany: 47.7 (Dec 49.3)

France: 45.4 (Dec 45.7)

Germany: Trade Plummets in December

Germany ended the year with a sharp decline in trade. In December, exports fell -4.6% MoM and imports fell -6.7% MoM. The robust drop in imports meant that the trade balance expanded to €22.2 billion, a multi-year high. For the full year 2023, the trade balance ended at €209.6 billion, a huge rebound from the €88.6 billion in 2022 (which was the lowest since 2000). Germany’s trade surplus is being supported by a decline in energy import prices as well as weak domestic demand that is causing a decline in demand for foreign goods. Imports from EU countries fell -7.4% MoM, and imports from non-EU countries fell -5.9% MoM. For the full year 2023, imports shrank -9.7%.

In the News

US Threatens to Escalate in the Middle East and Yemen

The United States has issued a stern warning, declaring its intent to escalate attacks against Houthis and other Iranian proxies in the Middle East if there are further assaults on commercial ships. While emphasizing that the US is not seeking a broader conflict, officials stress that the recent attacks are just the beginning of their response. These threats come in the aftermath of US strikes targeting over 85 locations across seven facilities, a retaliatory measure in response to the deaths of US troops. Late Sunday, the Islamic Resistance claimed responsibility for an attack on a base housing US troops in Syria. No US troops were hurt but six Kurdish fighters were killed.

Fed Chair Powell's 60 Minutes Interview

Federal Reserve Chair Jerome Powell, in a 60 Minutes interview, said that a strong US economy means that the Fed can approach rate cuts with caution this year. Powell expressed concerns about premature cuts leading to sustained inflation above the 2% target. He emphasized the need for more evidence that inflation is moving down before cutting, acknowledging that the Fed's job is not yet complete. Powell admitted that earlier tightening in 2021 would have been preferable. While downplaying concerns of a banking crisis due to commercial real estate, he acknowledged potential challenges for smaller banks which could include some collapses or mergers for smaller banks. Powell anticipates future rate cuts, emphasizing their non-political nature.

Chinese Regulators Pledge More Market Support

The China Securities Regulatory Commission announced measures to prevent abnormal market fluctuations, aiming to attract more medium- and long-term funds. This move comes as the CSI 300 experiences a five-year low and records a sixth consecutive losing month in January. Some reports suggest China is contemplating a 2 trillion yuan ($278 billion) stock stabilization fund to further stabilize markets.

Boeing Encounters More Manufacturing Issues

Boeing has identified additional problems with 737 jets, potentially causing delays in delivering around 50 aircraft. Specifically, misdrilled holes in fuselages were discovered by an employee at a supplier. While the issue does not pose an immediate safety threat, the 50 undelivered planes will require repairs. This development comes as the 737 Max 9 planes are gradually returning to service following a prior incident that led to an emergency landing of an Alaska Airlines flight.

Earnings

McDonald's (MCD, consumer staples) fell short of comparable sales expectations, with global comparable sales up 3.4%, below the 4.8% consensus. The US and international segments reported 4.3% and 4.4% growth, below expected figures of 4.5% and 8.3% respectively. Middle East sales were impacted by ongoing geopolitical events.

Caterpillar (CAT, industrial) reported moderate sales growth, slightly missing expectations, with revenues reaching $17.1 billion, a 3% YoY increase. Sales volume declined, primarily due to changes in dealer inventories, offset by higher equipment sales to end-users. Construction and Resource Industries segments saw a decline of -5% and -6%, while Energy & Transportation increased by 12%. Overall, the Machinery, Energy & Transportation industry saw a modest 2% growth. The full-year revenue for 2023 increased by 13%, driven by favorable price realization and higher sales volume. The profit margin significantly improved from 10.1% in Q4 2022 to 18.4% in Q4 2023. Cat Financial reported substantial YoY revenue gains, attributed to higher rates.

For more macro and market commentary, check out my Reddit feed.