Small Business Sentiment Improves in June but the Inflation Situation Didn't Imrove

Economic news and commentary for July 11, 2023

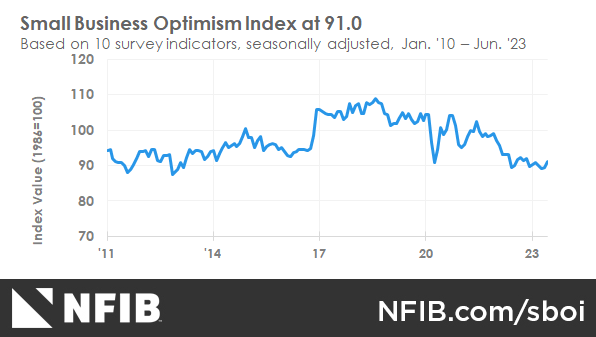

US NFIB Small Business Optimism Index

The NFIB Small Business Optimism Survey for June provided insights into the sentiment of small businesses, offering a glimpse of pricing trends at that level ahead of the upcoming CPI release. While there were some positive developments, challenges such as inflation and labor quality continued to weigh on small business owners. The NFIB Small Business Optimism Index saw a modest increase of 1.6 points to reach 91.0 in June. However, this marks the 18th consecutive month below the long-term average of 98, indicating that small businesses still face headwinds.

The gain in the index can be attributed to improvements in small business expectations about future conditions, likely due to the recent decline in inflationary pressures. Notably, the economic expectations index jumped by 10 pts to -40%, reflecting a more optimistic outlook among small business owners. The sales expectations index also showed improvement, rising 7 pts to -14%. These positive shifts in economic and sales sentiment were accompanied by small improvements in expectations regarding credit conditions and future expansion plans. Offsetting these positive indicators was a decline in small businesses' plans to increase employment. The index tracking employment plans dropped by -4 pts to 15%, reaching its lowest level this year and the lowest since the onset of the pandemic. This decline was somewhat correlated with a slight decrease in the job openings index, down -2 pts to 42, the lowest so far in 2023, and approaching the averages seen in the 2018-2019 period.

The update on small business inflation data presented a mixed picture. Price pressures have eased in recent months, as reflected by the NFIB Price Changes index, which fell by -3 pts to 29 in June, reaching its lowest level since March 2021. However, the Price Plans index increased by 2 points to 31, marking the highest level so far this year. This suggests that while immediate price pressures may be easing, small businesses are still anticipating higher prices in the future.

The core issues facing small businesses remain unresolved. Inflation and labor quality were identified as the top concerns among small business owners, with 24% expressing worry about these factors. This concern has remained relatively unchanged over the past few months. Looking ahead, the Federal Reserve is expected to take further action to address these challenges in its July meeting, including the possibility of another rate hike.

Still to come…

7:50 pm (EST) - Japan Machinery Orders

7:50 pm - Japan PPI

Morning Reading List

Other Data Releases Today

The Westpac Index of Consumer Sentiment increased 2.7% MoM to 81.3 in July. The cooling of inflation has helped ease sentiment from its declines over 2022.

Interest rate expectations fell -2.3% MoM to 174.8 which is still high historically.

German inflation was confirmed at 0.3% MoM and 6.4% YoY, and core inflation was confirmed at 5.8% YoY. All other segments were confirmed at the initial estimate as well.

The UK saw a decline of -9,000 jobs in June, and the unemployment rate grew 0.2 ppts to 4.0% in the 3 months to May. Job vacancies fell -85,000 to 1.0 million, and the inactivity rate fell -0.4 ppts to 20.8%. Both signal a looser labor market.

Italian industrial production grew 1.6% MoM in May but was still down -3.7% YoY. The average 3-month change of production is still low at -1.8%.

The ZEW Indicator of Economic Sentiment for Germany fell -6.2 pts to -14.7, and the Economic Situation Germany fell -3.0 pts to -59.5. The current situation indicator for the eurozone decreased, dropping 2.5 pts to a new reading of -44.4.

UK Employment

UK wage growth surprise could spell repeat 50bp rate hike (ING) - A few months ago it looked like UK wage growth had peaked. Now it is running at its fastest pace yet, and, depending on next week's inflation figures, it could push the Bank of England into another 50bp rate hike in August.

Italy Industrial Production

Italian industrial production rebounds in May, but it could prove temporary (ING) - The distribution of holiday days in April could be one explanation behind the reason behind recent volatility in Italian industrial production. We continue to see industrial weakness, at least in the short run.

US

Resilience, stubborn inflation, more rate hikes (S&P Global) - Labor market indicators, including Friday's employment report for June, the Job Openings and Labor Turnover Survey (JOLTS), and initial claims for unemployment insurance, on balance show a labor market that remains very tight — with a significant excess of demand over supply — and only hints that conditions are loosening.

Still Overvalued (First Trust Portfolios) - The Goldilocks future, where the Fed manages everything perfectly, is likely too optimistic. Some stock valuations have become too high in our opinion. More defensive strategies are appropriate at this juncture.

Financial Shocks in an Uncertain Economy (Dallas Fed) - The past 15 years have been eventful. The Global Financial Crisis (GFC) reminded us of the importance of a stable financial system to a well-functioning economy, one with low and stable inflation and maximum employment. Given the recent banking stress, we ponder this issue again. The pandemic was a huge shock surrounded by much uncertainty, making precise forecasts within traditional models difficult. And more recently, there has been continuous talk of a soft landing and recession risks.

Reducing Inflation along a Nonlinear Phillips Curve (San Francisco Fed) - Inflation has climbed since 2021, as the labor market has tightened. Two historical data relationships can account for elevated inflation over the past two years: the Beveridge curve, which relates job vacancies and unemployment rates over the business cycle, and a nonlinear version of the Phillips curve, which links inflation to labor market slack. Combining estimates of the two curves implies that inflation can fall in conjunction with a “soft landing” for the economy if labor market easing is achieved mainly by reducing job vacancies rather than increasing unemployment.

US hedge funds continued to UNDERPERFORM in June (Saxo Bank) - US hedge funds continued to underperform in June. They were up +1.3% relative to US stocks which were up +6.4% in June. Two insights: (1) US activist hedge funds had a banner month up +6.1% in June. (2) Even US hedge fund giants underperformed broad markets in 2023.

Are Higher Child Care Wages Affecting the Labor Supply? (St Louis Fed) - We analyze state-level data over time to determine whether higher child care wages are affecting the labor supply. We examine whether states that saw greater increases in child care costs also showed weaker rebounds of LFP rates for individuals with children.

Europe

Political uncertainty in the Netherlands to slow greening of the economy (ING) - The Dutch government collapsed on Friday after being in power for just 18 months. Today, PM Mark Rutte announced he will leave politics. New elections will probably take place in November. Within many large political parties, the leadership is now up for grabs, implying high uncertainty. Here, we look at the economic impact over the shorter and medium term.

NATO in the spotlight (S&P Global) - The North Atlantic Treaty Organization, better known as NATO, was having a bit of an identity crisis when Russia invaded Ukraine in 2022. That seismic event made membership in the 74-year-old alliance a hot ticket.

Flash Comment Riksbank - June 2023 Minutes - In line with the June MPR (Danske Bank) - Overall, we find the minutes from the June MPR as neutral as we find no surprising comments in any direction from the board members. The risk to inflation is still there, particularly in the service inflation, and the board seems to be on the alert for signs of wage drift.

Riksbank minutes: Pressured by core inflation (Nordea) - The minutes from the policy meeting in June showed that higher-than-expected service inflation and the weak SEK are a main concern for the Board. All members indicated that the policy rate could be hiked more than indicated in the rate path.

Sweden June 2023 Inflation Preview (Danske Bank) - Swedish June inflation should print close to Riksbank's forecsts (n.b. CPIF 6.0 % yoy and CPIF ex. Energy 7.8 % yoy), where we expect 6.0 % yoy and 7.7 % yoy). Market expectations are slightly higher.

NO Inflation Review: New record-high core (Nordea) - Norwegian Core inflation jumped to 7.0% y/y compared to Norges Bank's expectations at 6.6%. We still expect Norges Bank to raise the key rate to 4.25% in September.

Higher deficit and unidentified outflows weigh on reserves in Turkey (ING) - External pressures in Turkey continued with another higher-than-expected current account deficit in May, while reserves have remained under pressure given weak capital flows.

China

China | 2023 RMB Exchange Rate Outlook (BBVA) - RMB to USD exchange rate has cumulatively depreciated by 8% in 2023, amid expectation change of the US FED hike path. Look forward, we predict RMB to go back to around 7-7.1 at end-2023 and 6.7 at end-2024.

Inflation

Inflation Monitor for July 10 (BMO) - The U.S. and Canadian labour markets are still tight, keeping wage pressures elevated.

Monetary Policy

Dollars and Sense: Central Banks: Learning to Skip (TD Bank) - The Federal Reserve has moved to a meeting-by-meeting approach as it explores the stopping point on interest rates. We think that occurs at 5.50%, but even in that case, the Fed will need to ensure communication jawbones the market to prevent a drop in yields. The Bank of Canada has already jumped back in with another hike after pausing in January. The population surge poses a challenge for a central bank that would prefer to remain on the sidelines but cannot ignore the demand shock.

Opening remarks at the Panel on Policy Challenges for Central Banks, 2023 annual meeting of the Central Bank Research Association (Lorie Logan, Dallas Fed) - Dallas Fed President Lorie Logan delivered these remarks before the Central Bank Research Association Annual Meeting at Columbia University, New York.

Commodities

Nickel underperforms as surplus builds (ING) - Nickel has been the worst performing metal on the London Metal Exchange (LME) so far this year with prices slumping 37% in the first half of the year. This underperformance is likely to continue as we head into the second half of 2023 with the market likely to test lower levels amid a weak macro picture and sustained market surplus.

Subscribe to receive Econ Mornings every weekday at 9 am. More economic and finance content on Twitter, Reddit, and my website.