The Bank of England Pauses in a Near Split Decision

Economic news and commentary for September 21, 2023

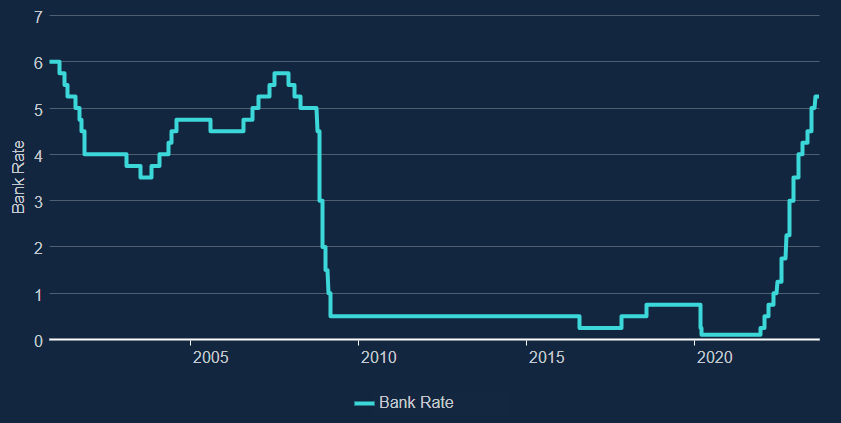

Bank of England Announcement

This morning, the Bank of England maintained its Bank Rate at 5.25%, ending a string of rate hikes that started back in December 2021. The pause was not without controversy as the BoE Monetary Policy Committee (MPC) as the vote was passed by slim margin of 5-4. The dissenting minority wanted a 25 bps rate hike. The announcement also included the decision to reduce to slow the rate of quantitative easing. Specifically, the MPC voted to reduce the amount of UK government bond purchases over the next 12 months by -£100 billion to £658 billion. This announcement comes after UK CPI inflation rates surprised to the downside on lower-than-expected services inflation.

It appears that the reason for the pause was likely related to that inflation release which may have caused an abrupt reassessment of the inflation risks. The MPC noted that the decline in annual inflation from 7.9% in June to 6.7% in August was “0.4 percentage points below expectations at the time of the Committee’s previous meeting” with both goods and services CPI inflation surprising to the downside. However, it also notes that these outsized declines were caused by the airfares & accommodation segment which “tend to be volatile over the summer holiday period.” In the next paragraph, it retreats from its admission of progress and states that services inflation “is projected to remain elevated in the near term.”

On the labor market and wages, the MPC says that it has started to see the impact of higher rates. This is likely referring to the recent rise in the unemployment rate and the continued decline in job vacancies which had been elevated for some time. The language that ends the official announcement suggests that these numbers are being just as closely monitored as inflation rates. In fact, the MPC specifically mentions that it is closely monitoring signs of inflationary pressures such as “the tightness of labour market conditions and the behaviour of wage growth and services price inflation.” Thus, we should look there as well for guidance on the BoE future decisions.

The final paragraph is a quick note on the reduction of asset purchases. The MPC notes that this action was already and agreed upon discussion point in September, and that the decision to implement some form of quantitative tightening should be a surprise to no one. The size of the reduction looks to have been guided by the market as the minutes mention that “the median market expectation for the MPC’s pace of gilt stock reduction over the year ahead was £100 billion.”

The minutes of the MPC describe the situation best: “For most members within this group, the latest developments meant that the judgement to keep Bank Rate unchanged at this meeting rather than increase it was finely balanced.” While the pause feels decisive, it was not by any means, and because of that, it really does feel like this week’s inflation release made a huge difference in the voting today. Since the BoE has adopted this hyper-data-dependent mode, it should be no surprise that a reversal in the disinflation trend as demonstrated by future data would likely cause a reversal on the sentiment of the MPC. For now, however, the members can rest on the fact that the lagging nature of monetary policy suggests that much of that tightening has yet to make a major impact yet. The hope is that inflationary pressures will respond to these restrictive conditions and continue to trend the right direction.

Still to come…

10:00 am (EST) - EU Consumer Confidence Flash

10:00 am - US Existing Home Sales

10:00 am - US Leading Indicators

10:30 am - US EIA Natural Gas Report

7:30 pm - Japan CPI

10:30 pm - Bank of Japan Announcement

Morning Reading List

Other Data Releases Today

France's business climate indicator was 100 for the 5th straight month in September. The manufacturing indicator improved 2 pts to 99 while building construction edged down -1 pt to 105 and retail fell -2 pts to 103.

Jobless claims grew 3,000 to 220,000 last week. The insured unemployment rate was unchanged at 1.1%. Continued claims edged up 4k to 1.69 million.

The Philadelphia Fed Manufacturing Survey Business Activity index fell -25.5 pts to -13.5 in September. The New Orders index dropped -26.2 pts to -10.2, and Inventories flipped to increasing (8.9, up 19.1 pts). Prices Paid up 4.9 pts to 25.7.

The US current account deficit decreased by $2.4B to $212.1B in Q2 2023, representing 3.2% of the GDP. This reduction is attributed to increased surpluses in services and primary income, even though the goods deficit expanded.

FOMC Announcement

Fed holds rates, raises guidance for rates in 2024 (TD Bank) - With the Fed previously signaling that a hike was off the table for today's meeting, everyone likely skipped over the press release and went straight to the FOMC Members' forecast. The Fed is now forecasting the closest thing to a perfect landing for the economy. Real GDP growth barely moves below its trend pace in 2024, while the unemployment rate effectively lands right on its steady state level, and inflation wonderfully grinds back to target. At the same time, Fed members maintained their view that one more hike is on the table for 2023, while reducing (and implicitly pushing out the timing of) rate cuts in 2024.

Message from FOMC Meeting: Higher for Longer (Wells Fargo) - As widely expected, the FOMC kept its target range for the federal funds rate unchanged at 5.25%-5.50% at today's policy meeting. The decision to keep rates unchanged was unanimously supported by all twelve voting members of the Committee.

Fed holds rates steady now but unsure about the future (CIBC) - Today’s no-surprise FOMC decision to keep rates unchanged comes with a side of caution as the dot plot continued to show another hike this year isn’t off the table and that the Fed expects to hold rates higher for longer. The projections significantly revised the outlook for the economy beyond this year, with the output gap materially less negative in 2024 and 2025 than they expected in June.

FOMC Commentary from MBA's Mike Fratantoni (Mortgage Bankers Association) - As expected, the Federal Reserve did not change its federal funds rate target at the September meeting. However, the FOMC members’ projections signal that they believe they are not yet done in their fight to bring inflation down. The majority of FOMC members still expect another hike this year, even though core inflation has slowed. And many FOMC members now expect that the pace of cuts in 2024 will be somewhat slower than they had thought in June.

Fed holds US rates steady, but markets are reluctant to buy into the more hawkish messaging (ING) - The Fed has left the Fed funds target range at 5.25-5.5% and continues to indicate the prospect of another 25bp hike this year. Longer term, the Fed is signalling less prospects of rate cuts and a diminishing chance of a recession as it guides inflation back to 2%. Given the challenges the economy faces, the market is understandably sceptical.

You Know It When You See It (First Trust Portfolios) - While the Fed kept rates unchanged at today’s meeting, between the press conference and forecast updates, Powell and Co. gave plenty of ammo to keep the financial press busy

speculating about what may come at the next FOMC meeting this Fall.

Fed Holds Rates Steady, but Hawkish Dots Push Bond Yields Higher (HilltopSecurities) - This afternoon, Fed officials voted unanimously to hold the overnight funds target steady at 5.25% to 5.50%. The September pause was fully expected, but a significantly more hawkish outlook was not.

One More Fed Rate Hike in 2023? (NAHB) - The Federal Reserve’s monetary policy committee held the federal funds rate at a top target rate of 5.5% at the conclusion of its September meeting. The Fed will also continue to reduce its balance sheet holdings of Treasuries and mortgage-backed securities as part of quantitative tightening. These actions are intended to slow the economy and bring inflation back to 2%.

FOMC Policy Announcement and SEP — Onward November (BMO) - The FOMC kept the fed funds target range unchanged at 5.25%-to-5.50% today, as expected, after lifting it by 25 bps last meeting. This repeats the first part of the skip-hike sequence established three months ago. And, importantly, the Fed has left the door open for a potential second-leg rate hike come the next announcement on November 1.

Research US - Fed review: Upbeat on growth (Danske Bank) - The Fed maintained Fed Funds Rate target unchanged at 5.25-5.50% as widely anticipated, but surprised hawkishly with clearly more optimistic projections. Median growth forecasts were revised higher for 2023-2024, warranting a 50bp upward revision to both 2024 & 2025 median rate projections.

FOMC Review: Still searching for the right level (Nordea) - The FOMC kept rates on hold while projecting one more hike this year. Growth projections were higher, and members now only see 50bps of cuts next year, half the June amount.

Hawkish Fed to proceed ‘carefully,’ but stay ‘higher for longer’ (EY Parthenon) - There was no surprise in the Federal Reserve’s decision to hold the federal funds rate at 5.25%–5.50%. The Federal Open Market Committee (FOMC or Committee) statement was little changed, with policymakers unanimously voting to hold the federal funds rate steady while preserving the conditional optionality for further tightening, should it be necessary.

France Business Climate

French business climate stable again, but inflationary pressures on the rise (ING) - Business sentiment remained stable in France in September, a sign that economic activity is holding up, but lacking dynamism. Worryingly, inflationary pressures are rising again.

US

Rise of the Machines: U.S. Business Investment Resists High Rates (TD Bank) - Despite interest rates rising to a 22-year high and credit conditions tightening to levels consistent with an economic downturn, business investment continues to display incredible resilience. Bipartisan legislation, including the CHIPS & Science Act and the Inflation Reduction Act, aimed at greening the economy and reshoring semiconductor production are partly to credit, alongside state and local government incentives.

Europe

Dutch Macro Perspectives - Budget Day light on policy, with focus on fighting poverty (ABN AMRO) - This year’s ‘Prinsjesdag’ (The Netherlands’ Budget day) took place against a different backdrop. First and foremost because of the caretaker status of the government. Secondly, the macro-economic environment has changed compared to recent years. As was already signalled by leaks to the press in recent weeks, few policy changes were presented today. No major policy overhauls were announced except for a small package to support household income.

ECB shows that transition risks will have a significant impact on corporates and banks (ABN AMRO) - The ECB stress-tested the economy under different transition scenarios over an 8-year horizon. Corporates are affected by transition risks through lower profitability and higher leverage, which result in higher credit risk. This increased risk ultimately feeds into banks’ own credit risk, which could lead to significant expected losses. Transition risk for the banking sector in the euro-area is very much concentrated within a few large banks.

EUR rates: Done (Nordea) - The ECB is done and now considering its next options. Upcoming discussions about speeding up QT and raising required reserves have added to momentum in German ASW tightening, 10s30s steepening and renewed the interest to look at €STR/BOR wideners.

Norges Bank hikes and promises one more in December (ING) - Norges Bank delivered a well-telegraphed 25bp hike today, but surprised markets by signalling rates will likely be increased again to 4.50% in December and left at that level throughout 2024. Despite the hawkish surprise, EUR/NOK has remained attached to the 11.50 gravity line. This will continue to be the case until the external environment swings.

A surprise pause by the Swiss National Bank, which could last for some time (ING) - The Swiss National Bank (SNB) surprised today by deciding to take a break from its cycle of rate hikes, keeping its key rate at 1.75%. Inflation expectations have been revised downward and the outlook for growth is weaker. That means this pause could last.

Riksbank’s half-hawkish hike leaves the krona vulnerable (ING) - Sweden's Riksbank has raised rates and signalled a 40% chance of another hike, which we think could be delivered if we get renewed SEK weakness or renewed upside surprises on inflation. Our base case is no more hikes. SEK dodged a drop thanks to the reserve hedging announcement, but lack of hawkish conviction leaves it vulnerable.

Swedish Labour Market: Turning point (Nordea) - The employment growth dropped markedly in August after the big uptick in July and the unemployment rate increased.

Canada

BoC Summary of Deliberations — Finger Still On the Hike Button (BMO) - The summary of the Bank of Canada’s deliberations from the September 6th meeting reiterated a hawkish bias. Recall that meeting saw the Bank pause after two consecutive 25 rate hikes, leaving the policy rate at 5%, or the highest since March 2001.

Inflation

The outlook for inflation? It's sticky (S&P Global) - The near-term outlook for inflation has deteriorated. S&P Global Market Intelligence's September forecasts for global consumer price inflation have been revised higher in both 2023 and 2024. This partly reflects the impact of higher crude oil prices. The prices of some non-energy industrial commodities have also rebounded, although they remain well below the peaks of 2022. Sticky core inflation rates, particularly for services, are a prime concern given generally tight labor market conditions and elevated wage and unit labor cost growth.

Real Estate

Mortgage Applications Increase in Latest MBA Weekly Survey: Week of September 15, 2023 (Mortgage Bankers Association) - Mortgage applications increased 5.4 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending September 15, 2023. Last week’s results included an adjustment for the Labor Day holiday.

Markets

Americas CIO View: Not Goldilocks for Stocks: Job market still too hot, profit growth still too cold (DWS Group) - U.S. gross domestic product (GDP) hasn’t stalled or even slowed much from 525bp of U.S. Federal Reserve (Fed) hikes the last 18 months. Resilience is from a robust service economy and service job creation. But S&P earnings per share (EPS) is flat to slightly down since Fed hikes started, stuck at $220 of annualized S&P EPS since 1Q22.

Research

How usable are capital buffers? (ECB) - This paper analyses banks’ ability to use capital buffers in the euro area, taking into account overlapping capital requirements between the risk-based capital framework and the leverage ratio capital framework from 2016 to 2022.

Looking for a way to take advantage of higher interest rates? I recommend SoFi’s high-yield savings account which has a yield of 4.5% (subject to change) and includes FDIC deposit insurance for both its checking and savings accounts just like a traditional bank. Use my referral link to get a sign-up bonus and start earning that rate today. (This is also a great way to support me since I get a bonus too!)

Subscribe to receive Econ Mornings every weekday at 9 am. More economic and finance content on Twitter, Reddit, and my website. You can also see my feed on the PiQSuite platform as a partnered feed.