UK CPI: Energy Inflation Crashes but Services Inflation is Still Sticky

Economic news and commentary for August 16, 2023

UK CPI & PPI

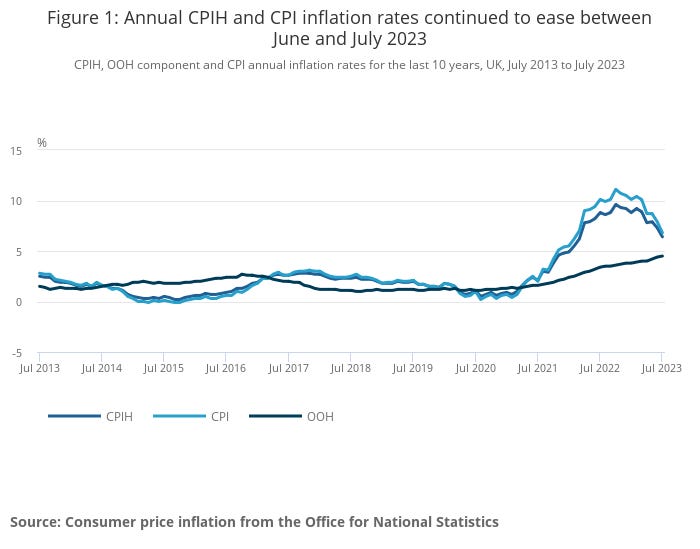

UK CPI grew 0.4% MoM and 6.8% YoY in July, down from 7.9% YoY in June. The decline in the headline annual rate can be attributed almost entirely to falling gas and electricity prices which had been the main source of the cost-of-living crisis that has developed over the last two years. The energy index fell -9.5% MoM last month which caused the annual rate to turn sharply negative at -7.8% YoY in July (down from 3.2% YoY in June). Normally, elevated food costs would offset the decline in energy, but in the last few months, inflationary pressure from food has eased. Food price growth was just 0.2% MoM increase, and YoY food inflation fell to the lowest point since the beginning of the year at 13.2% YoY. These trends in the volatile categories has led CPI inflation to the lowest since February 2022.

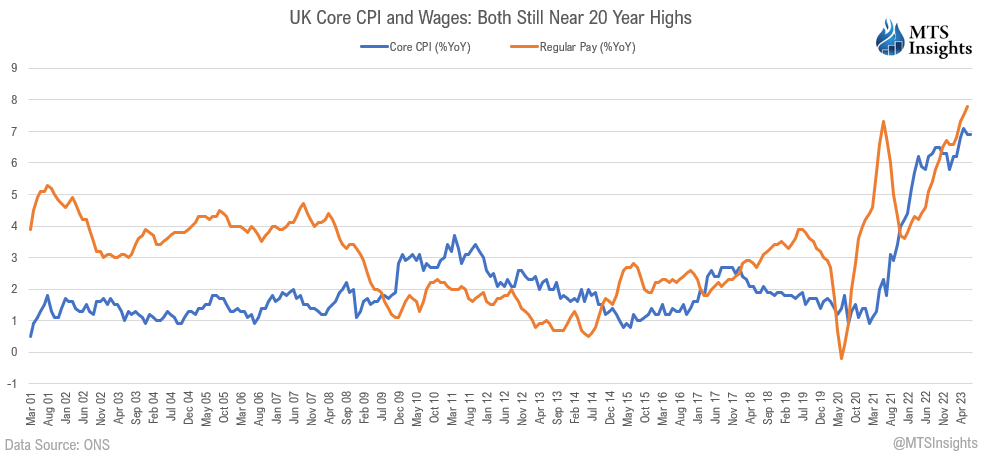

A different story is told by core CPI inflation. YoY core CPI growth was 6.9% YoY in July, unchanged from 6.9% YoY in June. This is near its high of 7.1% YoY and about half a percentage point to a percentage point higher than the range in 2022. The services index continues to keep core inflation sticky. Services inflation was 7.4% YoY, up slightly from 7.2% YoY previously. In July, hotels and air travel were the largest upward contributors. Travel & transport services inflation jumped to 10.6% YoY, a new peak, and the index tracking package holidays and accommodation services was 12.1% YoY. On the core side, durable goods prices are the main source of disinflation at -1.3% MoM and the annual rate falling -0.9 ppts to 3.9% YoY, the lowest of the notable goods type aggregates.

A similar story is told by the PPI report released today. Oil and petroleum inputs caused both input and output PPI growth to fall deeper into negative territory. Input prices were down -0.4% MoM and -3.3% YoY, and output prices were up slightly by 0.1% MoM but down -0.8% YoY. Notably, the annual inflation rate of the output PPI was negative for the first time since December 2020. This is the twelfth consecutive month that the annual inflation rate has slowed. However, the cause of that decline can be traced back to the sharp -40.0% YoY decline in petroleum product output prices.

The substantial decline in headline CPI inflation is a strong positive for UK consumers. Out of all the developed economies, UK households have felt the most hard done by inflation due to the sharp energy shock. That shock does seem to be over for the most part. Outside of the easing there, inflation has not abated with the exception of the durable goods category. Services inflation is the main talking point and is the main reason for sticky core CPI inflation due to the concentration of consumer demand in the services sector. Despite higher costs, consumers are not giving up on travel plans which suggests a lot about the strength of household financial conditions despite higher interest rates.

The Bank of England has largely expected services inflation to maintain its pace, saying in the most recent Monetary Policy Report that “services CPI inflation was projected to remain broadly unchanged in the near term.” However, any ticks upward will likely be met with similar upticks in the BoE’s hawkish rhetoric. The new near term peak in wage growth (up 7.8% YoY in Q2 2023, the highest since 2001) is also something that BoE members will consider in assessing the stickiness of services inflation. With that being said, if they decide that core CPI is the problem that needs to be solves, another rate hike is likely coming in the next meeting in September.

Still to come…

9:15 am (EST) - US Industrial Production

10:00 am - US Atlanta Fed Business Inflation Expectations

10:30 am - US EIA Petroleum Status Report

2:00 pm - FOMC Minutes

7:50 pm - Japan Trade

7:50 pm - Japan Machinery Orders

9:30 pm - Australia Employment

Morning Reading List

Other Data Releases Today

Euro area real GDP grew 0.3% QoQ in Q2 2023 after no growth in Q1 2023. GDP growth slowed to 0.6% YoY, down from 1.1% YOY. Employment growth maintained its pace at 1.5% YoY in Q2 2023, only slightly slower than 1.6% YoY in Q1 2023.

Euro area industrial production grew 0.5% MoM but was still down -1.2% YoY in June. Production fell across the board: capital goods (-0.7% MoM), intermediate goods (-0.9% MoM), non-durables (-1.1% MoM), capital goods (-1.1% MoM).

UK CPI

UK services inflation nudges higher on surging social rents (ING) - The surprise pick-up in UK services inflation was driven by factors that are unlikely to meet the Bank of England's definition of 'persistent'. We expect a September rate hike, but November is still more of a question mark.

Chance for a Bank of England 50bps rate hike in September is back on the table (Saxo Bank) - Stronger growth, accelerating wages, and rising unemployment show that the BOE doesn't have inflation under control and might need to continue to hike, although the British economy is quickly deteriorating. That calls for a more aggressive and faster tightening from the Bank of England, increasing the odds for a 50bps rate hike in September.

US Retail Sales

Retail Sales: Resilience or Madness? (Wells Fargo) - Somehow rising delinquencies, higher consumer financing costs and the erosion of pandemic-era savings comprised the perfect formula for an expectation-crushing 0.7% increase in July retail sales...and for an added flex, the gain comes despite upward revisions to prior monthly data.

Strong consumer keeps US on track for 3% GDP growth (ING) - Retail sales provided another upside data surprise and indicates a 3% annualised GDP growth rate is possible for the third quarter. However, higher consumer borrowing costs, reduced credit availability, the exhausting of pandemic-era savings and the restart of student loan repayments pose major challenges for fourth quarter activity.

Retail sales rise more than expected in July (TD Bank) - U.S. consumers kicked off the third quarter on a strong note with retail sales coming in well above expectations. Though still early yet, sales are currently tracking 4.7% annualized in 2023 Q3 relative to the revised 0.6% posted for Q2. Despite the strong start, looking ahead, we expect consumer spending to slow over the remainder of the year as past rate hikes continue to filter through the economy.

US Retail sales: Q3 US goods consumption is off to a roaring start (CIBC) - Today's release suggests core goods ex autos consumption will be higher than expected in Q3 and is another sign that demand remains firm in the US. We retain our call for a final 25bps Fed hike in September. Tighter monetary policy will continue to slow the labor market which should work to limit retail sales in discretionary categories, in combination with the depletion of pandemic-accumulated excess savings.

Retail sales resilience in July (EY Parthenon) - Retail sales posted a stronger than expected 0.7% gain in July as consumers spent more online, at sports and clothing stores, and on dinner and bar outings. Still, they exercised more discretion on furniture, electronics and cars. Adjusted for inflation, retail sales volumes rose a robust 0.6% indicating that while consumers are increasingly cautious with their outlays amid elevated prices and interest rates, they are not retrenching.

Retail Sales Rose 0.7% in July (First Trust Portfolios) - Consumer spending remained strong in July. Retail sales rose 0.7% for the month, beating consensus expectations, and were revised higher for prior months. The gain in July was powered by nonstore retailers (think internet and mail order) boosted by a record Amazon Prime Day, with an assist from a robust increase at restaurants & bars. The largest declines in July were for autos and furniture & electronics stores. Sales at restaurants & bars, the only look at the service sector we get in this report, rose a whopping 1.4% in July.

US

A softer landing – but still a landing (ABN AMRO) - Moving to a stagnation scenario – Our base case for the US economy no longer foresees a mild recession, but instead a slowdown and a stagnation in output around the turn of the year. The headwinds facing the economy remain very much intact, both from tight monetary policy and the running down of excess savings. As such, we see a slowdown as a question of ‘when’ rather than ‘if’. Even so, we also need to acknowledge the remarkable resilience of the economy over the past year, which points to an underlying strength that we had underestimated.

The IRA and the US’s mineral supply challenge (S&P Global) - To what degree will the massive Inflation Reduction Act (IRA) achieve its goal of accelerating the US energy transition? That hinges on minerals: Will the US be able to secure sufficient supply of the minerals needed for its move toward net zero? An S&P Global analysis suggests there are formidable challenges.

US Inflation – Encouraging, but don’t extrapolate blindly to Australia (NAB) - Recent US CPI prints have shown good progress on disinflation. In this Weekly, we look at where those gains have occurred, and what to be careful of when drawing implications for Australia.

Stagflation could bring a short-term uptrend in the US Dollar (Saxo Bank) - Our latest economic outlook calls for a light stagflation in the US which could complicate the path of the central banks including the Fed. The US dollar has recovered recently on higher US yields and Fitch’s rating downgrade, and a clear downtrend in the greenback may have to wait until the Fed pivots.

Americas CIO View: Exploring other schools of thought: All schools out for summer? (DWS Group) - Despite the highest observed S&P price-to-earnings (P/E) ratio in 20 years, except 2021 when real interest rates were negative, summer brought a rally without S&P EPS growth or lower interest rates. S&P earnings per share (EPS) declined the last few quarters year-over-year (y/y) and Treasury yields climbed 25bp this summer.

Worker Voices Tell Us What the Data Do Not (Patrick Harker, Philadelphia Fed) - Speaking at a webinar, Patrick T. Harker, president and CEO of the Philadelphia Fed, stressed the importance of qualitative data in understanding the labor market. Hosted by Fed Communities, the event focused on the recent Worker Voices report, a national Fed study that engaged job seekers and workers without a four-year degree. “For us as policymakers,” said Harker, “the soft data provided by Worker Voices are equally important as, if not perhaps even more important than, numbers-driven hard data in getting a full understanding of our economic situation.”

Europe

Swedish July inflation review: Back on track (Nordea) - Inflation harmonised with the Riksbank’s forecast in July, in line with our expectations. Core services inflation stabilised.

China

China | Will Chinese economy enter into “Japanization”? (BBVA) - The recent data show that China is going into the coexistence of growth slowdown and deflation. Given China still has enough policy room, we do not think China will enter into "Japanization".

Canada

Canadian home sales drop in July amid BoC Hike (TD Bank) - Higher interest rates are having an impact on the housing market, just as the Bank of Canada intended when it resumed hiking rates in June. That said, the minor dip in sales last month indicates some durability to demand in the face of rising borrowing costs. Notably, conditions in some markets are much firmer than others.

Inflation back above 3% in July, thanks to higher energy prices (TD Bank) - Although headline inflation moving back above to 3% is likely to catch some attention, it is what's going on under the hood that is more concerning for the Bank of Canada. The BoC's median and trim inflation measures continued to make progress in July, but at a glacial pace. Underlying inflation remains a long way from the 2% goal.

Canadian CPI (July): Still a bit hot around the collar (CIBC) - The upside surprise in July inflation wasn't entirely attributable to higher energy prices and food prices, as core categories outside of mortgage interest costs also accelerated, and headline inflation is likely to increase further in August as base effects remain unfavorable. While we would argue for more patience, the BoC is likely on track for a final 25bp hike in September.

Canadian Existing Home Sales (July) — Cool Summer (BMO) - Canadian housing activity is balancing, with recent Bank of Canada rate hikes taking some early-year momentum out of the market. Existing home sales dipped 0.7% in July (seasonally adjusted), but were still up 8.7% from weak year-ago levels when the market was sliding into a correction.

Cdn CPI: Things Just Got Interesting (BMO) - There's no sense sugar coating this one—it is not a good report for the Bank of Canada. While the Bank had anticipated a back-up in headline inflation in their latest forecast, July's result is already at their call for all of Q3 (3.3%), and the August reading is almost certainly set to be even higher.

Argentina

Argentina Presidential Election Scenario Analysis (Wells Fargo) - Toward the end of last week, we laid out our scenarios for Argentina's primary elections (PASO). Heading into the PASO, we believed voters would reject traditional Peronism given poor and deteriorating local economic conditions, and favor a return to market and business-friendly policies. While voters did indeed reject the Peronist coalition, support was directed toward the unorthodox policy platform of Javier Milei rather than the investor preferred Juntos por el Cambio (JxC) coalition.

Real Estate

Builder Confidence Falls on Rising Mortgage Rates (NAHB) - After steadily rising for seven consecutive months, builder confidence retreated in August as rising mortgage rates nearing 7% (per Freddie Mac) and stubbornly high shelter inflation have further eroded housing affordability and put a damper on consumer demand.

Outlook

The Forward View – Global: August 2023 (NAB) - Global inflation continues to trend lower. Our global CPI indicator rose 5.3% yoy in June, its lowest reading since October 2021, and consumer prices in China slipped into deflation in July 2023. While commodity prices have trended higher since the start of June (led by energy), monthly core inflation for the major AEs in June was 0.2% m/m (as was US core CPI in July) pointing to underlying improvement.

Global inflation and growth: what to watch for in the upcoming August PMI surveys (S&P Global) - The global economy continued to lose growth momentum at the start of the second half of 2023, underpinned by waning of service sector growth momentum and a deepening manufacturing downturn. Whether this continues in August and to what extent if so, will be eagerly watched with the upcoming flash PMI releases for major developed economies on August 23rd, followed by worldwide PMI figures at the start of September.

Looking for a way to take advantage of higher interest rates? I recommend SoFi’s high-yield savings account which has a yield of 4.5% (subject to change) and includes FDIC deposit insurance for both its checking and savings accounts just like a traditional bank. Use my referral link to get a sign-up bonus and start earning that rate today. (This is also a great way to support me since I get a bonus too!)

Subscribe to receive Econ Mornings every weekday at 9 am. More economic and finance content on Twitter, Reddit, and my website. You can also see my feed on the PiQSuite platform as a partnered feed.