UK GDP Shows Modest Growth in April, Led by Services Sector

Economic news and commentary for June 14, 2023

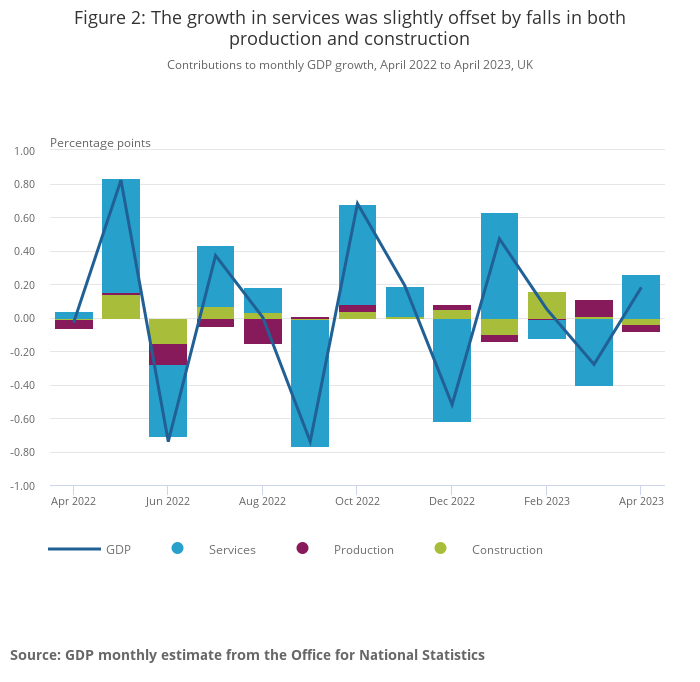

UK GDP, Trade, and Industrial Production

The latest GDP data released by the UK for the month of April indicates a more positive start to Q2 compared to the end of Q1. However, the growth recorded during this period was not particularly strong. UK GDP experienced a 0.2% MoM increase, following a decline of -0.3% MoM in March. Over the three months leading up to April, GDP saw meager growth of just 0.1%.

The services sector played a significant role in driving the monthly growth, expanding by 0.3% MoM. This growth helped to reverse some of the weaknesses observed in March, with 10 out of 14 sectors within the services industry showing expansion. Of particular note was the output of consumer services, which exhibited even stronger growth at 1.0% MoM. This growth was largely driven by a 2.0% MoM increase in food and beverage services activity, making it the largest contributor to the overall expansion of this segment.

In contrast, the production sector performed poorly in April, following a positive end to the first quarter. It experienced a decline of -0.3% MoM, with manufacturing production also falling by -0.3% MoM. Notably, the pharmaceutical (-5.0% MoM) and electronics (-3.8% MoM) industries saw significant contractions during this period. Apart from production, other sectors such as construction and mining & quarrying also experienced negative growth rates. Construction declined by -0.6% MoM, while mining & quarrying saw a larger decline of -1.9% MoM. New construction work specifically fell by -1.0% MoM.

Separate from these sectors (and not considered in monthly GDP calculations), UK trade provided a boost to growth in April, as the deficit decreased by £1.7 billion to reach £16.2 billion. This improvement was driven by a 3.4% MoM increase in exports and a -1.4% MoM decrease in imports. While imports from the EU declined by -3.6% MoM, exports to non-EU economies witnessed a substantial jump of 7.3% MoM, reaching near a 2-year high. The main contribution to the £1.1 billion (7.3%) rise in exports to non-EU countries was a £0.7 billion increase in machinery and transport equipment, led by exports of mechanical machinery to New Zealand and cars to China

Overall, the latest GDP data suggests that the UK economy managed to slightly reverse the weak trend observed at the end of the first quarter. This recovery was primarily driven by the resilient services sector, which offset the weak performance of the production sector—a trend that has been evident in the UK S&P Global PMIs. However, it is worth noting that the growth in the services sector appears to be losing momentum. In the three months leading up to April 2023, the services sector experienced a 0.1% decline compared to the preceding three months up to January 2023, with 8 out of the 14 sub-sectors showing falls. The consumer-facing services segment has slightly offset this decline with a 0.1% increase in that same period. This development is likely to be welcomed by the Bank of England, as it prepares for potential interest rate hikes in order to address high wage growth and persistent inflation in the services sector.

Still to come…

10:00 am (EST) - US Atlanta Fed Business Inflation Expectations

10:30 am - US EIA Petroleum Status Report

2:00 pm - US FOMC Announcement

7:50 pm - Japan Trade & Machinery Orders

9:30 pm - Australia Employment

10:00 pm - China Investment, Industrial Production & Retail Sales

Morning Reading List

Other Data Releases Today

India's Wholesale Price Index fell -0.9% MoM and -3.5% YoY in May, down from 0.9% YoY in April. Fuel & power wholesale prices are down -9.2% YoY which pushed wholesale prices for commodities (-1.8% YoY) & manufactured products (-3.0% YoY) down.

Euro area industrial production increased 1.0% MoM and 0.2% YoY in April. Capital goods production surged 14.7% MoM while durables and non-durables production fell -2.6% MoM and -3.0% MoM respectively.

German wholesale prices fell -1.1% MoM and -2.6% YoY in May, down from -0.5% MoM in April. This is the largest annual decline since July 2020. Mineral oil products are the main cause of the decline, down -31.3% YoY.

US PPI fell -0.3% MoM and was up just 1.1% YoY in May, down from 2.3% YoY in April.

Core PPI: 2.8% YoY (0.0% MoM)

Processed Goods: -7.1% YoY (-1.5% MoM)

Unprocessed Goods: -27.5% YoY (-4.8% MoM)

Services: 3.9% YoY (0.2% MoM)

Euro Area Industrial Production

Eurozone industrial production up in April but with lots of underlying weakness (ING) - The production increase in April underwhelms and leaves a good chance of negative overall production growth in the second quarter. The economy, therefore, remains in a stagnation environment as the second quarter is unlikely to show much of a bounceback in economic activity.

US CPI

US inflation numbers boost chances of a pause in Fed rate hikes (ING) - While US inflation came in broadly in line with expectations, there are signs of softening in some key categories. While housing costs and vehicle prices continue to run hot, the outlook is improving rapidly. This should cement expectations for the Fed to keep rates unchanged tomorrow but the commentary around the decision is likely to remain hawkish.

May CPI: Still Too High, but Better Days Ahead (Wells Fargo) - The consumer price index increased a modest 0.1% in May. Falling energy prices and slow food inflation kept the headline index in check. Excluding food and energy, the core CPI rose a much stronger 0.4%. A big jump in used auto prices and steady inflation for core services propped up the core index. Over the past year, headline CPI is up 4.0%. Although still high, this is the lowest reading since March 2021. The core index has been much slower to come down and is up 5.3% over the past 12 months and 5.0% over the past three months (annualized).

Inflation continues to ease in May, but lingering price gains will keep FOMC vigilant (TD Bank) - May's inflation reading largely met expectations, with both the headline and core measure easing to 4.0% and 5.3%, respectively. That said, non-housing service inflation heated up in May, with price gains led across those spending categories most closely tied to discretionary spending. Goods prices were also higher, though this was largely driven by another sharp gain in used vehicle prices. After stripping out its effects, price growth across all other goods were flat. This is an encouraging sign, as wholesale used vehicle prices have turned lower in recent months, suggesting goods prices will (again) soon become a source of deflation.

US CPI cooling supports Fed inaction tomorrow (CIBC) - May's inflation data showed tame advances in enough key categories to justify a pause from the Fed tomorrow. Although the annual core inflation pace will continue to cool in the summer months, helped by base effects, the ongoing strength in the labor market suggests that 2.0% inflation won't be attainable on a sustained basis, and we could see two final 25bp rate hikes in Q3 from the Fed as a result.

CPI data hums ‘should I stay, or should I go?’ (EY Parthenon) - The latest consumer price inflation data doesn’t change the Fed outlook for a June rate hike skip, but it illustrates the “should I stay, or should I go?” dilemma that the Fed faces when considering further rate increases. Some Fed policymakers will interpret the persistent (and backward-looking) core inflationary pressure and an indication to “go” on tightening, while others with more of a forward-looking policy framework will see justification to “stay.”

Inflation Slows to Lowest Level since March 2021 (NAHB) - Consumer prices in May saw the smallest year-over-year gain since March 2021, mainly driven by lower energy prices. This marked the eleventh consecutive month of deceleration. While this measure aligned with expectations, core inflation remained persistent due to the increase in rent prices. The shelter index (housing inflation) continued to be the largest contributor to both headline and core inflation, accounting for over 60% of the increase in all items excluding food and energy.

U.S. Consumer Price Index (May) — Slower Inflation Readings Continue (BMO) - The CPI increased increase 0.1% in May, in line with market expectations and pulling headline inflation down by 0.9 ppts to 4.0% y/y. This is the slowest since March 2021 and looks very impressive against the 9.1% y/y peak last June. Lower gasoline prices (-5.6%) and subdued food price gains (0.2%) offset much of the expected 0.4% increase in the core index.

The Consumer Price Index (CPI) Rose 0.1% in May (First Trust Portfolios) - Today’s CPI report showed progress in the battle against inflation, but the fight is not over. Headline inflation moderated in May, coming in-line with consensus expectations, while the year-over-year comparison dropped to 4.0% from 4.9% in April. Prices were once again held down by the volatile energy sector, which fell 3.6% in May. Stripping out energy and its often-volatile counterpart – food prices (+0.2% in May) – “core” prices rose 0.4%, also matching consensus expectations.

US NFIB Small Business

Small Business Optimism Index Ekes out Modest Improvement in May as Inflation Concerns Persist (TD Bank) - NFIB's Small Business Optimism Index rose 0.4 points to 89.4, coming in above market expectations for a moderate decline to 88.5. This is the 17th consecutive month that the index is below the 49-year average of 98.

Small Business Optimism Improves in May: But Firms are Still Sour on the Outlook Amid Inflation Concerns (Wells Fargo) - The NFIB Small Business Optimism Index ticked up from 89.0 in April to 89.4 in May, besting expectations of a decline. May's bump in optimism was the first improvement in three months.

US

US | Fed to skip raising the fed funds rate (BBVA) - The inter-meeting period was marked by a significant division of opinions among Fed officials: some voting members conveyed a hawkish stance in favor of further hikes, while some others leaned toward a momentary pause in order to carefully assess the effects of the cumulative tightening.

Europe

Euro Area Macro Monitor - Can the May disinflationary impulse be trusted? (Danske Bank) - The quite benign Q1 GDP data was revised to the downside during May hence the euro area technically entered a recession in Q1 2023. However, we argue that this should not be interpreted that gloomy given a strong service sector in conjunction with very tight labour markets.

Spain Economic Outlook. June 2023 (BBVA) - Growth in 2023 is revised upwards to 2.4% and downwards in 2024 to 2.1%. The improvement is explained by statistical revisions and export developments. There are doubts about the sustainability of the pace of expansion and job creation in 2024, in line with the uncertainty in the global economy.

Directional Economics EMEA: Making the best of it (ING) - After facing three years of headwinds to economic growth, the economies of Central and Eastern Europe might just be on the verge of an upturn. As we move into the second half of the year, our team sees the region ‘making the best' of an admittedly still challenging environment.

China

China Economic Update – June 2023 (NAB) - Chinese trade data have exhibited some unusual patterns in recent months – including a sharp jump in export volumes in March, at a time demand for goods in most advanced economies has been slowing. Beyond this short-term spike, there has also been a noticeable decline in the share of China’s exports being delivered to its major trading partners since early 2022 – although it is too early to know if this represents a short-term anomaly or a permanent shift in the direction of trade.

Australia

NAB Economics Monthly Data Insights – May 2023 (NAB) - Our monthly transaction data showed a small rise in spending in May (in seasonally adjusted terms), driven by discretionary spending.

Mexico

Mexico Economic Outlook. June 2023 (BBVA) - Upward revision in our 2023 growth estimate to 2.4% (1.4% previously); the resilience of domestic demand drives growth this year. We anticipate a slowdown in 2H23 due to lower external demand, with a carry-over effect on 2024.

Politics

The G7's message of unity (S&P Global) - Over May 19-21, leaders of the Group of Seven (G7) came together in Hiroshima, Japan, conveying a message of unity in the midst of broader volatility, and addressing a host of issues including the Russia-Ukraine war, G7-Indo-Pacific relations, economic resilience and energy transition.

Research

Micro- and Macroeconomic Impacts of a Place-Based Industrial Policy (Philadelphia Fed) - We investigate the impact of a set of place-based subsidies introduced in Turkey in 2012. Using firm-level balance-sheet data along with data on the domestic production network, we first assess the policy’s direct and indirect impacts. We find an increase in economic activity in industry-province pairs that were the focus of the subsidy program, and positive spillovers to the suppliers and customers of subsidized firms.

Green

Biodiversity loss part II: portfolio impacts and abatement measures (Allianz) - Portfolios most exposed to equities and the agriculture and food services sectors feel the pinch of biodiversity loss. The results of our pilot study on pollination-service loss (PSL) allow for quantitative estimates of financial institutions’ portfolio exposure to biodiversity-related risk. Applying the shocks to a representative portfolio of an average German life insurer leads to rather modest impacts: The overall portfolio loss comes out at 0.17%, mainly because of low exposure to the sectors that will be hit the hardest (agriculture and food services) and to equities in general. In contrast, portfolios with larger equity shares (e.g. US insurers) would likely experience larger losses overall.

Subscribe to receive Econ Mornings every weekday at 9 am. More economic and finance content on Twitter, Reddit, and my website.