UK Inflation August Update: A Precursor to the Bank of England's Announcement

Economic news and commentary for September 20, 2023

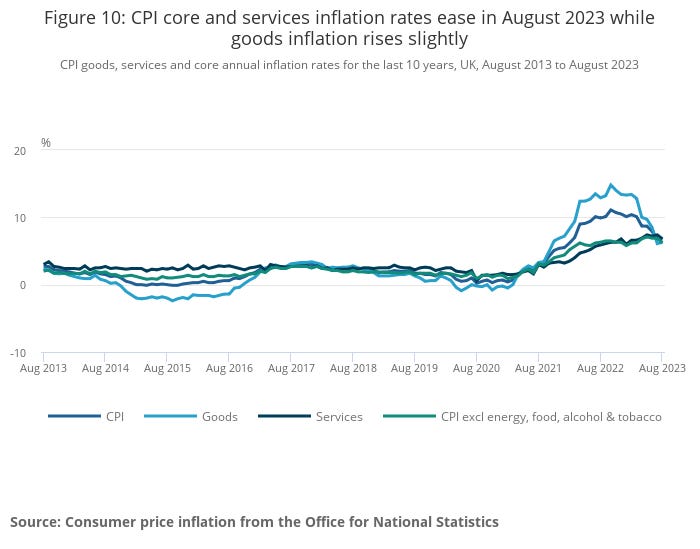

UK CPI & PPI

The UK's inflation data for August, released just before a highly anticipated Bank of England announcement, will set the stage for a huge decision of whether to pause or hike once again. The Consumer Price Index (CPI) for the UK rose by 0.3% MoM, reaching an annual rate of 6.7% YoY, a slight dip from July's 6.8%. This marks the lowest inflation rate since February 2022, a notable decline from the peak of 11.1% YoY in October 2022. The primary driver of this month's inflation was energy, mirroring trends observed in other countries. Despite a 1.7% MoM surge in the UK's energy CPI, it remains down by -3.2% YoY. Meanwhile, food inflation, which previously peaked at 14.8% YoY, has moderated, registering a 0.5% MoM increase and settling at 12.6% YoY. This reduction was influenced by a 1.5% MoM rise in alcohol and beverage prices, while non-processed and seasonal food prices both experienced a decline.

The surprise today was in the core CPI, which saw a modest 0.2% MoM increase, bringing the annual rate down from 6.9% YoY to 6.2% YoY. This deceleration was largely attributed to the services sector, where prices remained unchanged for the month, resulting in a YoY rate of 6.8%. Several service segments, including travel & transport (-0.2% MoM), package holidays & accommodation (-1.0% MoM), and non-catering recreational & personal services (-0.8% MoM), reported deflationary trends. Consequently, the combined impact of the recreation & culture and restaurants & hotels segments led to a 0.24 ppt reduction in the annual CPI rate, though this was almost entirely offset by the influence of energy prices on the transport index. Goods inflation, influenced heavily by energy and food prices, rose by 0.5% MoM, reaching 6.3% YoY. Some segments, such as household goods (0.2% MoM) and non-energy industrial goods (0.3% MoM), showed signs of disinflation. Recreational goods prices actually declined (-0.2% MoM).

Producer Price Index (PPI) movements in the UK underscored the volatility of energy prices. Both input and output producer prices witnessed an uptick, largely due to surging crude oil input prices (12.1% MoM) and petroleum production prices (7.7% MoM). Notably, of the output PPI segments only petroleum products showed an upward contribution to the change in the annual inflation rate, at 1.42 ppts. This upwards contribution was greater in magnitude than the sum of the contributions of the other product groups.

The Bank of England, which has been a bit more hawkish than its other developed market central bank peers, has been closely monitoring wage and core CPI pressures, which have been more persistent in the UK than elsewhere. This latest report provides one of the first pieces of tangible evidence of inflation easing, primarily driven by a slowdown in service price growth and the largest deceleration in core CPI since the pandemic ended. However, most of disinflation was seen in recreation and travel categories and in just this one month, so it might be risky to change the perspective on inflation based on such a short-term, limited trend. On the other hand, there are signals from the labor market that the demand for hiring is cooling with vacancies falling and the unemployment rate starting to tick up. With that in mind, the Bank of England should be able to get away with a pause, and a clear guidance that it will raise rates in the future if progress on inflation is reversed.

Still to come…

10:30 am (EST) - US EIA Petroleum Status Report

2:00 pm - FOMC Announcement

Morning Reading List

Other Data Releases Today

Japan's trade deficit widened in August with exports dropping -8.4% MoM and imports rising 1.5% MoM. Significant declines were seen in key export sectors like machinery (-13.5% MoM) and manufactured goods (-6.0% MoM).

Australia's Westpac Leading Index grew slightly to -0.50% in August, down from -0.56% in July. The index has been negative since August 2022. The growth outlook for the next 3-9 months remains "poor".

German PPI edged up 0.3% MoM but was still down -12.6% YoY in August. This is the largest YoY decline on record (August 2022 PPI YoY was the largest on record). Excluding energy, German PPI fell -0.4% MoM but was up 1.2% YoY.

UK Inflation

UK inflation surprise boosts chances of Bank of England pause (ING) - We're still tempted to say the Bank of England will hike rates tomorrow, and some of the downside surprise in services inflation is down to volatile travel categories. But it's a close call, and both wage and inflation data suggest the end of the current tightening cycle is very close to its conclusion.

US Housing Starts

U.S. housing starts fell in August as interest rates pushed higher (TD Bank) - Homebuilding activity faltered in August as higher mortgage rates weighed on the demand for new homes. The decline was centered in the multi-family segment which is down 41.6% year-on-year (y/y) and roughly 20% below the pre-pandemic average for the month of August. In contrast, the single-family segment is up 2.4% y/y and roughly 4.4% above the pre-pandemic average for August. The multi-family sector has struggled under higher interest rates and slower price growth in rental rates, but the 15.8% uptick in permitting activity in August suggests the sector may improve in the coming months.

Housing Starts Declined in August: Higher Interest Rates Intensify the Headwinds for Residential Construction (Wells Fargo) - Total housing starts dropped 11.3% to a 1.28 million-unit pace in August. The monthly decline was broad-based, with single-family and multifamily starts falling by 4.3% and 26.3%, respectively. The surprising pull-back in starts stands in contrast to a strong gain in both single-family and multifamily building permits.

Housing Starts Plunge In August (BMO) - The long stretch of housing market weakness is likely to continue over the near term amid high mortgage rates and challenging affordability that are limiting home demand.

Housing Starts Lower on Rising Mortgage Rates (NAHB) - Higher mortgage rates averaging above 7% put a damper on single-family production in August, as builders also continue to face supply-side challenges in the form of elevated construction costs, a lack of skilled labor and a shortage of buildable lots.

Housing Starts Declined 11.3% in August (First Trust Portfolios) - Housing starts posted the largest monthly decline in over a year in August, falling to the slowest pace since the worst of the COVID pandemic in 2020. However, we don’t see this as a sign of persistent weakness ahead in home building. While both single-family and multi-unit projects contributed to the decline, a massive 26.3% drop in the

multi-unit category was largely responsible for today’s bad headline number.

Canada CPI

Inflation mercury spikes to 4% in August (TD Bank) - Headline inflation moving back up to 4% on higher energy prices would likely be tolerated by the Bank of Canada. But, core inflation measures heating back up to 4% y/y, and 4.5% on a three month annualized basis is going to ring some alarm bells at the Bank.

Canadian CPI (Aug): Not just a gasoline-driven acceleration (CIBC) - Canadian inflation accelerated by more than expected in August, and even though higher prices at the pumps were a big factor behind the move they were not the only one. Core inflationary pressures remained stronger than the Bank of Canada would like to see, although we still suspect that evidence of a slowing economy and rising unemployment rate will give policymakers enough comfort that inflation will ease ahead without the need for further interest rate increases.

Canadian CPI: A Little Bit Louder, A Little Bit Worse (BMO) - Things just got a lot more interesting for the Bank of Canada, and most definitely not in a good way. We all knew that the extended back-up in gasoline prices was going to be a headache for headline CPI and inflation expectations, but the inconvenient truth is that core has suddenly heated up as well. We will note that even excluding mortgage interest costs, prices are now up 3.2% y/y, or above the target band. There's still lots of data to go before the Bank next decides on rates (October 25), including another swing at the CPI. Unfortunately, we suspect that with oil firing higher and core inflamed again, that report will be no better than today's—second verse, same as the first, a little bit louder and likely a little bit worse.

US

US | Fed’s debate on how high should rates go is likely to end soon (BBVA) - The strength of the economy and the job market will refrain the Fed from ruling out the chance of an additional rate hike this year. For now, the FOMC will skip and leave its options open.

Cooling labour market to drive Fed pause; BoE to hike once more (ABN AMRO) - Labour markets are cooling in both the US and the UK, but we expect still-elevated wage growth in the UK to trigger one last BoE hike, while in the US, we think rate hikes have come to an end.

Government shutdown: What are the risks from a government shutdown? (EY Parthenon) - There is a pressing obligation for Congress to pass legislation to fund the government in fiscal year 2024 and avoid a government shutdown before the September 30 deadline, but the window is rapidly closing. Such a shutdown could leave a visible mark on the economy.

US Weekly Economic Commentary: Growth above trend as FOMC meets (S&P Global) - On balance, good news arrived last week, suggesting that the recent slowing in price inflation remains intact and real growth continues at a solid, above-trend pace. If growth were not "too strong," we would characterize this as a Goldilocks outcome we'd like to see continue.

Economic Long COVID (Northern Trust) - Chief Economist Carl Tannenbaum discusses the many ways the pandemic is still with us.

Europe

Spain | Analysis of national tourist flows in real time between May and August of 2023 (BBVA) - According to BBVA card spending data, the summer months have been characterized by a slight improvement in tourist spending compared to the beginning of the year, driven by the good behavior of consumption by Spaniards and despite the sluggishness of tourism by of foreigners.

Polish industrial production still weak, but with first green shoots (ING) - Polish industrial production remains in contraction (2.0% year-on-year drop), but there are some positive signs of change (minor growth in seasonally-adjusted terms, solid growth in some export-oriented sectors and capital goods production). But real GDP is set to drop again in the third quarter in YoY terms.

Polish labour market tightness persists as unemployment hits record low (ING) - While growth for employment in enterprises ceased, the unemployment rate remains at a record low, and wages are expanding at a double-digit rate. Labour market conditions remain tight and pro-inflationary. A gradual recovery in real wages should allow for a rebound in household consumption in the fourth quarter of this year.

China

China/Hong Kong Market Pulse: Stronger Activity Data, Regulatory Easing Amid Shadow Banking and Local Government Debt Risks (Saxo Bank) - The PBoC is working to stimulate economic growth by implementing an RRR cut. Positive growth is evident in industrial production and retail sales. However, it's important to note that shadow banking and local government debt continue to present persistent risks. Despite these challenges, the market offers opportunities due to undervalued assets and low institutional investor allocation, especially with some signs of an economic cyclical upturn.

Emerging Markets

Countries Can Tap Tax Potential to Finance Development Goals (IMF) - Emerging markets and developing economies need $3 trillion annually through 2030 to finance their development goals and the climate transition. That amounts to about 7 percent of these countries’ combined 2022 gross domestic product and poses a formidable challenge, particularly for low-income countries.

Real Estate

Commercial and Multifamily Mortgage Debt Outstanding Increased by $37.7 Billion in Second-Quarter 2023 (Mortgage Bankers Association) - The level of commercial/multifamily mortgage debt outstanding increased by $37.7 billion (0.8 percent) in the second quarter of 2023, according to the Mortgage Bankers Association’s (MBA) latest Commercial/Multifamily Mortgage Debt Outstanding quarterly report.

Central Banks

Central banks: How your views compare to ours (ING) - We ran a series of live polls at our recent Economics Live webinar earlier this week, and this is how the views of our listeners compare to our own.

Commodities

Oil’s rally has more room to run (ING) - The oil market has seen quite the move in recent months. ICE Brent is up more than 25% so far this quarter and broke above $95/bbl briefly. Tightening fundamentals support this move and we are likely to see Brent breaking above $100/bbl in the near term. However, we don’t think such a move will be sustainable.

Research

Preventive vs. Curative Medicine: A Macroeconomic Analysis of Health Care over the Life Cycle (St Louis Fed) - This paper studies differences in health care usage and health outcomes between low- and high-income individuals. Using data from the Medical Expenditure Panel Survey (MEPS) I find that early in life the rich spend significantly more on health care, whereas from midway through life until very old age the medical spending of the poor dramatically exceeds that of the rich. In addition, low-income individuals are less likely to incur any medical expenditures in a given year, yet, when they do incur medical expenditures, the amounts are more likely to be extreme.

I've Got 99 Problems But a Bill Ain't One: Hospital Billing Caps and Financial Distress in California (Philadelphia Fed) - We examine the financial consequences of the 2007 California Fair Pricing Law (FPL), a law that places a price ceiling on hospital bills for uninsured and financially vulnerable individuals. Using difference-in-differences models, we exploit cross-sectional variation in exposure to the law to estimate the causal effects of the FPL on different measures of financial distress. We find that the law reduces the medical and non-medical debt burden of individuals targeted by the law, with the likelihood of incurring non-medical debt in collections declining by 14.5 percent and the number of non-medical collections declining by 31 percent.

Green

The greening of the iPhone supply chain (S&P Global) - Apple Inc.'s iPhone and Watch updates this year come with important supply chain considerations, including the use of recycled materials, plans to shift transport modes and the use of new processors.

Looking for a way to take advantage of higher interest rates? I recommend SoFi’s high-yield savings account which has a yield of 4.5% (subject to change) and includes FDIC deposit insurance for both its checking and savings accounts just like a traditional bank. Use my referral link to get a sign-up bonus and start earning that rate today. (This is also a great way to support me since I get a bonus too!)

Subscribe to receive Econ Mornings every weekday at 9 am. More economic and finance content on Twitter, Reddit, and my website. You can also see my feed on the PiQSuite platform as a partnered feed.