US Consumer Prices Surge in August Driven by Energy Costs

Economic news and commentary for September 13, 2023

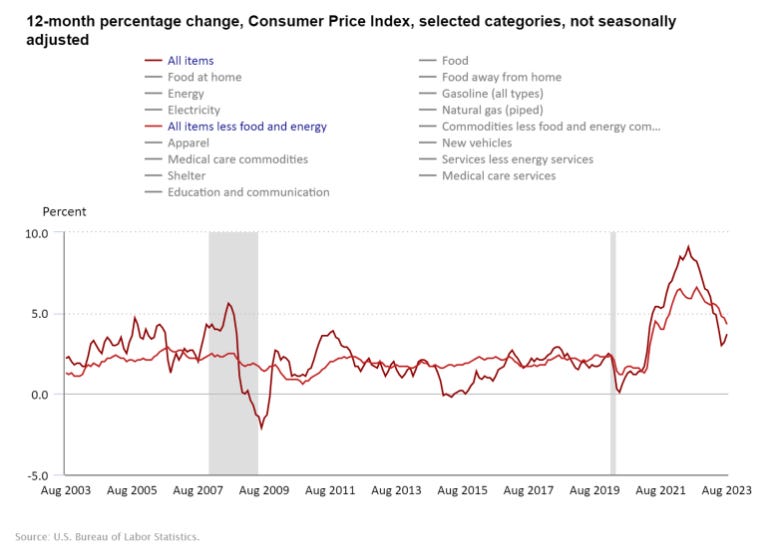

US CPI

In August, the US witnessed a significant uptick in consumer prices, marking the fastest monthly growth since June 2022. The Consumer Price Index (CPI) rose by 0.6% MoM and 3.7% YoY, a noticeable acceleration from the 3.2% YoY recorded in July.

A primary driver behind this surge was the energy index, which reversed its declining trend observed in Q2 2023. Energy prices soared by 5.6% MoM. Breaking it down, the gas index witnessed a substantial jump of 10.6% MoM. In contrast, electricity and natural gas indexes saw marginal increases, with rates of 0.2% MoM and 0.1% MoM, respectively. Fuel oil prices also experienced a significant rise, increasing by 9.1% MoM. On the food front, inflation continued its trend of modest gains, registering a growth of just 0.2% MoM. Both grocery prices and food away from home prices reflected this slow pace, with increments of 0.2% MoM and 0.3% MoM, respectively.

While the headline CPI showed robust growth, the core CPI (ex-food and energy) recorded a more subdued monthly gain of 0.3% MoM. Goods inflation, excluding energy, remained particularly low, with prices declining by -0.1% MoM. This marked the third consecutive month of decline. A significant contributor to this drop was the used car and vehicle index, which decreased by -1.2% MoM. Other indexes in this segment presented a mix of muted gains or slight declines. Services CPI saw an increase of 0.4% MoM, but its annual pace decelerated by 0.2 percentage points, settling at 5.9% YoY. The shelter index, a consistent contributor to the core CPI's monthly gain, rose by only 0.3% MoM, marking its smallest gain this year.

There does seem to be a lot of noise in CPI data with many different segments seeing mean reversions and just in general volatile swings. These are often ignored by the Fed which is why the special “Supercore” aggregate can be important to look at. The Supercore CPI, which excludes food, shelter, energy, and used cars, grew by 0.4% MoM and 3.2% YoY in August. For comparison, in July, this aggregate was flat MoM and up 3.4% YoY. Through all the noise, it looks like the trend of disinflation is being maintained. The significant downtrend in the monthly paces of core CPI growth is another strong indicator of this. Over the last three months, it has grown at about 0.23% MoM which is an annual rate of just under 2.8% YoY.

The Fed will be looking through the volatility in its next September meeting. The core messages of disinflation should shine through to them, but that may not be enough to keep them from hiking one last time. Key employment indicators have slowed, which will also be encouraging in the fight against inflation, but many FOMC members have already indicated their preference for one more 25 basis point increase in the Fed funds rate. It will be a close call, however, as there are many reasons to maintain the pause.

Still to come…

10:00 am (EST) - US Atlanta Fed Business Inflation Expectations

10:30 am - US EIA Petroleum Status Report

7:50 pm - Japan Machinery Orders

9:30 pm - Australia Employment

Morning Reading List

Other Data Releases Today

Japan's PPI in August rose 0.3% MoM and 3.2% YoY, with export prices seeing the largest MoM gain since September 2022 at 1.9%. Petroleum & coal product prices, up 5.2% MoM and 7.5% YoY, indicate rising energy costs might drive inflation in Q3.

UK GDP fell -0.5% MoM in July after a strong 0.5% MoM increase in June. Services output fell by -0.5% MoM making a -0.4 ppt contribution to the GDP decline. Industrial production fell -0.7% MoM but made a smaller negative contribution of -0.1 ppt.

The contraction in UK industrial production of -0.7% MoM was substantial in July and partially reversed the strong 1.8% MoM growth in June. Manufacturing production fell -0.8% MoM and 9/13 subsectors contracted.

The UK trade balance increased £0.5 bil to -£15.5 bil with exports up 0.8% MoM and imports down -0.4% MoM in July. The total trade in goods and services deficit widened by £1.2 bil to £18.8 bil in the 3 months to July 2023.

Italian employment grew 0.6% QoQ and 1.7% YoY in Q2 2023. The unemployment rate fell further, down -0.3 ppts to 7.6% with the total number of unemployed down -3.2% QoQ. Gross wages and salaries increased 0.3% QoQ and 2.1% YoY in Q3.

Euro area industrial production dropped -1.1% MoM and -2.2% YoY in July. Sharp declines came in capital goods and durables production. Capital goods fell -2.7% MoM but are up 0.4% YoY, while durable goods decreased -2.2% MoM and -6.7% YoY.

UK GDP

UK economic output falls further than expected in July (ING) - The monthly GDP numbers have been highly volatile, but we do expect slower growth over coming months as the cooler jobs market and higher rates continue to bite.

US NFIB

Small Business Optimism Index Falls in August (TD Bank) - NFIB's Small Business Optimism Index fell 0.6 points to 91.3 in August, coming in below market expectations for a decline to 91.5. After three consecutive months of improvement, August pared back some of the recent gains, although the index remains higher than it was during the first half of the year.

Small Business Optimism Falls Back in August (Wells Fargo) - After three straight months of improvement, the NFIB Small Business Optimism Index slipped to 91.3 in August. Dimmer sales prospects and a weaker outlook for business conditions seemed to drive August’s dip, solidifying the index’s 20-month streak below its longer-term historical average. Although this outturn may seem bleak, August’s survey was not all bad news. Small business owners echoed recent trends in national data which reveal that the labor market is finding better balance, supporting our expectation that the Fed is done hiking rates. Yet, plans to raise prices perked up in August, suggesting that the ride back to 2% inflation will be bumpy and monetary policy will likely remain restrictive for some time.

US

Income, Poverty and Health Insurance Coverage in the United States: 2022 (Census Bureau) - The U.S. Census Bureau announced today that real median household income in 2022 fell in comparison to 2021. The official poverty rate of 11.5% was not statistically different between 2021 and 2022. The Supplemental Poverty Measure (SPM) rate in 2022 was 12.4%, an increase of 4.6 percentage points from 2021. This is the first increase in the overall SPM poverty rate since 2010. Meanwhile, 92.1% of the U.S. population had health insurance coverage for all or part of 2022 (compared to 91.7% in 2021). An estimated 25.9 million or 7.9% of people did not have health insurance at any point during 2022, according to the 2023 Current Population Survey Annual Social and Economic Supplement (CPS ASEC). That compares to 27.2 million or 8.3% of people who did not have health insurance at any point during 2021.

Revolving Credit Growth Reaccelerates in July (NAHB) - Consumer credit outstanding growth slowed to 2.5% in July, down from 3.4% in July (SAAR) according to the Federal Reserve’s latest G.19 Consumer Credit report. Revolving credit growth reaccelerated to 9.2% in July, potentially reflecting strong consumer sentiment and job security in a tight—albeit cooling—labor market. In contrast, nonrevolving consumer debt outstanding inched up just 0.2% over the month.

Macro/FX Watch: EURCAD in focus with gains in oil and ECB meeting on the radar (Saxo Bank) - The upswing in oil prices made CAD the G10 outperformer in yesterday’s session. USDCAD has room on the downside after the recent run higher but EUR and JPY have more to lose with oil prices rising which brings EURCAD into focus. Also, bets for an ECB rate hike have picked up after a recent Reuters report suggesting inflation forecasts may be adjusted higher, but boost to EUR could remain limited with stagflation concerns rising.

Europe

Fixed-income: A hawkish pause from ECB and attractive risk-reward in bonds (Saxo Bank) - In today's fixed-income focused podcast, we preview the ECB rate decision on Thursday on the back of a recent stagflation outlook from the EU Commission making the policy decision a difficult one. We argue for a hawkish pause with the potential move by the ECB to stop reinvestments into the PEPP facility. Based on a slowing economy and stagflation light outlook we go through why both European and US sovereign bonds have an attractive risk-reward ratio, with Peter Garnry and Althea Spinozzi.

Swedish Labour Market: Less demand in August (Nordea) - Unemployment rose to 6.3% in August according to the SPES monthly numbers (seasonally adjusted). The number of newly registered unemployed increased at a faster pace than previous months but remained well below its historical average.

Higher-than-expected Romanian inflation is not as bad as it looks (ING) - At 9.4%, August inflation came in higher than expected but can be largely blamed on one item: drug prices. These increased by a whopping 20.8% versus the previous month. On the bright side, core inflation dropped by 1.1pp versus July, to 12.1%, and looks on track to reach single digits this year.

Solid contraction in the Dutch manufacturing sector amid a technical recession for the wider economy (S&P Global) - The Netherlands followed its neighbour, Germany, into a technical recession in the second quarter of 2023, with GDP shrinking by 0.3%, as per the initial estimate published by Statistics Netherlands last month. This contraction comes on the heels of a 0.4% quarterly decline in the first quarter of the year and marks the Dutch economy's first recession, albeit a mild one, since the initial onset of the pandemic.

Canada

Too Much Money Can Exacerbate Inflation (TD Bank) - There was a time not too long ago when money supply was central to economists' expectations for inflation. While a long-term relationship between the two variables has never been in doubt, monetary aggregates have done little to explain short-term movements in inflation over the past several decades.

Wait until next year (CIBC) - It’s not just the catchphrase for fans of my hometown Toronto Maple Leafs; “wait until next year” is the message for investors and central bankers that have been looking for signs that higher interest rates are going to bring inflation back to target. Yes, price increases have decelerated sharply, but as we anticipated a year ago, that reflects the fact that so much of the earlier spike wasn’t attributable to overheated demand. Improvements in supply chains, and slowdowns in China and Europe, are helping to cool global price pressures, as captured in less heated markets for most commodities, shipping costs, and goods prices.

Trade

World Trade Report 2023: Re-globalization for a secure, inclusive and sustainable future (WTO) - The 2023 World Trade Report evaluates how re-globalization – integrating more people, economies and pressing issues into world trade – can provide solutions to global challenges, and assesses the risks of trade fragmentation.

Real Estate

Commercial Real Estate Chartbook: A Tale of Two Cities (Wells Fargo) - It was the best of times, it was the worst of times. Economic growth has remained surprisingly resilient to the Federal Reserve's interest rate hiking cycle, standing in stark contrast to the commercial real estate market. As we recently published in our economic outlook for September, a short and shallow recession in the first half of 2024 remains our base case. That said, the odds of a soft landing have increased alongside a remarkably sturdy labor market, which has cooled in recent months but has shown little signs of contracting. Sturdiness in the labor market appears to be supporting income growth, fostering strength in consumer spending and bolstering overall economic growth.

Household Real Estate Value Jumps in the Second Quarter (NAHB) - The second quarter of 2023 release of the Z.1 Financial Accounts of the United States indicates that the market value of households’ real estate assets increased over the quarter. Low existing for-sale inventory helped to increase real estate value after falling for three consecutive quarters.

Debt

Market Reforms Can Stabilize Debt and Foster Growth in Developing Countries (IMF) - The global economy has experienced multiple shocks in the past three years. Emerging markets and developing economies not only need to reignite growth and secure a full recovery, but they also must manage rising debt and other policy considerations.

Looking for a way to take advantage of higher interest rates? I recommend SoFi’s high-yield savings account which has a yield of 4.5% (subject to change) and includes FDIC deposit insurance for both its checking and savings accounts just like a traditional bank. Use my referral link to get a sign-up bonus and start earning that rate today. (This is also a great way to support me since I get a bonus too!)

Subscribe to receive Econ Mornings every weekday at 9 am. More economic and finance content on Twitter, Reddit, and my website. You can also see my feed on the PiQSuite platform as a partnered feed.