US Wage and Services Inflation Resist Down Trend, Euro Area GDP Barely Grows

Economic news and commentary for April 28, 2023

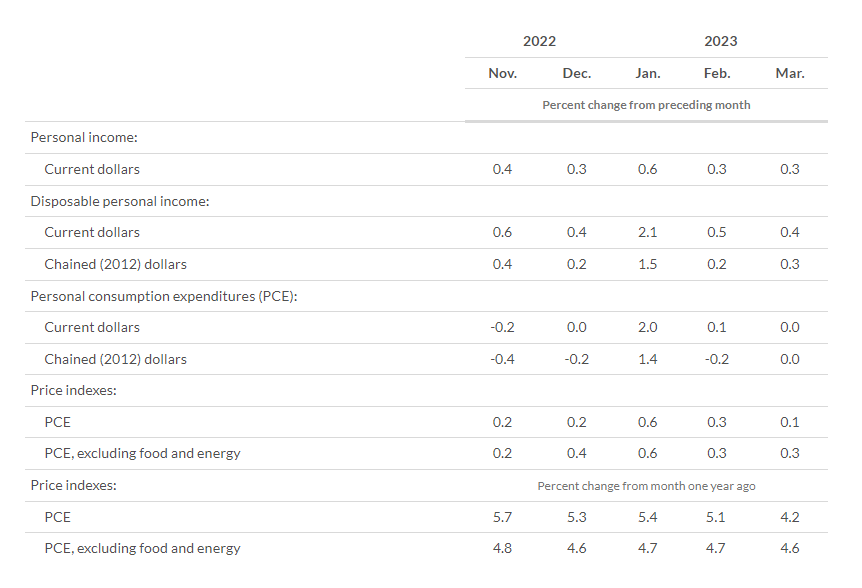

US Employment Cost Index, Personal Income & Consumption

In yesterday’s US GDP release, we saw a strong consumer carry economic growth in the first quarter of the year, but today, monthly consumption data points to a different short-term trend. In March, disposable personal income grew 0.4% MoM, and personal consumption was unchanged. Both of these data points were the weakest of the three months in the quarter. The vitality in yesterday’s PCE number was a result of outsized strength in January where disposable income and personal consumption jumped 2.1% MoM and 2.0% MoM, respectively. In March, things have mostly slowed to a stop. In this case, it was a decline in goods consumption which fell -0.6% MoM, extending losses of -0.2% MoM in February, that offset an increase of 0.4% MoM in services spending and caused the stagnation

The weakness in consumption has lead to further softness in inflation. The headline PCE price index edged up just 0.1% MoM and 4.2% YoY, down from the previous reading of 5.1% YoY. Declines in energy prices helped to push the headline annual inflation number below core inflation as we have seen in CPI readings. The core PCE price index grew 0.3% MoM and 4.6% YoY and was mostly stable from the previous 4.7% YoY rate. Another similarity with the CPI is the goods and services breakdown where goods deflation is actively occurring (-0.2% MoM and 1.6% YoY, down from 3.6% YoY) while services prices are resisting a downtrend (0.2% MoM and 5.5% YoY, down from 5.8% YoY). Services PCE inflation has bounced around between 5.3% YoY and 5.8% YoY for the last seven months now.

As Federal Reserve officials have alluded to, sticky wage growth is feeding through to service providers and causing them to be resistant to reducing selling prices. We also got an update on wage growth today in the Q1 2023 Employment Cost Index release. Total compensation grew 1.2% QoQ in Q1 which puts the annual increase at 4.8% YoY, slightly lower than the 5.1% YoY in Q4 2022. However, the wage component of compensation slowed less. Both private and public workers saw wage growth of 5.0% YoY in Q1 2023, only down -0.1 ppts from the previous period, and private workers saw wage growth of 5.1% YoY, unchanged from previously. Both of these reports (ECI and consumption & outlays) suggest that there hasn’t been substantial progress in keeping both services and wage inflation down. The Fed has no reason to move away from hiking in May.

Euro Area GDP

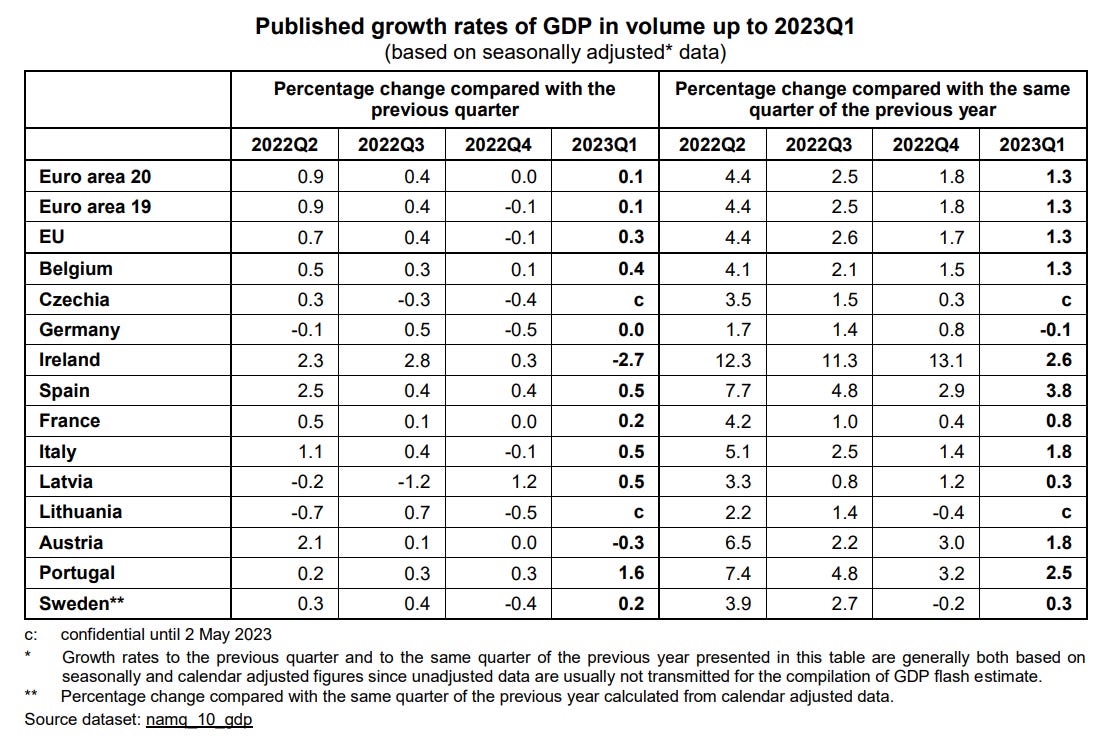

Europe eeks out a quarter of slight growth after stagnating at the end of 2022. In the advanced report, euro area GDP edged up 0.1% QoQ after a 0.0% QoQ change in Q4 2022. In terms of annual comparisons, GDP is now up 1.3% YoY which is a downshift from the 1.8% YoY pace in Q4 2022 and slower than every quarter last year. Despite sluggish growth, the euro area has for the most part avoided contractions in economic activity. Year-over-year growth rates were positive for all reporting countries in the region except for Germany which was only down a slight -0.1% YoY. The monthly growth rates followed a similar trend with only two countries experiencing a deterioration in GDP in Q1 2023, Austria down -0.3% QoQ and Ireland down -2.7% QoQ. The major European economies lead the region with slight growth, Spain (0.5% QoQ), Italy (0.5% QoQ), and France (0.2% QoQ), with the exception being Germany which saw no growth.

Overall, the results confirm that the euro area avoided a recession over the last two quarters when industry data (PMIs, industrial production) pointed to moderate contractions in manufacturing activity. We have the services sector to thank for that. Activity remains stable and in some cases increasing for services firms as strong incomes support consumers in the short term. Strength in this segment of the economy is enough to keep the ECB’s foot on the gas when it comes to rate hikes as inflation remains too high. Based on the few April inflation releases this morning, (German CPI inflation down just -0.2 ppts to 7.2% YoY and French CPI inflation up 0.2 ppts to 5.9% YoY), that probably won’t change before May. Thus, after two or three more increases in the policy rate, it should be expected that the euro area will enter into a recession.

Still to come…

9:45 am (EST) - US Chicago PMI

10:00 am - US Consumer Sentiment

Morning Reading List

Other Data Releases Today

Japan

Japan's unemployment rate increased 0.2 ppts to 2.8% in March. The unemployment rate for 25-35 yr old increased the most (+0.7 ppts). The labor force increased 37,000 or 0.5% MoM with 17,000 (0.3% MoM) finding employment and 15,000 (8.3% MoM) remaining unemployed.

Japan's industrial production grew 0.8% MoM in March and was down -0.7% YoY. Shipments increased just 0.4% MoM. Production is expected to have increased 4.1% MoM in April, and the forecast for May is at -2.0% MoM.

Japanese retail sales increased 0.6% MoM in March and was up 7.2% YoY. For the quarter, sales grew 2.6% QoQ. Good sales were up 5.5% YoY (down from 5.7% YoY), and services sales were up 15.4% YoY (down from 17.2% YoY).

The Bank of Japan holds its policy rates, yield curve control, and asset purchases unchanged. The BoJ says it will continue easing policy until CPI less fresh food "exceeds 2% and stays above the target in a stable manner.”

Australia

Australia's PPI grew 1.0% QoQ and 5.2% YoY in March, down from 5.8% YoY in February. Electricity & gas supply was the reason for the quarterly increase, up 13.3% QoQ. Furniture (-5.8% QoQ) & electronics (-3.5% QoQ) producer prices both declined.

France

France's GDP grew 0.2% QoQ in Q1 2023, up from 0.0% QoQ in Q2 2023. Consumption was flat, and imports fell -0.6% QoQ as demand slowed. Capital formation edged down -0.2% QoQ with the goods (-0.5% QoQ) decline offsetting services (0.4% QoQ).

France's CPI increased 0.6% MoM and 5.9% YoY in April, up from 5.7% YoY in March.

Food: 14.9% YoY (Mar 15.9% YoY)

Energy: 7.0% YoY (Mar 4.9% YoY)

Goods: 4.7% YoY (Mar 4.8% YoY)

Services: 3.2% YoY (Mar 2.9% YoY)

Germany

German GDP was flat in Q1 2023 after a decline of -0.5% QoQ in Q4 2022 (revised down from -0.4% QoQ in the previous estimate). There was also a downgrade in Q2 2022 GDP growth from 0.0% QoQ to -0.2% QoQ.

German employment increased 57,000 or 0.1% MoM in March, and the unemployment rate fell -0.1 ppts to 2.8%. The number of unemployed individuals fell -18,000 or -1.4% MoM to 1.26 million.

Germany's CPI grew 0.4% MoM and 7.2% YoY in April, down from 7.4% YoY in March.

Energy: 6.8% YoY (Mar 3.5% YoY)

Food: 17.2% YoY (Mar 22.3% YoY)

Services: 4.7% YoY (Mar 4.8% YoY)

Goods: 9.3% YoY (Mar 9.8% YoY)

Italy

Italian GDP increased 0.5% QoQ in Q1 2023 after a slight decline of -0.1% QoQ in Q4 2022. Both industry and services recorded positive growth. Domestic demand contributed positively through increases in inventories and net exports.

Canada

Canada's GDP grew 0.1% MoM in February after an 0.6% MoM in January. Both services-producing industries and goods-producing industries edged up 0.1% MoM. Advanced estimates point to GDP down -0.1% MoM in March. However, the strength in the first 2 months of the year resulted in a 0.6% QoQ increase in Q1 2023.

Europe GDP

Eurozone economy grew marginally in the first quarter of 2023, but divergence is high (ING) - The eurozone economy carries on along the rim of stagnation. A meagre 0.1% quarter-on-quarter GDP growth in the first quarter with high divergence across member states is better than feared – but clearly no reason to cheer.

Spain’s economic growth picks up while core inflation falls again (ING) - The Spanish economy expanded 0.5% quarter-on-quarter in the first three months of the year, mainly due to strong growth in investment and net exports. Inflation rose again to 4.1% in April, but this was mainly due to unfavourable base effects. Core inflation fell again.

German economy not out of recessionary danger, yet (ING) - The stagnation of the German economy shows that the eurozone's largest economy has not escaped the risk of a recession.

France: Exports boost GDP while inflation increases again (ING) - French GDP grew by 0.2% over the quarter, due almost entirely to the normalisation of the supply chain situation, as domestic demand declines and inflation suprises to the upside.

Italian GDP growth surprisingly strong in first quarter (ING) - This is a very strong reading, but will be hard to replicate, at least in the short run. Still, we now believe that 2023 Italian GDP growth will average slightly above 1%.

Bank of Japan

Bank of Japan stays on hold but policy adjustment is coming (ING) - Based on upbeat activity data and higher-than-expected inflation, we believe the BoJ will take steps to normalise policy by adjusting its yield curve control tool in the coming months.

US GDP

US GDP growth disappoints as corporate America comes under pressure (ING) - The US economy expanded at a 1.1% annualised rate in the first quarter – lower than the 1.9% consensus – as business investment and a run down in inventories partially offset weather-boosted consumer spending and robust government expenditure. The headwinds from higher borrowing costs and reduced credit availability will weigh more heavily in 2H 2023.

Real GDP (Q1-2023, advance estimate) (TD Bank) - Real GDP expanded by 1.1% quarter-on-quarter (q/q, annualized) in the first quarter of 2023 – a marked deceleration from last quarter's 2.6% – and well below the consensus forecast of 1.9%.

U.S. GDP: Downshifting (BMO) - Real GDP growth was propped up by the strong start for consumers this year and by hefty government spending. Assuming the latter pipes down (no guarantees), the economy faces a weaker outlook, though inventory rebuilding could provide temporary support in Q2.

US Q1 GDP: Strength beneath the headline (CIBC) - GDP growth cooled to 1.1% annualized in the US in the first quarter, as a drop in inventory investment compounded declines in the interest-sensitive residential investment and business investment in equipment components. The advance was well below the 1.9% expected by the consensus, but the headline masked an acceleration in consumer spending, with both goods and services increasing, which added to growth in net exports and government spending.

Economic Growth Weakens in the First Quarter (NAHB) - In the first quarter of 2023, economic growth slowed to an annual rate of 1.1%, amid rising interest rates and an ongoing banking crisis. This quarter’s growth was dragged down by decreases in private inventory investment and residential fixed investment. Private inventory investment subtracted 2.26 percentage points off the headline growth rate for overall GDP, while residential fixed investment took 0.17 percentage points off the headline number.

Weak GDP growth in Q1 and a likely contraction in Q2 (EY Parthenon) - The US economy is unwell, and it’s starting to show. It started 2023 on a soft note with real GDP advancing a modest 1.1% in Q1 — below expectations.

Real GDP Increased at a 1.1% Annual Rate in Q1 (First Trust Portfolios) - Real GDP growth was a mixed bag in the first quarter and we still think we’re headed for a recession. First the bad news: real GDP grew at a soft 1.1% annual rate in Q1, lagging consensus expectations. Moreover, the growth was almost entirely due to consumer spending, with a 45.3% annualized gain in purchases of motor vehicles and parts, which is unlikely to be repeated later this year.

Housing Share of GDP Lower in the First Quarter of 2023 (NAHB) - Housing’s share of the economy moved lower at the end of the first quarter of 2023. Overall GDP increased at a 1.1% annual rate, following a 2.6% increase in the fourth quarter of 2022 and 3.2% increase in the third quarter of 2022. Despite overall GDP increasing, housing’s share of GDP decreased to 15.8%, below the 2022 fourth quarter share of 15.9%.

US

‘Supercore’ Inflation: Connecting the Dots to the Labor Market (TD Bank) - Non-housing service inflation (aka ‘supercore’) has become an area of particular focus for policymakers in recent months. At just over 50%, supercore accounts for a sizeable chunk of core PCE inflation – the Fed’s preferred inflation measure.

Triple-Play Volatility (Goldman Sachs) - Competing financial and economic priorities have continued to amplify the dissonance in US markets. We expect volatility to penetrate portfolios across three levels—market, sector, and stock—leaving equity prices generally flat for the year ahead.

Research US - Fed Preview: One more hike - Cuts still far away (Danske Bank) - We expect the Fed to deliver a final 25bp hike next week and then maintain the Fed Funds rate at 5.00-5.25% for the remainder of the year. Powell is unlikely to close the door for further hikes, but even with nominal rates on hold, we expect the monetary policy stance to continue tightening towards H2.

Federal Reserve preview: A final hike as US recession fears mount (ING) - Inflation remains 'unacceptably high', but banking stresses are leading to a tightening of lending conditions, which will do more to slow the economy than the likely 25bp hike on Wednesday. While the Fed will leave the door ajar for further hikes, the need for higher policy rates is highly questionable. We expect 100bp of rate cuts before year-end.

What U.S. interest rates are (and aren’t) telling us (DWS Group) - According to futures markets, investors expect Fed rate cuts starting in September. We think this prediction should be taken with a grain of salt.

US | Recession fears and debt ceiling anxiety are both weighing on interest rates (BBVA) - As suggested by the FOMC last month, “some additional policy firming” will likely mean that the Fed will decide to take the fed funds rate to a 5.00- 5.25% target range peak next Wednesday through a final 25bp rate hike.

States with Highest and Fastest Rising Construction Wages (NAHB) - Despite a housing market slowdown but reflecting persistent long-term labor challenges, wages in construction continue to rise, often outpacing and exceeding typical earnings in other industries.

Europe

ECB Preview - The art of compromise (Danske Bank) - Next week, the ECB will meet to deliver another rate hike in its hiking cycle that started in July last year. This time, the question is whether it will slow the hiking pace to 25bp or continue to hike once more by 50bp. We believe it will be a 50bp compromise deal with no specific forward guidance (nor guidance on balance sheet normalisation in H2 yet), but repeating a data-dependent approach to future policy decisions.

Europe’s Knife-Edge Path Toward Beating Inflation Without a Recession (IMF) - Success will require tighter macroeconomic policies tailored to changing financial conditions, strong financial supervision and regulation, and bold supply-side reforms.

Spain | 1Q23 EPA confirmed that the labor market gained momentum (BBVA) - Employment hardly changed between January and March, improving expectations. After adjusting by seasonality, job creation and total hours worked accelerated (to 1.2% and 0.6% t/t SWDA, respectively). In addition, the unemployment rate (12.6% SWDA) and the temporary employment rate (17.8% SWDA) fell.

Turkish Central Bank keeps rates on hold (ING) - In line with its forward guidance that the current policy rate is adequate to support the country's recovery from the earthquakes, the Central Bank of Turkey (CBT) left the policy rate flat at 8.5%.

Sweden's Central Bank Hikes Rates, Signals A Little More To Come (Wells Fargo) - Sweden's central bank, the Riksbank, delivered a widely expected policy rate increase at its announcement earlier this week. The Riksbank raised its repo rate 50 bps to 3.50%, and signaled that rates would probably be raised a further 25 bps in either June or September. Two policymakers dissented in favor of a smaller 25 bps hike, providing a dovish aspect to the announcement.

Swedish Tendency Survey: Lower inflation (Nordea) - The Economic Sentiment Indicator (ESI) declined in April, indicating sluggish growth. Inflation indicators declined across the board.

Swedish Q1 flash GDP: Resilience (Nordea) - The Q1 GDP flash estimate stood at 0.2% q/q and 0.3% y/y. The outcome was close to forecasts. The Riksbank’s call for Q1 GDP was 0.3% q/q and 0.3% y/y. Our forecast ahead of the flash was 0.0% q/q and 0.2 y/y, but the flash was clearly stronger than our view in our Economic Outlook from January.

Canada

BMO Business Activity Index — The Idles of March (BMO) - The Canadian economy continued to cool off in March based on BMO's Canadian Business Activity Index (BAI). The BAI fell 0.2% for the second straight month, highlighting that, despite the recent resilience, growth could turn negative as soon as the second quarter.

Real Estate

Housing Availability Expectations See Mild Improvement (NAHB) - After souring significantly in the final quarter of 2022, buyers’ expectations of housing availability edged up slightly in the first quarter of 2023, with 26% expecting the home search to get easier in the months ahead, just ahead of the 24% a quarter earlier. Despite the mild improvement, buyers’ perceptions of housing availability remain well below their level in the third quarter of last year (when 37% expected easier availability ahead).

Vulnerable housing and real estate markets (S&P Global) - The tightening of global monetary conditions is driving a softening of house prices, which in some key markets are expected to decline in 2023 and 2024.

Monetary Policy

Policy rates: end of the beginning or beginning of the end? (Allianz) - Ahead of the next round of monetary policy meetings next week, continued banking sector stress raises the question of whether financial stability concerns might alter the policy rate path in the US and the Eurozone, allowing inflation to remain higher for longer.

Outlook

FOMC and ECB meetings accompanied by PMIs and payrolls (S&P Global) - The start of May sees a truncated week for some amid public holidays, but it’s nevertheless a busy diary which includes worldwide PMI data, US nonfarm payrolls and rate setting meetings in the US, Eurozone, Norway, Brazil and Australia.

Subscribe to receive Econ Mornings every weekday at 9 am. More economic and finance content on Twitter, Reddit, and my website.